Key Takeaways:

- CEO Succession: IDEXX Laboratories announced on January 13 that Michael Erickson will succeed Jay Mazelsky as President and CEO, with Mazelsky becoming Executive Chair before retiring in May 2027, transferring leadership amid a year when shares surged 64%.

- Earnings and Outlook: IDEXX reported Q4 revenue of $1.09 billion, beating estimates by $18 million, while guiding 2026 revenue of $4.63–$4.72 billion above consensus, yet shares fell 6% as management flagged a roughly 2% decline in U.S. same-store clinical visits.

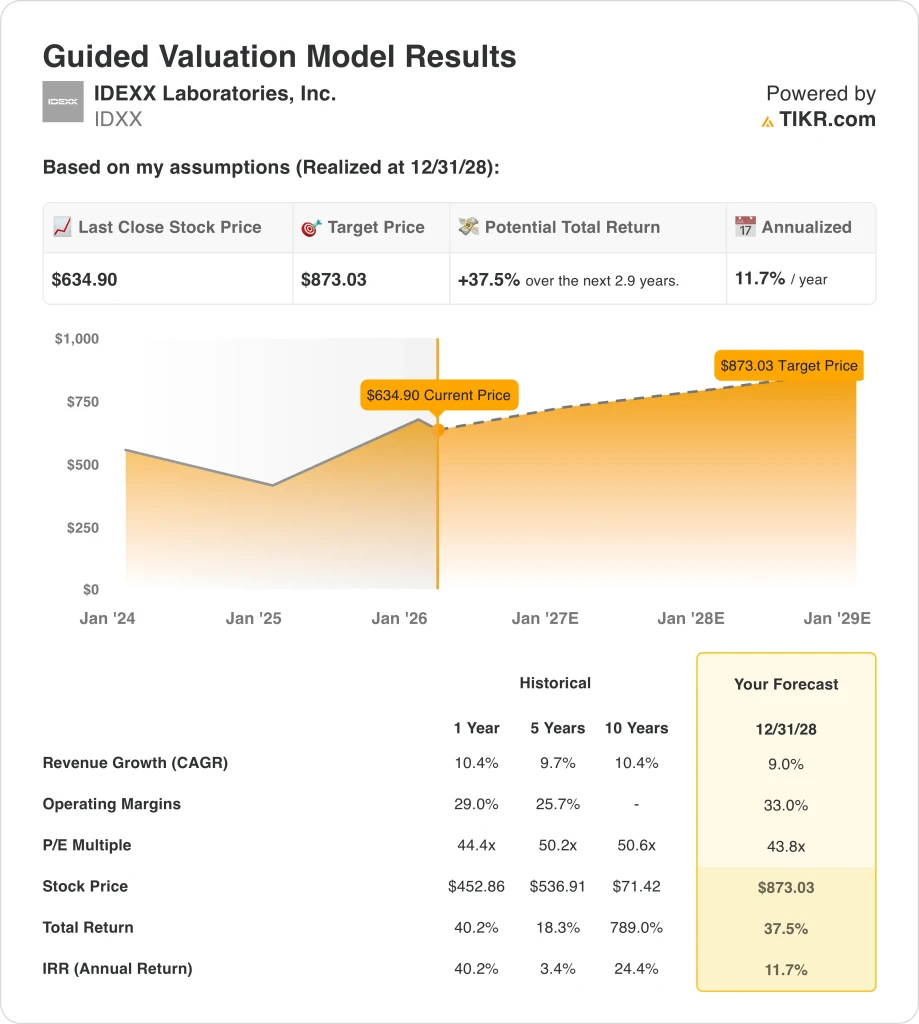

- Price Target: Based on 9% revenue growth, 33% operating margins, and a 43.8x exit multiple, IDEXX stock could reach $873 by December 2028 from $635 today.

- Return Profile: IDEXX implies 38% total upside from $635 to $873 over 2.9 years, equating to a 12% annualized return supported by planned 1–2% annual diluted share reductions and $1.1 billion in annual free cash flow generation.

Breaking Down the Case for IDEXX Laboratories, Inc.

On January 13, IDEXX Laboratories (IDXX) appointed Michael Erickson as incoming President and CEO, succeeding Jay Mazelsky who delivered 64% stock appreciation in 2025 before transitioning to Executive Chair through May 2027.

Q4 revenue of $1.09 billion grew 14% as reported, with full-year 2025 revenue reaching $4.30 billion on 10% organic growth, while gross margins expanded to 61.8% from 58.8% in 2021.

