Key Takeaways:

- CEO Transition: Las Vegas Sands appointed Patrick Dumont as Chairman and CEO effective March 1, 2026, succeeding Robert Goldstein who delivered a record $806 million Marina Bay Sands EBITDA quarter and $2.9 billion in full year Singapore EBITDA before moving to a senior advisor role through March 2028.

- Q4 2025 Results: Las Vegas Sands reported Q4 revenue of $3.65 billion beating the $3.34 billion estimate by 9%, yet operating profit of $707 million missed the $806 million estimate as Macau EBITDA of $608 million disappointed against a $700 million quarterly target despite rolling chip volume surging 60% year-over-year.

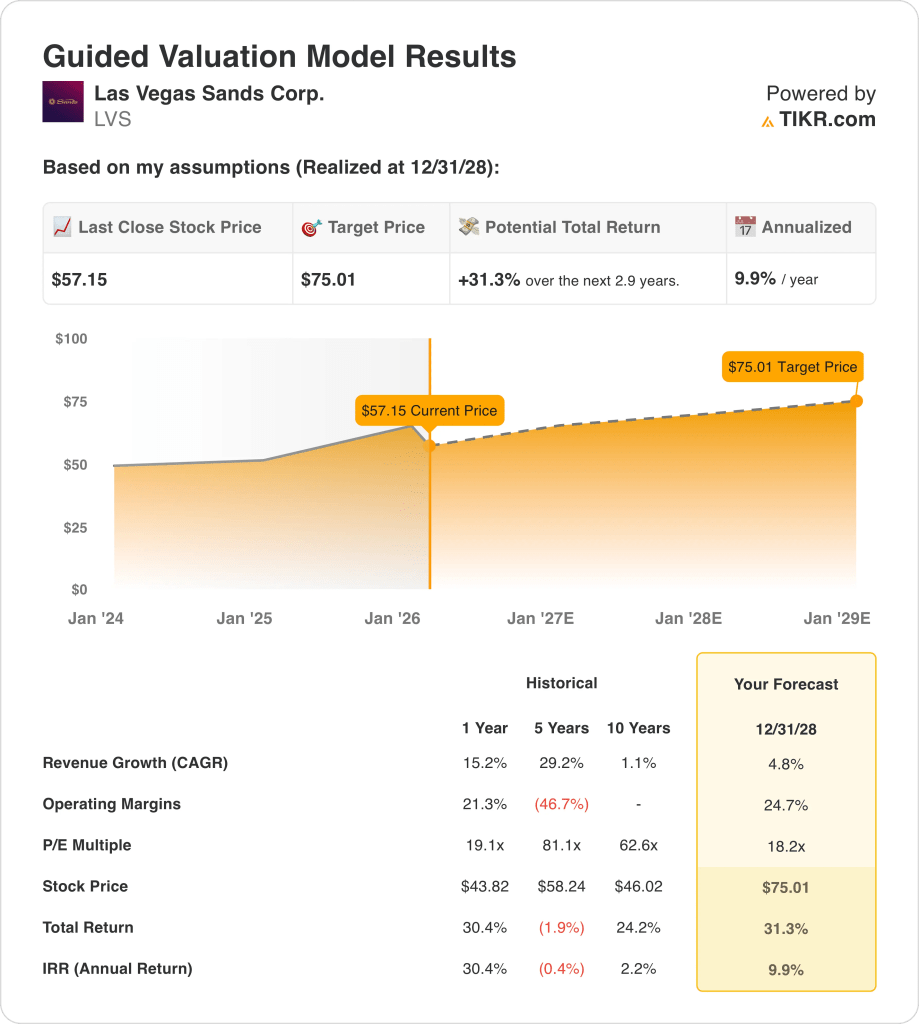

- Price Target: Based on 5% revenue growth, 25% operating margins, and an 18x exit multiple, Las Vegas Sands stock could reach $75 by December 2028 from $57 today.

- Return Profile: Las Vegas Sands implies 31% total upside from $57 to $75 over 3 years, equating to a 10% annualized return supported by $1.56 billion in remaining share repurchase authorization and a $0.25 quarterly dividend as Macau margins stabilize toward low 30%.

