Key Stats for Simon Property Group Stock

- 52-Week Range: $136.3 to $205.1

- Current Price: $190.2

- Street Mean Target: $206.3

- Street High Target: $250

- Valuation Model Target: $247.4

What Happened?

Simon Property Group (SPG), the largest mall REIT in the United States, confronted its most significant leadership transition in three decades when founder and longtime CEO David Simon died on March 23, with SPG stock trading near $190.

The board immediately appointed Chief Operating Officer Eli Simon as CEO and President, while naming director Larry Glasscock non-executive chairman, a succession that markets absorbed without a sustained selloff given Eli’s decade-long operational role.

The leadership transition arrived against a record operational backdrop: SPG generated $4.8 billion in Real Estate FFO (funds from operations, the REIT equivalent of operating earnings) for FY2025 and executed over 17 million square feet of leases across its 254-property portfolio.

Simon stated at Citi’s Miami Global Property CEO Conference on March 3 that “our pipeline is up about 15% over last year” and “that’s really broad-based across all categories,” tying accelerating leasing demand directly to SPG’s ongoing redevelopment of Taubman Realty Group assets acquired for $2 billion in 2025.

A $4 billion shadow development pipeline anchored by mixed-use transformations at Boca Raton’s Town Center and San Diego’s Fashion Valley, combined with a new $2 billion share repurchase program and a Q1 2026 dividend raised 4.8% to $2.20 per share, positions SPG for durable compounding well beyond the near-term leadership noise.

Wall Street’s Take on SPG Stock

The Taubman consolidation, Boston’s Copley Place redevelopment, and accelerating leasing demand all point to the same thesis: SPG is executing a quiet portfolio upgrade that will push NOI materially higher as $1.5 billion in active development delivers over the next two to three years.

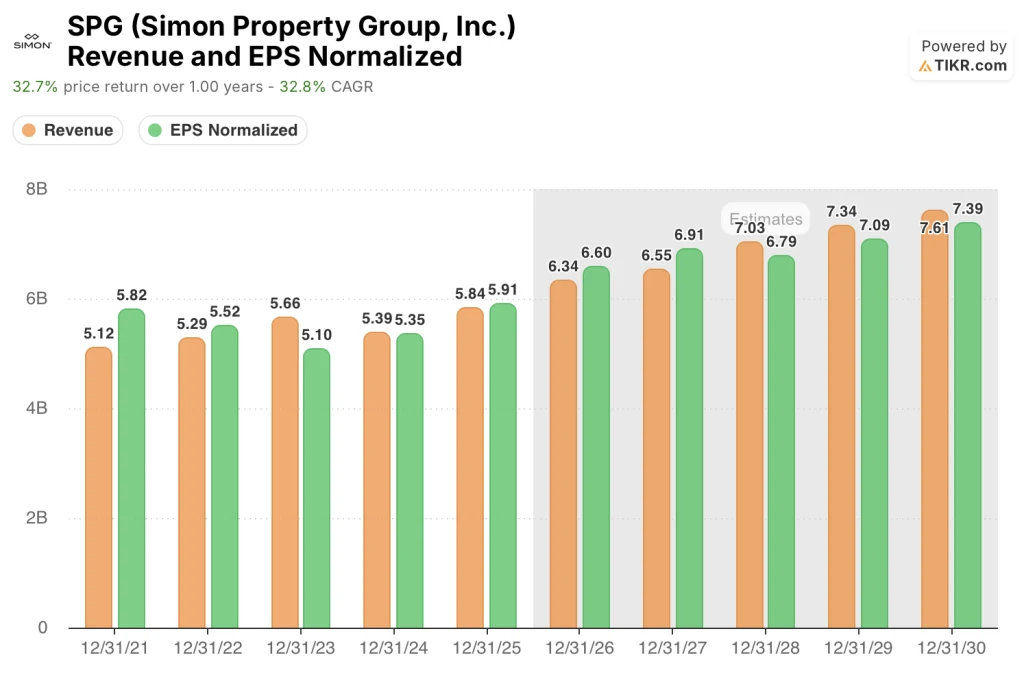

SPG’s consensus estimate calls for revenue of $6.34 billion in 2026, rising to $7.61 billion by 2030, while normalized EPS climbs from $5.91 in 2025 to an estimated $6.60 in 2026, both trajectories anchored by management’s confirmed guidance of at least 3% domestic property NOI growth and a 15% year-over-year increase in the leasing pipeline.

