Key Takeaways:

- AI Adoption Accelerating: Top insurers are rapidly scaling AI solutions, with one client expanding coverage from 15% to 40% of claims.

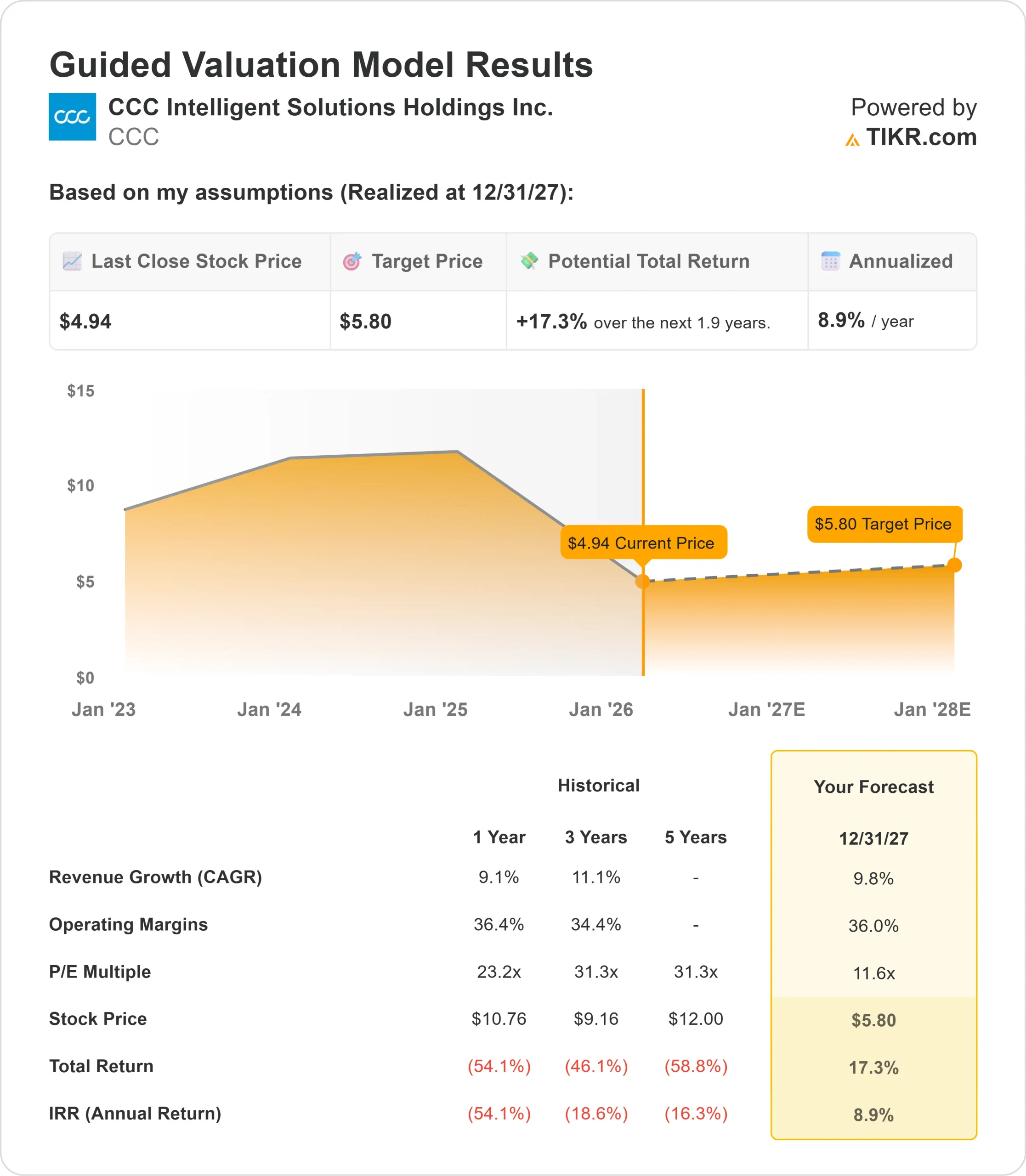

- Price Projection: Based on current momentum, CCC stock could reach $5.80 by December 2027.

- Potential Gains: This target implies a total return of 17% from the current price of $4.94.

- Annual Return: Investors could see roughly 9% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

CCC Intelligent Solutions (CCC) delivered strong third-quarter 2025 results with 12% revenue growth and continued expansion of its AI-driven platform across the insurance economy

CEO Githesh Ramamurthy highlighted accelerating adoption across the customer base, particularly among sophisticated insurers deploying multiple AI solutions.