Breaking Down the Case for Las Vegas Sands Corp.

Last February, Las Vegas Sands (LVS) appointed Patrick Dumont as Chairman and CEO effective March 1, 2026, succeeding Robert Goldstein who served 30 years and delivered $2.9 billion in Singapore EBITDA before transitioning to a senior advisor role through March 2028.

The company delivered $13 billion in fiscal 2025 revenue reflecting 15% growth, yet operating income of $3.1 billion at 24% margins came as Macau EBITDA of $608 million in Q4 missed the internal $700 million quarterly target while Marina Bay Sands posted a record $806 million EBITDA quarter.

Outgoing CEO Robert Goldstein stated on the January 28, 2026, earnings call that “Marina Bay Sands has delivered an EBITDA of $806 million, simply the greatest quarter in the history of casino hotels,” while simultaneously acknowledging Macau disappointment and committing to better results in 2026 as rolling chip volume surged 60% year-over-year.

Q4 revenue beat estimates at $3.65 billion versus the $3.34 billion consensus, yet operating profit of $707 million missed the $806 million estimate as Macau’s hold-adjusted EBITDA margin compressed 390 basis points to 29% driven by higher promotional intensity, elevated event costs from the NBA China Games Week partnership, and wage investments adding table hour capacity.

Also, LVS repurchased $500 million of LVS common stock in Q4 and increased SCL ownership to 74.8% with $66 million in additional SCL purchases, leaving $1.56 billion of share repurchase authorization remaining as management targets continued aggressive buybacks alongside the $0.25 quarterly dividend.

The investment tension centers on whether incoming CEO Dumont sustains Marina Bay Sands’ record $806 million EBITDA trajectory toward $3.1 billion to $3.4 billion annually while reversing Macau’s 390 basis point margin compression toward the targeted low 30% level, against a backdrop of $57 current stock price, 19x forward P/E, and 10% projected annualized returns through December 2028 that require 5% revenue growth and 25% operating margins without further premium segment promotional escalation.

What the Model Says for LVS Stock

Last February, Las Vegas Sands named Patrick Dumont as Chairman and CEO effective March 1, 2026, as Q4 Macau EBITDA of $608 million missed the $700 million quarterly target while Marina Bay Sands delivered a record $806 million quarter, creating a split execution story entering 2026.

The model’s assumption underwrites 4.8% revenue growth, 24.7% operating margins, and an 18.2x exit multiple, producing a $75 target price by December 2028, with margins sitting above fiscal 2024’s 21.3% but well below the 15% revenue growth the company delivered last year.

The market assumption for the forward P/E as of February 2026 stands at 18.2x, down from 22x at December 2025, as Macau margin compression of 390 basis points in Q4 and intense promotional spending weighed on investor sentiment despite $500 million in Q4 share repurchases.

The model delivers 31.3% total upside and a 9.9% annualized return from $57.15, sitting just below the standard 10% equity hurdle rate, as $1.56 billion in remaining buyback authorization and a $0.25 quarterly dividend partially offset the risk of Macau margin recovery falling short under incoming CEO Dumont.

The model signals a Hold, as a 9.9% annualized return marginally trails the 10% equity hurdle rate, and reaching $75 requires both Marina Bay Sands sustaining record EBITDA and Macau margins recovering toward low 30% without further promotional escalation through 2028.

With a 9.9% annualized return sitting just below the 10% equity hurdle, the model supports neither clear capital appreciation nor preservation, as the $75 target by December 2028 demands simultaneous Singapore record sustainability and Macau margin recovery, leaving risk uncompensated by valuation math alone.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Las Vegas Sands stock:

1. Revenue Growth: 4.8%

Las Vegas Sands stock delivered 15% revenue growth in fiscal 2025 to $13 billion as Marina Bay Sands posted a record $806 million EBITDA quarter, yet the post-pandemic recovery tailwind that produced 152% growth in fiscal 2023 no longer exists as a structural support.