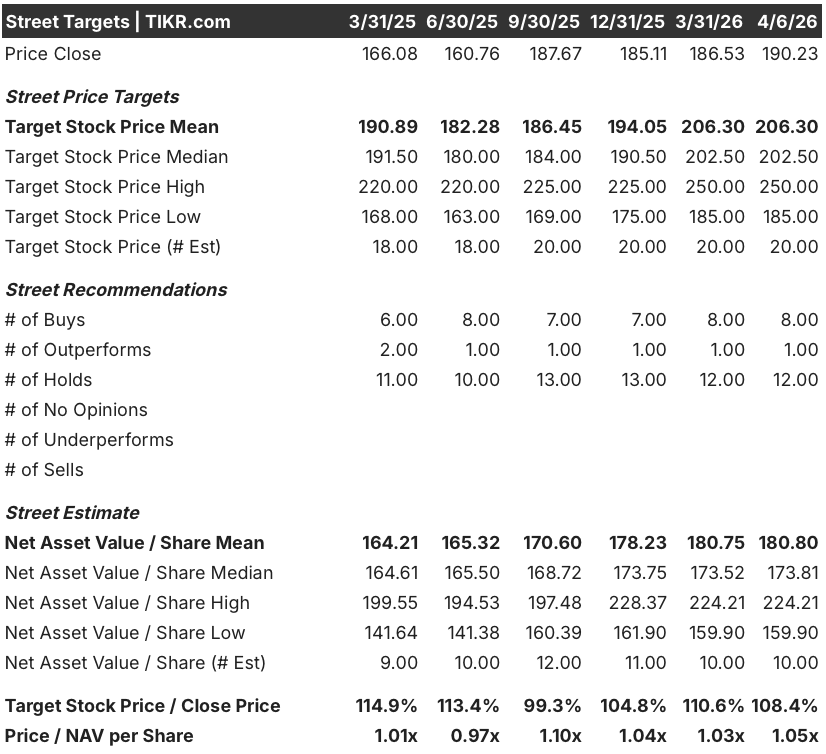

Nine analysts carry buy or strong buy ratings on SPG and 12 hold neutral positions, with no sells, a mean price target of $206.30, and a street high of $250, reflecting Wall Street’s consensus that the company’s redevelopment execution needs to prove out before the multiple re-rates.

The $206.30 mean target implies roughly 8.4% upside from current levels, but the $250 street high suggests a credible bull case tied specifically to NOI accretion from the $4 billion shadow pipeline materializing faster than the base case assumes.

Trading at 1.05x estimated NAV of $180.80 per share, SPG stock appears fairly valued on a trailing basis, but that multiple understates the forward picture: portfolio NOI grew 4.7% in 2025 and management has guided to continued acceleration in 2026, meaning today’s NAV anchor is already stale relative to where earnings are heading.

Simon’s statement that SPG generates “over $1.5 billion in excess of our dividend each year” reframes the capital return story, signaling that the new $2 billion buyback program is structurally fundable without incremental leverage.

If Saks Global’s bankruptcy resolution drags into 2027 and delays anchor re-tenanting across multiple premium properties, near-term NOI accretion from those boxes will be back-end weighted, pressuring the 2026 FFO range.

Q1 2026 earnings, expected in early May, will be the first real test of Eli Simon’s leadership continuity, with the number to watch being domestic property NOI growth versus the 3% floor management guided.