- The company reported total revenue of $267 million, up 12% year over year and ahead of guidance. Adjusted EBITDA reached $110 million with a 41% margin, also exceeding expectations.

- One top-10 insurer increased claims leveraging at least one CCC AI model from roughly 15% to about 40% over the past year.

- The company’s AI layer now includes advanced capabilities in routing, estimating, and workflow automation.

- Mobile Jumpstart, an AI-powered estimating tool, surpassed an annualized run rate of over 1 million estimates in September, cutting preparation time from 30 minutes to under two minutes.

- CCC saw strong momentum in casualty claims, which is growing faster than the overall business.

- Liberty Mutual signed on to transition a substantial portion of its casualty business to CCC’s platform, with the deal reaching full run rate by mid-2026.

- The casualty market represents a similar total addressable market to auto physical damage but currently contributes only 10% of revenue with one-fifth the customer count.

- The EvolutionIQ acquisition continues delivering results. The platform’s medical record synthesis solution processed 6 million documents and 82 million pages over the past 12 months.

- In Q3, a top-25 CCC client became a new customer for EvolutionIQ’s workers’ compensation solution, demonstrating successful cross-selling opportunities.

Despite strong fundamentals and expanding AI adoption, CCC trades at $4.94, leaving room for upside for investors who recognize the company’s position in critical insurance infrastructure.

See analysts’ full growth forecasts and estimates for CCC stock (It’s free) >>>

What the Model Says for CCC Intelligent Solutions Stock

We analyzed CCC’s transformation into an AI-powered platform that connects over 35,000 businesses across the insurance ecosystem.

The company benefits from structural demand drivers. Insurers face mounting pressure to improve affordability as one in four Americans has downgraded or dropped coverage to free up cash, and one in three would temporarily go without coverage to afford basic necessities.

CCC’s AI solutions deliver measurable ROI and operational efficiency, helping insurers reduce costs.

Medical inflation is accelerating, particularly affecting casualty claims. CCC’s platform addresses this challenge through AI-powered medical record analysis and injury claims resolution, creating compelling value for insurers managing higher-dollar claims.

The repair facility network is also embracing innovation. More than 5,500 shops have adopted Build Sheets for accurate part selection, and Mobile Jumpstart usage is accelerating.

These tools are widening the productivity gap between facilities on the CCC platform and those that aren’t.

Using a forecast of 9.8% annual revenue growth and a 36% operating margin, our model projects the stock price will rise to $5.80 in 1.9 years. This assumes an 11.6x price-to-earnings multiple.

That represents compression from CCC’s historical P/E averages of 23.2x (one year) and 31.3x (three years). The lower multiple reflects near-term headwinds from declining claim volume, which moderated to 6% in Q3 from 9% in Q1, creating roughly a 1 percentage point drag on growth.

The real value lies in capturing long-term growth as AI adoption scales across the insurance economy while expanding into casualty and workers’ compensation markets.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CCC stock:

1. Revenue Growth: 9.8%

CCC’s growth centers on AI solution adoption and expansion in the casualty market.

- The company delivered 12% total growth in Q3, with approximately 5 points from cross-sell and upsell, 3 points from new logos, and 4 points from EvolutionIQ.

- Emerging solutions now contribute more than 2 percentage points of growth and account for 4% of total revenue.

- These AI-based solutions are the fastest-growing portion of the portfolio.

- When insurers fully deploy CCC’s AI layer across estimating, workflow, and reinspection, they can increase revenue per client by roughly 50%.

- Casualty growth outpaces overall company growth and represents a compelling long-term opportunity that may reach or exceed the scale of auto physical damage over time.

2. Operating margins: 36%

CCC has demonstrated strong margin expansion with adjusted EBITDA margins of 41% in Q3.

The company continues to see margin improvement opportunities through operational efficiency and cost management.

Management is making strategic investments in go-to-market capabilities and separating the roles of Chief Product Officer and Chief Technology Officer to drive stronger execution.

These investments are being funded by reallocation of existing spend to higher-ROI opportunities and should not impact margin expansion going forward.

3. Exit P/E Multiple: 11.6x

The market currently values CCC at 12.3x earnings. We assume modest compression to 11.6x over our forecast period, reflecting near-term uncertainty from claim volume headwinds.

As AI deployment continues and CCC demonstrates resilient execution across insurance and casualty markets, the company should command a premium multiple.