The fiscal 2026 estimate of $13.76 billion reflects 5.7% growth as Macau operations delivered $2.06 billion in Q4 revenue up 16%, yet rolling chip volume’s 60% surge introduced lower-margin premium segment concentration that limits revenue-to-EBITDA conversion.

The 4.8% model’s assumption through fiscal 2028 rests on Marina Bay Sands sustaining above $2.9 billion annually, Macau recovering toward the $700 million quarterly EBITDA target, and CEO Patrick Dumont executing his first full year without operational disruption from the leadership transition effective March 1, 2026.

Any failure in Macau’s base mass recovery, intensification of the already “intense” promotional environment acknowledged by management, or Singapore hold normalization below the $71 million favorable Q4 variance compounds revenue shortfalls faster than the single-property concentration of Marina Bay Sands can absorb.

This sits below the 1-year revenue growth of 15.2%, as the post-recovery normalization in both Singapore and Macau limits the pace of incremental volume capture, and sustaining even 4.8% requires Macau EBITDA to grow consistently while Marina Bay Sands holds near-record output levels.

2. Operating Margins: 24.7%

Las Vegas Sands stock reported 23.5% operating margins in fiscal 2025 on $3.07 billion in operating income, as fiscal 2024’s 21.7% margin improved through Singapore’s record EBITDA quarter and Macau’s 60% rolling chip volume surge, though at a cost of $7.35 billion in total operating expenses including $3.93 billion in other operating expenses.

The 24.7% model’s assumption sits above fiscal 2025’s 23.5% level, as fiscal 2026 EBIT margins are estimated at 25% and EBITDA margins at 39.6%, but Macau’s hold-adjusted margin compression of 390 basis points in Q4 and $1.84 billion in SG&A expenses create a structural ceiling without base mass recovery.

Margin expansion toward 24.7% requires Macau’s management commitment to “low 30s” EBITDA margins to materialize, NBA China Games Week event costs to moderate after being described as the “biggest event in company history,” and March 2026 annual wage adjustments to stay within manageable bounds for frontline staff across both markets.

The market assumption for the forward P/E as of February 2026 sits at 18.2x, down from 22x at December 2025, as investors priced in Q4 Macau margin compression and the promotional intensity management described as “stable but subject to change month to month,” creating a sentiment discount that margin execution must overcome.

All three margin drivers, Singapore hold rates, Macau promotional discipline, and SG&A control, must work simultaneously to reach 24.7%, and any single deterioration activates a downward cascade across both EBITDA at 39.6% and net income margins at 15.9% estimated for fiscal 2026.

This sits above the 1-year operating margin of 21.3% from fiscal 2024, as Marina Bay Sands’ record output and Macau’s premium segment revenue share growth pushed margins higher in fiscal 2025, and sustaining 24.7% through fiscal 2028 requires both markets to maintain their respective fiscal 2025 trajectories without promotional cost escalation.

3. Exit P/E Multiple: 18.2x

The 18.2x exit multiple capitalizes Las Vegas Sands stock’s normalized net income at December 2028 under conditions of moderate revenue growth, margin expansion, and a post-transition leadership environment, treating the multiple as a terminal earnings anchor rather than a sentiment-driven premium.

The model already embeds 24.7% operating margins and 4.8% revenue growth through fiscal 2028, meaning the 18.2x exit multiple does not require additional credit for scale efficiency or capital allocation improvement, as both are already absorbed in the earnings trajectory.

The market assumption for the forward P/E as of February 2026 stands at 18.2x, down from 22x at December 2025, as Macau’s Q4 operating profit miss of $707 million versus the $806 million estimate and the CEO transition effective March 1, 2026, compressed investor willingness to pay above 20x for near-term execution uncertainty.

At 18.2x, the exit multiple sits in line with current market assumptions and does not embed a re-rating, as the $1.56 billion share repurchase authorization and $0.25 quarterly dividend support earnings-per-share accretion but cannot substitute for operational margin delivery in Macau or Singapore hold stability.