Operating expenses of $1.30 billion in 2025, split between $1.05 billion in SG&A and $250 million in R&D, supported operating income of $1.36 billion at a 31.6% operating margin, up 90 basis points comparable year-over-year.

CFO Andrew Emerson stated on the February 2 earnings call that “from a clinical visit pressure, it’s an area that we want to make sure that we continue to understand,” embedding a roughly 2% same-store visit decline into 2026 guidance while targeting 8–10% CAG Diagnostics recurring revenue growth.

Nearly 6,400 inVue Dx instruments placed in 2025 contributed over $75 million in revenue, and the December controlled launch of Fine Needle Aspirate cytology targets mast cell tumor detection, expanding an addressable Cancer Dx opportunity management pegs at $1.1 billion.

Free cash flow of $1.1 billion, equal to 100% of net income, funded $1.2 billion in buybacks at an average $506 per share, reducing diluted share count by 2.7% while leverage stayed at 0.5x gross.

The investment tension centers on whether incoming CEO Erickson sustains 9% revenue growth and expands operating margins to 33% against a $635 stock price, 43.8x exit multiple, and 12% annualized return target that assumes persistent veterinary visit softness never deepens beyond the guided 2% decline through December 2028.

What the Model Says for IDXX Stock

IDEXX’s Q4 beat of $18 million and 64% share appreciation in 2025 establish execution credibility, yet management’s own guidance of a 2% U.S. same-store clinical visit decline constrains the organic volume growth the model requires to reach its target.

The model’s assumption of 9% revenue growth, 33% operating margins, and a 43.8x exit multiple produces a $873 target price by December 2028, with the margin assumption sitting 140 basis points above 2025’s 31.6% reported level and the growth assumption tracking below the 10.4% delivered in fiscal 2025.

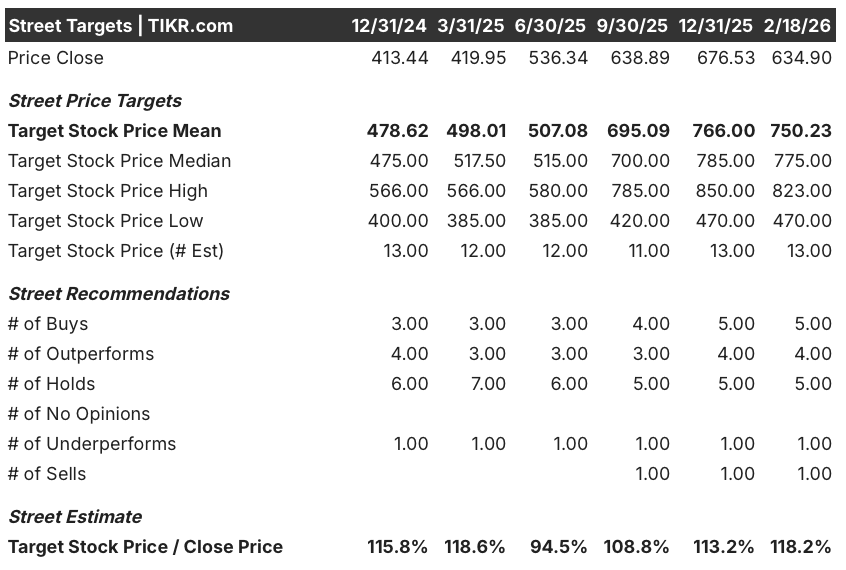

The market assumption for forward P/E stands at 43.78x as of February 18, nearly identical to the model’s 43.8x exit multiple, meaning the stock must sustain current market pricing through 2028 with no incremental re-rating to hit the target.

The street mean target of $750 against a $635 close produces a target-to-price ratio of 118%, recovering from a trough of 95% in June 2025, while the current recommendation breakdown of 5 Buys, 4 Outperforms, 5 Holds, and 1 Sell reflects analyst conviction that has strengthened modestly since December 2024 but remains divided.

The model delivers 38% total upside from $635 to $873, equating to an 11.7% annualized return that clears the 10% equity hurdle, supported by $1.1 billion in annual free cash flow and offset by the constraint that the market already prices the stock at the model’s exit multiple.

The CEO transition to Michael Erickson, effective following Jay Mazelsky’s move to Executive Chair, introduces execution continuity risk precisely as inVue Dx FNA and international Cancer Dx expansion enter their most capital-intensive commercial phases in 2026.