The strategic investments in product development and the teams that support them position CCC to capitalize on a transformative era of growth and innovation.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

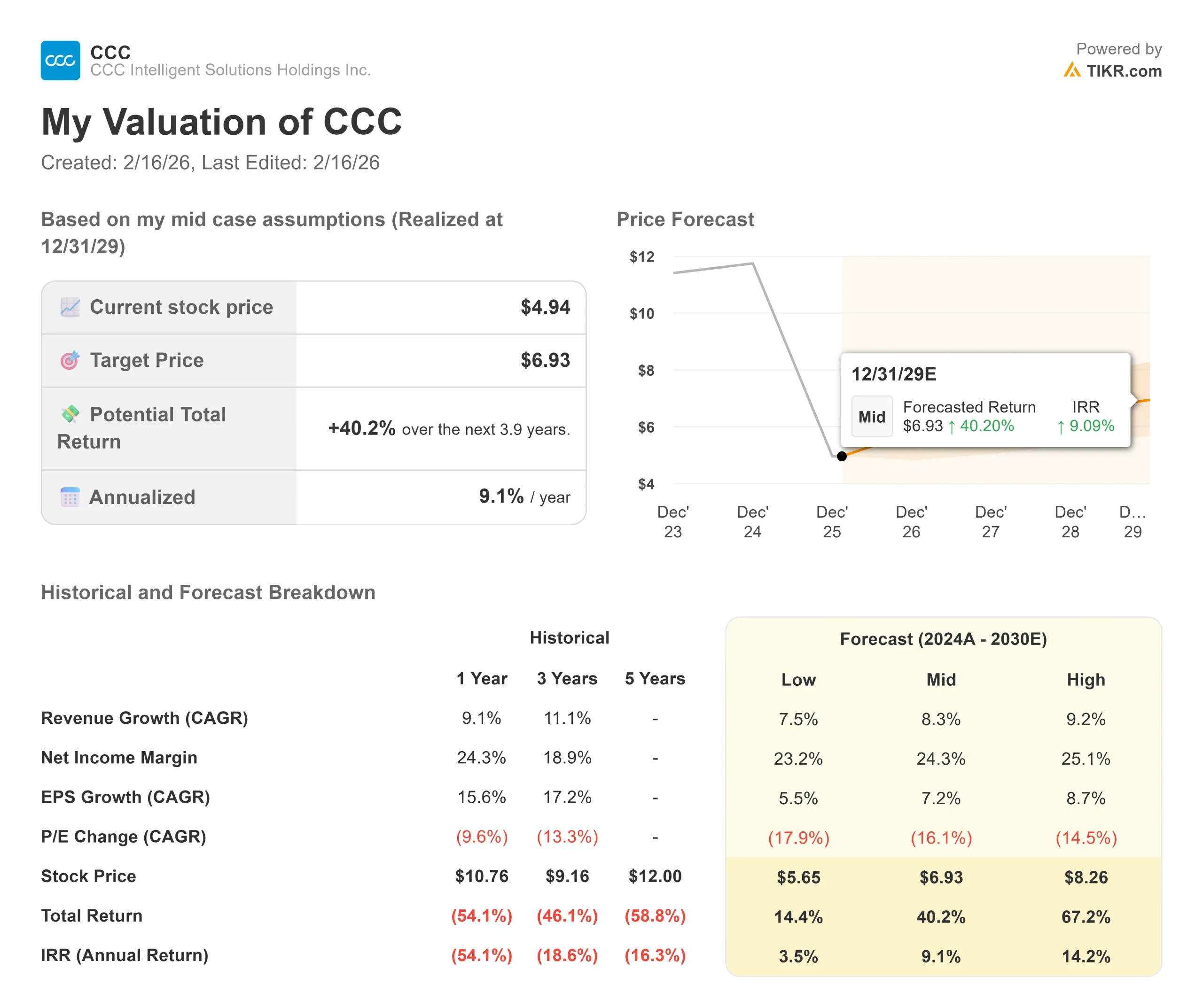

Insurance technology companies face adoption cycles and fluctuations in claim volume. Here’s how CCC stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth slows to 7.5% and net income margins compress to 23.2%, investors still see a 14.4% total return (3.5% annually).

- Mid Case: With 8.3% growth and 24.3% margins, we expect a total return of 40.2% (9.1% annually).

- High Case: If AI adoption accelerates to drive 9.2% revenue growth while CCC maintains 25.1% margins, returns could hit 67.2% total (14.2% annually).

See what analysts think about CCC stock right now (Free with TIKR) >>>

The range reflects the execution of AI deployment, the successful navigation of claim volume normalization, and the penetration of the casualty market.

In the low case, claim declines persist longer than expected, or AI adoption moderates.

In the high case, casualty wins accelerate, EvolutionIQ cross-selling exceeds expectations, and repair facility adoption drives network effects faster than anticipated.

How Much Upside Does CCC Intelligent Solutions Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!