Key Stats for Workday Stock

- Past-Week Performance: -8.7%

- 52-Week Range: $117.8 to $276

- Current Price: $124.2

What Happened?

Workday (WDAY) entered fiscal 2027 carrying a 40% year-to-date stock decline and a co-founder returning to the CEO chair, yet its agentic AI business, which refers to software that autonomously executes tasks like payroll processing and HR case resolution, crossed $400 million in annual recurring revenue while the stock trades at $124.18, less than half its 52-week high of $276.00.

On February 24, co-founder Aneel Bhusri, reinstated as CEO effective February 6, reported Q4 subscription revenue of $2.36 billion, up 15.7% year-over-year, while guiding fiscal 2027 subscription revenue to $9.93 billion to $9.95 billion, roughly $50 million short of the $10 billion consensus compiled by LSEG, triggering price-target cuts from at least 26 analysts.

Emerging AI products generated over $100 million in net new annual contract value in Q4 alone, growing over 100% year-over-year, and expansion deals that included AI solutions were nearly 50% larger on average than non-AI deals, a spread that peer Salesforce, which trades at 13.98x forward earnings versus Workday’s 11.94x, has not yet quantified in equivalent terms.

Bhusri stated on the Q4 fiscal 2026 earnings call that “no amount of vibe coding is going to produce an HR or an ERP system,” tying directly to the February 15 general availability launch of Sana Enterprise, an AI layer that connects Workday’s HR and finance platform to external tools including Microsoft Outlook, Gmail and Salesforce across the company’s 75 million users.

Workday’s $3.18 billion free cash flow target for fiscal 2027, a 15% increase, combined with $2.9 billion in remaining buyback authorization and a consumption-based Flex Credits pricing model already adopted by nearly 50 customers including Accenture, Nike and Merck, positions the platform to reaccelerate growth as 12 organically built agents enter general availability through the March R1 release.

Wall Street’s Take on WDAY Stock

Bhusri’s return as CEO and the February 24 earnings miss reframed WDAY as an AI disruption casualty, yet the same quarter delivered $1.22 billion in free cash flow, confirming the platform’s cash generation remains structurally intact.