This is a marginal Buy: the 11.7% annualized return clears the 10% hurdle, the street mean at 118% of current price confirms directional upside, but the model’s exit multiple already matches today’s market assumption, requiring sustained premium pricing and margin expansion without leadership disruption through December 2028.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for IDEXX stock:

1. Revenue Growth: 9%

IDEXX stock delivered 10.4% revenue growth in fiscal 2025 to $4.30 billion, driven by 12% organic CAG growth and record inVue Dx instrument placements, yet management’s own 2026 guidance incorporates a 2% U.S. same-store clinical visit decline that removes volume recovery as a structural tailwind.

The fiscal 2026 consensus estimate of $4.68 billion reflects 8.7% growth, nearly identical to the model’s assumption, as CAG Diagnostics recurring revenue guidance of 8–10% organic growth anchors the range while instrument revenue faces a deliberate step-down lapping the inVue Dx launch.

The 9.0% model’s assumption through December 2028 rests on international CAG Diagnostics sustaining double-digit growth, Cancer Dx expanding beyond 6,000 North American customers into international markets in Q1 2026, and inVue Dx FNA adoption generating incremental consumable pull-through without wellness visit trends deteriorating beyond the guided 2% decline.

Any acceleration in U.S. wellness visit declines past 2%, combined with a slower-than-expected international Cancer Dx rollout and leadership disruption from the CEO transition, compounds CAG recurring revenue shortfalls faster than reference lab volume gains can absorb, as each 1% revenue miss on a $4.68 billion base represents $47 million in foregone top-line growth that directly pressures the earnings trajectory.

This sits below the 1-year revenue growth of 10.4%, as the post-inVue Dx launch normalization and persistent wellness visit pressure structurally limit volume recovery, and sustaining 9.0% requires international diagnostics expansion and Cancer Dx adoption to offset the approximately 200 basis point U.S. clinical visit drag embedded in guidance.

2. Operating Margins: 33%

IDEXX stock reported 31.6% operating margins in fiscal 2025 on $1.36 billion in operating income, expanding 90 basis points comparable year-over-year as gross margins reached 61.8% and SG&A of $1.05 billion consumed 24.4% of revenue across a $4.30 billion revenue base.

The 33.0% model’s assumption sits 140 basis points above fiscal 2025’s reported level, broadly consistent with the fiscal 2026 EBIT margin consensus of 32.2%, as management guided 30–80 basis points of comparable operating margin improvement driven by lab productivity initiatives, cloud software recurring revenue expansion, and CAG Diagnostics recurring mix gains.

Reaching 33.0% by December 2028 requires SG&A to grow materially slower than the revenue pace that produced $1.05 billion in fiscal 2025, capex stepping up to $180 million in 2026 without compressing free cash flow conversion below the guided 85–95%, and gross margins holding above 61.8% as instrument revenue mix normalizes lower.

The market assumption for the forward P/E as of February 18 stands at 43.78x, down from 48.03x at December 2025, as the cautious 2026 visit outlook compressed investor willingness to pay above 48x, creating a sentiment reset the model’s 33.0% margin assumption must overcome through sustained execution rather than multiple re-expansion.

Any failure in Reference Lab productivity gains, combined with incremental commercial investment supporting the international Cancer Dx rollout and the $180 million capex cycle in 2026, collapses operating margins back toward 31.6% faster than cloud software ARR growth can compensate, as each 10 basis point margin shortfall on $4.68 billion of forward revenue represents $47 million in missed operating income.

This sits above the 1-year operating margin of 31.6%, as the model embeds lab productivity gains, SG&A leverage from the completed global commercial expansion, and cloud-based PIMS recurring revenue scaling, and reaching 33.0% requires gross margins to expand beyond 61.8% while $180 million in 2026 capex absorbs a rising share of operating cash flow.

3. Exit P/E Multiple: 43.8x

The 43.8x exit multiple capitalizes IDEXX stock’s normalized net income at December 2028 under conditions of 9.0% revenue growth and 33.0% operating margins, treating the multiple as a terminal earnings anchor for a veterinary diagnostics platform with high-90s customer retention and structurally recurring consumable revenue streams.

The model already embeds 140 basis points of operating margin expansion and 9.0% revenue growth through December 2028, meaning the 43.8x exit multiple does not require additional credit for Cancer Dx panel expansion or inVue Dx FNA adoption, as both are absorbed in the earnings trajectory and a higher multiple would double-count growth already in the model.