Simon Property Group Financials

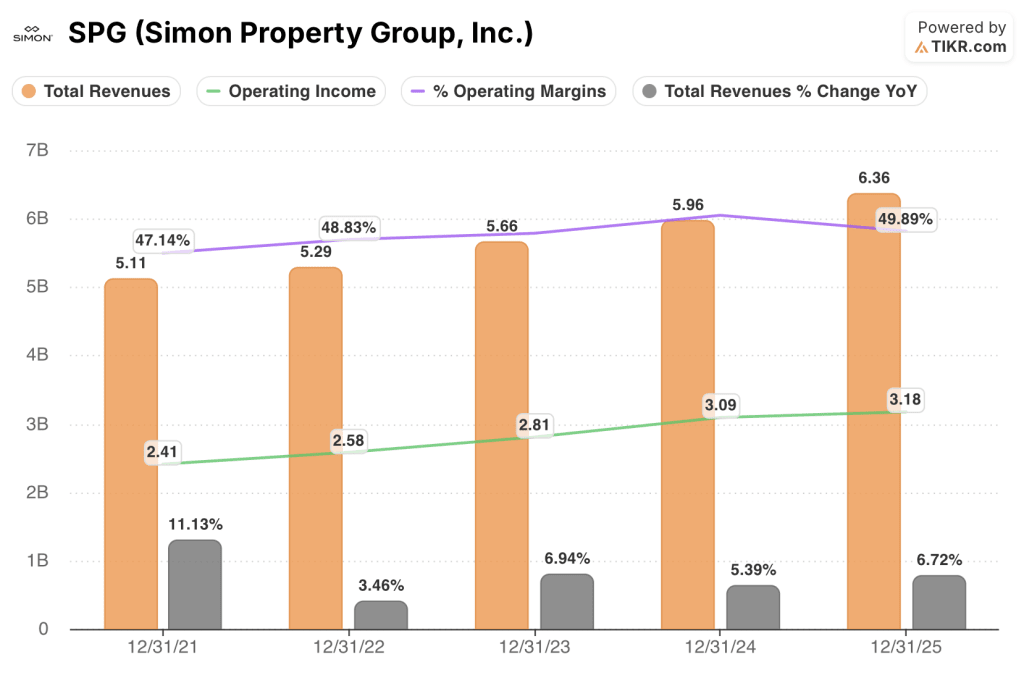

SPG grew total revenues 6.7% year-over-year to $6.36 billion in FY2025, the fastest top-line growth rate in the four-year dataset and the clearest confirmation that the company’s premium mall and outlet platform is accelerating rather than plateauing.

Rental revenues, which form the core of SPG’s income stream and reflect the contractual base rents across its U.S. malls, premium outlets, and mills portfolio, rose from $5.39 billion in 2024 to $5.84 billion in 2025, driven directly by the Taubman Realty Group consolidation and a 4.7% increase in average base minimum rent per square foot.

Operating income reached $3.18 billion in 2025, holding the operating margin at 49.9% despite total operating expenses rising to $3.19 billion, a reflection of the one-time integration costs embedded in property expenses and SG&A that will compress as Taubman assets stabilize.

The operating margin trajectory over the past four years — 47.1% in 2021, 48.8% in 2022, 49.6% in 2023, 51.9% in 2024, and 49.9% in 2025 — reveals that the 2025 margin dip is acquisition-related rather than structural, and the underlying trend points toward recovery as the Taubman integration matures and the redevelopment pipeline converts to income

What Does the Valuation Model Say?

