Key Stats for DaVita Stock

- Past-Week Performance: 6%

- 52-Week Range: $101 to $157

- Current Price: $148

What Happened to DaVita Stock?

DaVita (DVA) surged 35% in February 2026, climbing from $109.06 to $147.75 — its strongest monthly gain in over a year.

The catalyst was DaVita’s Q4 2025 earnings report, where the company beat both EPS estimates ($3.40 vs. $3.16 expected) and revenue ($3.62B vs. $3.50B expected).

The bigger shock was 2026 guidance, with DaVita projecting adjusted EPS of $13.60 to $15.00, a 33% jump over 2025 that blew past analyst expectations of $12.65.

Adding fuel to the rally, DaVita announced a ~$200M minority investment in Elara Caring to build a kidney-specific home care model, a direct bet on reducing hospitalizations and expanding beyond the clinic.

The market is no longer viewing DaVita as a struggling dialysis operator, as its Integrated Kidney Care business turned profitable for the first time in 2025, a milestone originally not expected until 2026.

Furthermore,TD Cowen raised its price target to $144 and UBS lifted theirs to $190, both signaling that Wall Street is finally repricing DaVita as a growth story, not just a dialysis utility.

Where is the DVA Stock Headed?

The 35% February surge is not just a reaction to one earnings beat — it signals the market is beginning to reprice DaVita as a multi-vertical kidney care platform, not a single-service dialysis company.

The fundamental case is hard to ignore, with 2026 EPS forecast to grow 30.7% to $14.08 and free cash flow guided at $1.125B midpoint, giving DaVita real financial firepower heading into the year.

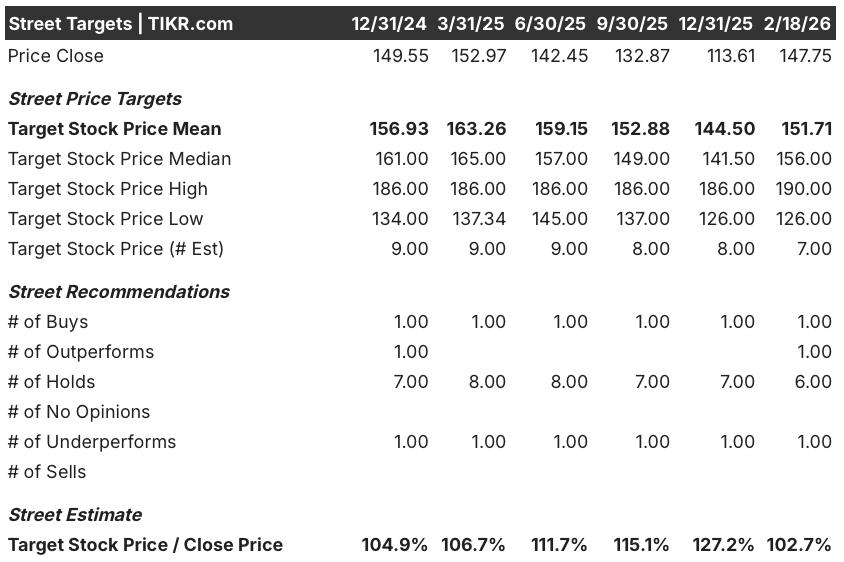

Wall Street remains cautiously positioned, with a mean price target of $151.71 across 7 analysts — only 2.7% above the current price of $147.75, with just 1 Buy, 1 Outperform, and 6 Holds on record.

The target spread, however, reveals the real debate: the Street’s high sits at $190 while the low is $126, a $64 gap that reflects deep disagreement on how much IKC profitability and the Elara Caring expansion are actually worth.

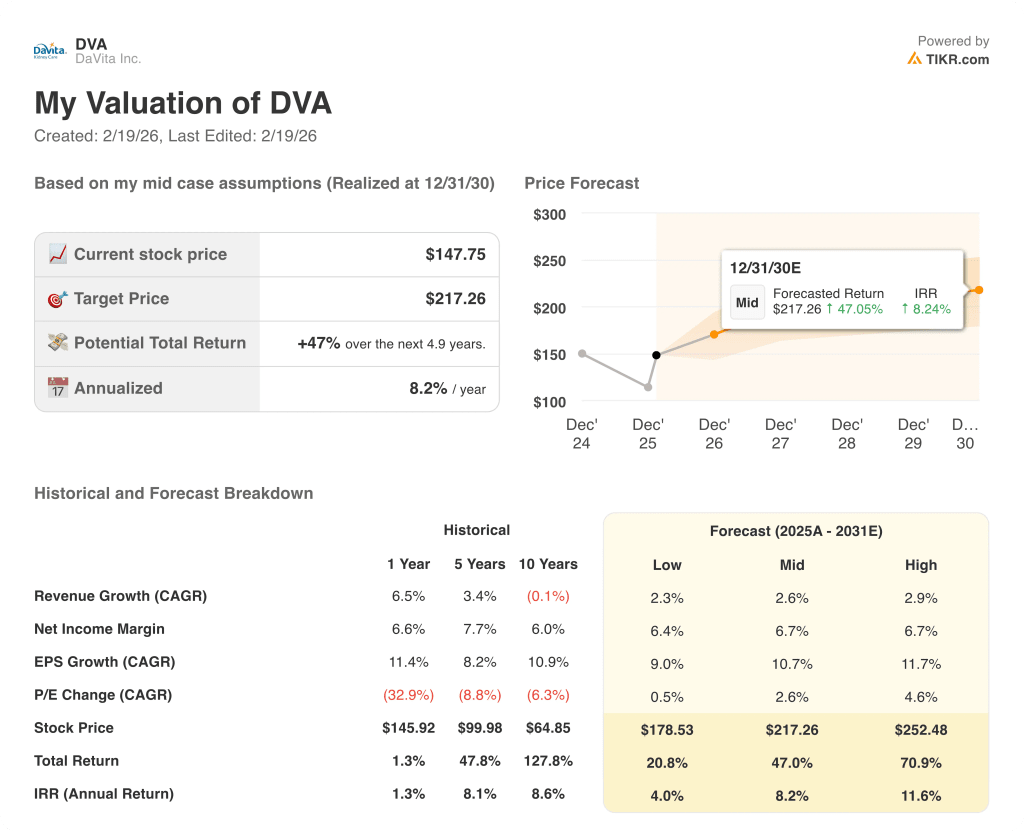

TIKR’s valuation model paints a more optimistic picture, forecasting a mid-case target price of $217.26 by December 2030, representing a 47% total return from current levels at an annualized IRR of 8.2% per year.

To put that in context, even the model’s low-case scenario projects a stock price of $178.53, still representing over 20% upside from today, suggesting the downside is relatively well protected at current levels.

The risks are tangible and dated — Berkshire Hathaway sold 1.6M shares on January 29, the ACA premium tax credit expiration creates a $40M headwind in 2026 growing to $70M in 2027, and U.S. treatment volume remains flat with no near-term recovery expected before 2029.

DaVita looks like a stock that has already priced in the good news at current levels, making it a compelling long-term story but a tricky near-term buy until analysts meaningfully revise their targets upward.

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Wall Street’s best ideas don’t stay hidden for long. Catch analyst upgrades, earnings beats, and revenue surprises on thousands of stocks the moment they happen with TIKR for free →