If Macau fails to recover toward low 30% EBITDA margins or Marina Bay Sands hold normalizes below the $45 million to $71 million quarterly variance range, the exit multiple compresses below 18.2x rather than expanding, and the $75 target price collapses toward the $58 5-year historical stock price level.

This sits below the 1-year historical P/E of 19.1x, as the CEO transition, Macau margin compression, and Macau promotional environment uncertainty justify a modest valuation discount versus the trailing year, and any sustained Macau EBITDA recovery toward $700 million quarterly would be required before the multiple re-rates above 19x.

What Happens If Things Go Better or Worse?

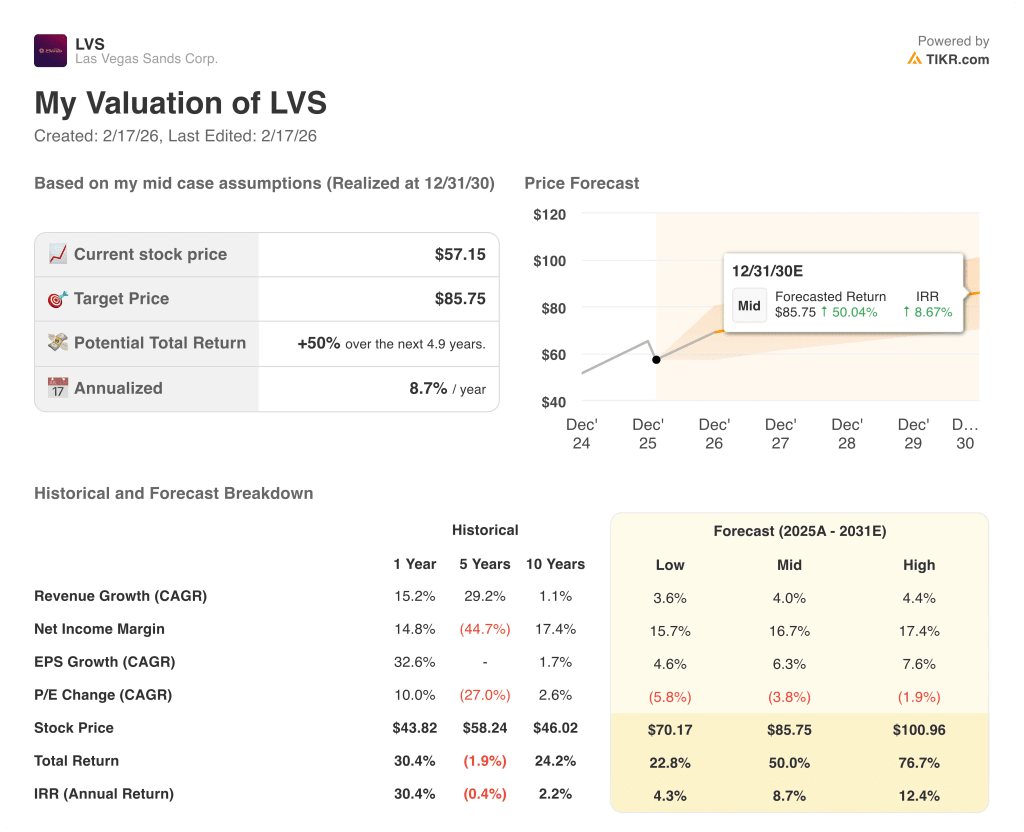

Las Vegas Sands stock results are shaped by Marina Bay Sands’ hold rate sustainability, Macau’s base mass recovery pace, and incoming CEO Patrick Dumont’s promotional discipline across both markets through December 2030.

- Low Case: If Macau margins stay compressed and Singapore hold normalizes below Q4 levels, revenue grows 4% and net margins hold near 16% → 4% annualized return.

- Mid Case: With Macau recovering toward the $700 million quarterly EBITDA target and Marina Bay Sands sustaining record output, revenue grows 4% and net margins reach 17% → 9% annualized return.

- High Case: If base mass recovers, promotional intensity moderates, and Dumont’s capital allocation accelerates share count reduction, revenue grows 4% and net margins approach 17% → 12% annualized return.

How Much Upside Does Las Vegas Sands Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!