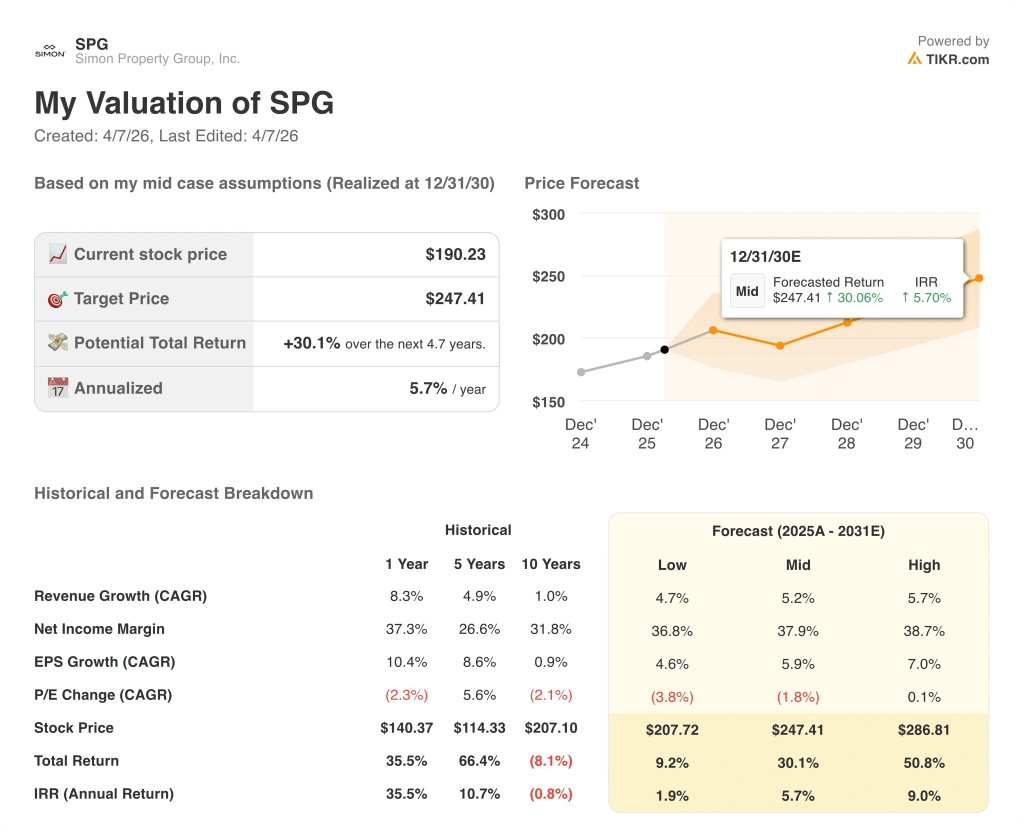

TIKR’s model assigns SPG a mid-case target price of $247.41 by December 2030, implying a 30.1% total return over 4.7 years, anchored by a revenue CAGR assumption of 5.2% that aligns precisely with management’s confirmed guidance of at least 3% domestic NOI growth plus the incremental contribution from $1.5 billion of active development currently yielding 9%.

SPG appears undervalued at current levels, with the $247.41 mid-case target supported by an EPS CAGR of 5.9% through 2030 against a stock price that has moved sideways relative to improving fundamentals over the past year.

The central tension in the SPG investment case is whether the $4 billion shadow pipeline converts to income on schedule or faces the permitting and municipal approval delays that Eli Simon explicitly flagged, with most major starts expected in 2027 and 2028.

Bull Case

- Active $1.5 billion development pipeline delivers at the guided 9% blended yield, contributing an estimated $30 million incremental NOI in 2026, with the larger $4 billion shadow pipeline beginning to start construction in 2027 and 2028 across flagship mixed-use projects at Boca Raton and Fashion Valley

- Saks Off Fifth lease recapture converts 38 rejected leases paying $18 million into a $30 million-plus rent roll at premium outlet locations, with David Simon confirming on the Q4 call that half the portfolio is already tracking to that number and the remaining boxes generating additional upside into 2027

- Taubman integration costs burn off as three legacy assets — Green Hills, Cherry Creek, International Plaza — begin $250 million in redevelopments in 2026, normalizing operating margins back toward the 51.9% peak reached in 2024

- Simon+ loyalty program, launched November 2025 with 25 million consumers in its database, begins generating retail media revenue at scale, adding a high-margin ancillary income stream not currently embedded in consensus estimates

Bear Case

- Tariff-driven retailer margin compression triggers a second wave of tenant stress beyond Saks and Catalyst Brands, where a one-time Catalyst restructuring charge already clipped Q4 2025 FFO by $0.31 per share, and David Simon acknowledged on the Q4 call that the full tariff impact will be felt in 2026

- City planning and entitlement timelines push shadow pipeline starts past 2028, keeping $4 billion of NOI-generating capital on the sidelines and deferring the re-rating catalyst the street needs to move price targets toward the $250 high

- The 1.05x Price/NAV multiple contracts toward the 0.97x trough seen in mid-2025 if broader REIT sentiment deteriorates under sustained elevated interest rates, with SPG’s CFO confirming on the Q4 call that the company still faces higher coupons on debt rolling off legacy low-rate paper

- Leadership transition execution risk concentrates in 2026, with Eli Simon managing his first full fiscal year as CEO while simultaneously integrating Taubman, delivering active redevelopments, and navigating the Saks bankruptcy resolution across a 254-property portfolio

Should You Invest in Simon Property Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SPG stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Simon Property Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SPG stock on TIKR for Free →