The market assumption for the forward P/E as of February 18 stands at 43.78x, compressing from 48.03x at December 2025 and from a peak of 48.34x at September 2025, as the February 2 earnings call’s 2% clinical visit decline guidance reset investor willingness to pay premium multiples, placing the model’s 43.8x exit in line with the current market assumption rather than above it.

If international Cancer Dx adoption stalls, CEO transition disrupts commercial execution, or U.S. wellness visits decline beyond 2%, earnings compression below the 33.0% margin assumption pushes the sustainable multiple toward 34.14x (the current forward EV/EBIT market assumption) rather than sustaining near 43.8x, collapsing the $873 target price by roughly 20%.

This sits below the 1-year historical P/E of 44.4x, as recent multiple compression from the visit-decline guidance and the pending leadership transition justify a modest discount to the trailing year’s valuation premium, and sustaining 43.8x through December 2028 requires margin expansion to 33.0% and clinical visit trends stabilizing without further deterioration below the guided 2% decline.

What Happens If Things Go Better or Worse?

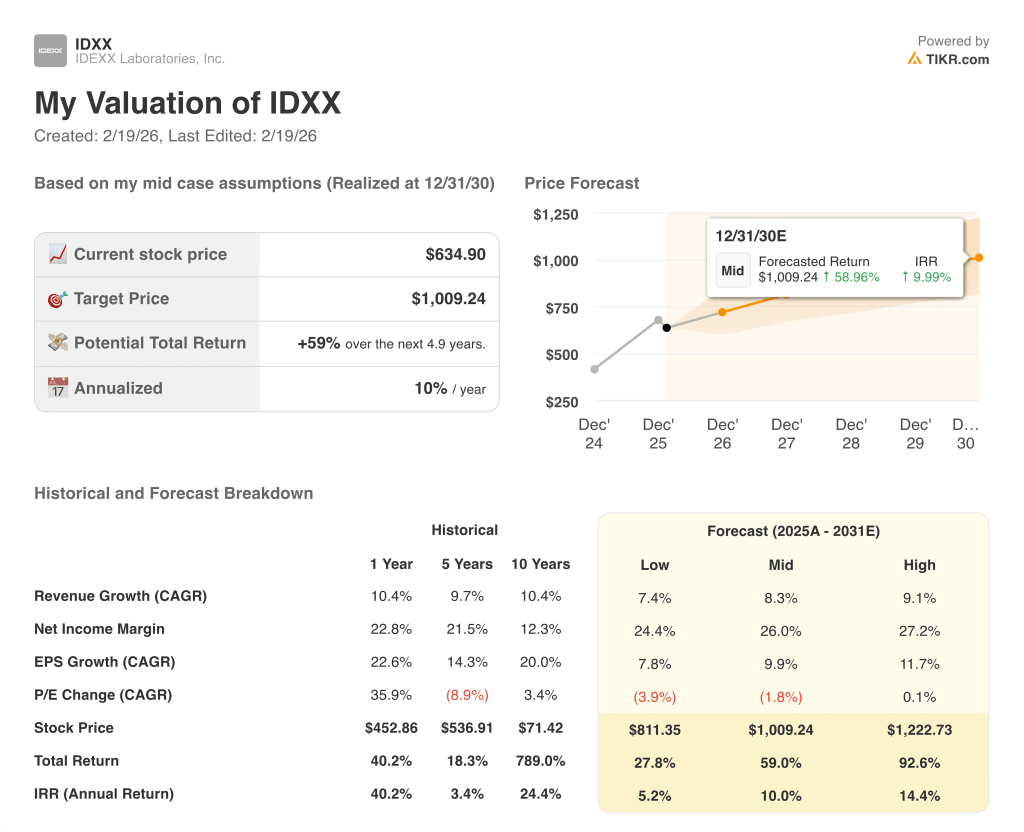

IDEXX stock scenarios through December 2030 center on whether veterinary visit recovery materializes, Cancer Dx and inVue Dx consumable adoption scales, and the incoming CEO sustains commercial execution through the leadership transition.

- Low Case: If wellness visit declines persist beyond the guided 2% and Cancer Dx international adoption lags, revenue grows around 7% and net income margins stay near 24% → 5% annualized return.

- Mid Case: With clinical visits stabilizing near guided levels and inVue Dx FNA driving incremental consumable pull-through, revenue growth near 8% and margins improving toward 26% → 10% annualized return.

- High Case: If international Cancer Dx scales faster than expected and corporate inVue Dx placements accelerate, revenue reaches about 9% and margins approach 27% → 14% annualized return.

How Much Upside Does IDEXX Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!