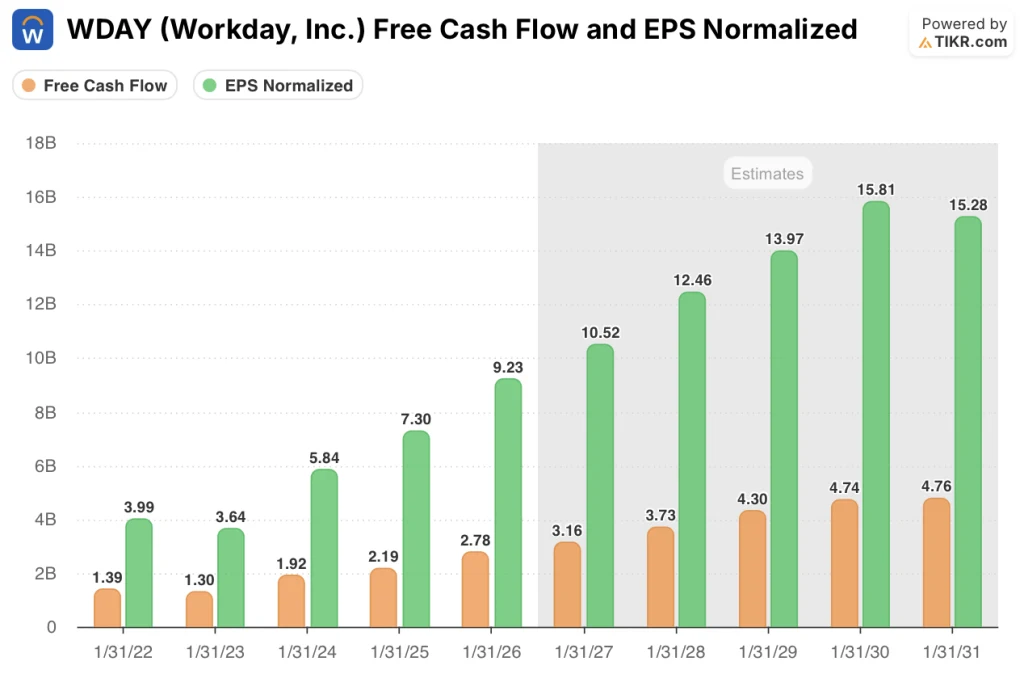

Workday’s normalized EPS is forecast to climb from $9.23 in FY2026 to $10.52 in FY2027 and $12.46 in FY2028, anchored by $400 million in AI ARR growing over 100% year-over-year, a 97% gross retention rate locking in the existing revenue base, and $2.78 billion in FY2026 free cash flow confirming the platform generates real cash regardless of macro-driven deal delays.

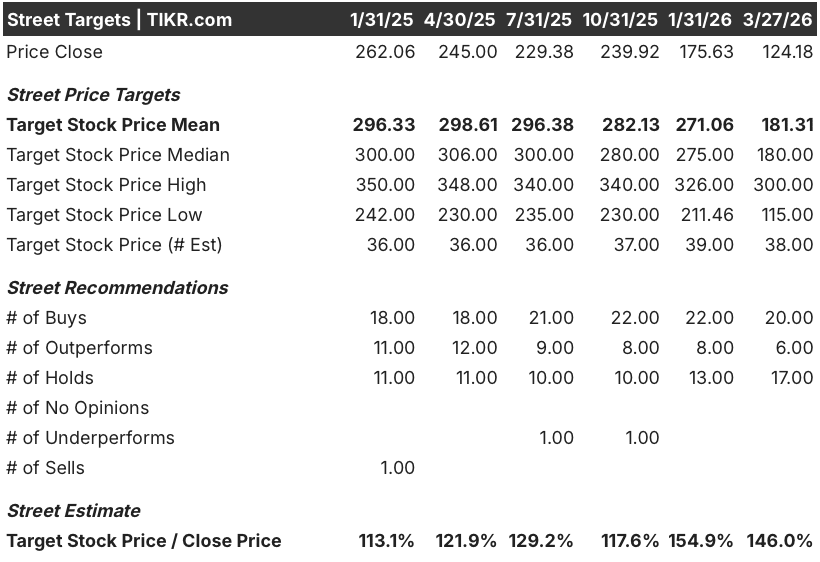

Twenty analysts carry buy or outperform ratings, 17 hold, and the mean price target of $181.31 across 38 estimates implies roughly 46% upside from $124.18, reflecting Street conviction that Flex Credits consumption growth and agentic AI adoption will reaccelerate top-line momentum.

The analyst price target range spans $115.00 on the low end to $300.00 on the high, where the bear case hinges on further deal elongation in federal and healthcare markets and the bull case rests on second-half Flex Credits adoption confirming a durable consumption revenue model.

What Does the Valuation Model Say?

The TIKR mid-case target of $217.74, implying a 75.3% total return and 12.3% annualized IRR over 4.8 years, is built on 10.3% revenue CAGR supported by the agentic AI pipeline already in early access and a net income margin expanding from 25.9% in FY2026 to 27.7% by FY2031.

The market is pricing structural impairment, yet WDAY generated $2.78 billion in free cash flow in FY2026 with a 29.1% FCF margin, a cash profile inconsistent with a business in secular decline.

The 97% gross revenue retention rate and $28.1 billion total subscription backlog confirm the core is not eroding, supporting the TIKR target of $217.74 as the agentic layer compounds on an already locked-in revenue base.

Bhusri stated directly on the Q4 earnings call that he intends to “be conservative on the guide and then beat it,” a posture consistent with Workday’s historical pattern of underpromising on subscription revenue guidance.

Prolonged deal elongation in federal and healthcare markets, which drove Q4 net new ACV shortfall, represents the primary risk to the TIKR model’s 11.7% FY2027 revenue growth assumption if those pipelines do not convert.

Q1 FY2027 subscription revenue guidance of $2.335 billion, with cRPO growth expected between 14.5% and 15.5%, is the first confirmation point for whether Flex Credits adoption and pipeline conversion are tracking the TIKR model’s growth assumptions.

Should You Invest in Workday, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WDAY stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Workday, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WDAY stock on TIKR for Free →