Key Stats for Microsoft Stock

- Pre-Market Price change for Microsoft stock: -6%

- $MSFT Share Price as of Jan. 28: $481

- 52-Week High: $555

- $MSFT Stock Price Target: $616

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

What Happened?

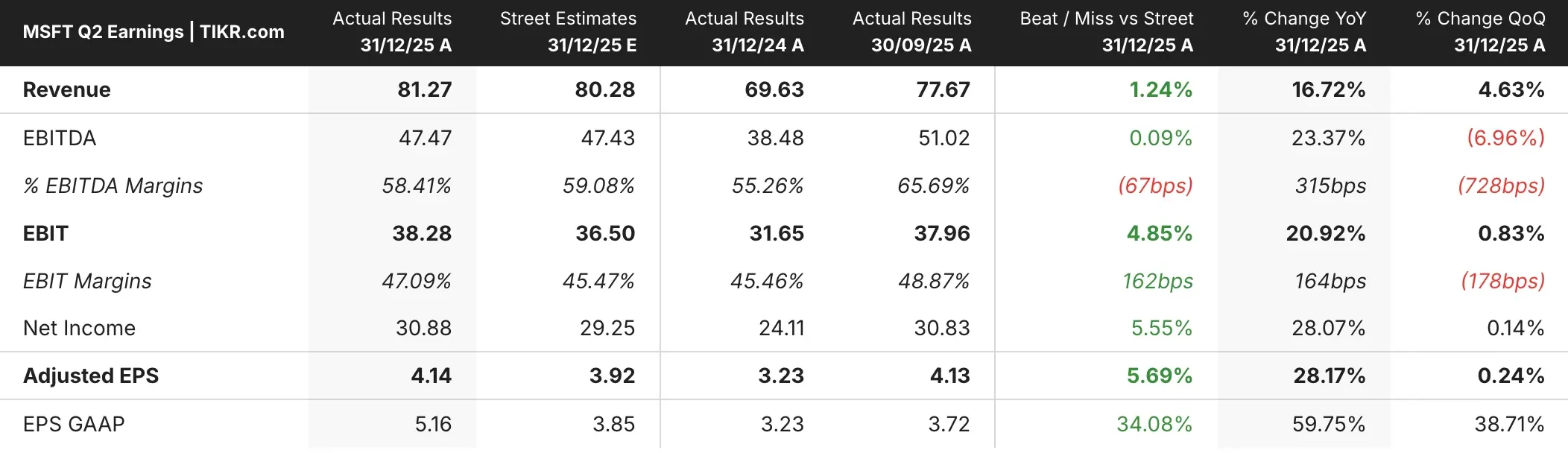

Microsoft (MSFT) stock is down 6% in pre-market despite beating Wall Street’s earnings expectations.

- The selloff in MSFT stock came as investors focused on slowing cloud growth and massive capital spending rather than the company’s strong quarterly results.

- The tech giant reported adjusted earnings of $4.14 per share, beating estimates of $3.92, while revenue came in at $81.27 billion versus expectations of $80.28 billion.

- However, Azure cloud growth slowed to 39% from 40% in the previous quarter, raising concerns about the company’s ability to meet surging demand for AI infrastructure.

CEO Satya Nadella revealed that Microsoft added nearly one gigawatt of total capacity during the quarter alone.

But CFO Amy Hood acknowledged that “customer demand continues to exceed available supply,” forcing the company to make difficult allocation decisions between Azure customers, first-party AI products like Microsoft 365 Copilot and GitHub Copilot, and research and development teams.

Capital expenditures and finance leases totaled $37.5 billion in the quarter, up 66% year over year and well above analyst expectations of $34.31 billion.

This record spending reflects Microsoft’s aggressive push to build out AI infrastructure, but it also compressed gross margins to just over 68%—the narrowest level in three years.

See analysts’ growth forecasts and price targets for MSFT stock (It’s free!) >>>

What the Market Is Telling Us About MSFT Stock

The decline in Microsoft stock suggests investors are growing concerned about the return on the company’s unprecedented AI investments.

While revenue and earnings beat expectations, the combination of slowing Azure growth and ballooning capital spending has raised questions about profitability.

One particularly striking disclosure caught analysts’ attention:

- OpenAI now accounts for 45% of Microsoft’s $625 billion in remaining commercial performance obligations (RPO), which measure future contracted revenue.

- This heavy concentration creates significant risk if OpenAI fails to meet its ambitious financial targets.

“The backlog is really good, but the disclosure that OpenAI is 45% of their backlog goes back to the question: Can OpenAI achieve these financial goals to pay Oracle, Microsoft and many of the providers?” Jefferies analyst Brent Thill said on CNBC.

Hood pushed back against these concerns, noting that the remaining 55% of RPO—roughly $350 billion—is “larger than most peers, more diversified than most peers” and represents 28% growth.

She emphasized that Microsoft remains OpenAI’s “provider of scale” and expressed confidence in the partnership.

Microsoft stock has also been weighed down by capacity constraints.

- Hood explained that incoming GPU supply must be carefully balanced between serving Azure customers, powering first-party AI products, supporting R&D innovation, and replacing aging infrastructure.

- This means Azure growth is effectively capped by how much capacity Microsoft can allocate to third-party customers.

The company’s guidance for fiscal third-quarter Azure growth of 37% to 38% at constant currency met expectations but offered little upside surprise.

Meanwhile, the implied operating margin of 45.1% came in below the 45.5% consensus, as Microsoft continues to invest heavily in AI computing capacity and talent.

On a positive note, Microsoft 365 Copilot is gaining traction with 15 million paid seats—the first time the company has disclosed this metric.

With over 450 million total paid commercial Microsoft 365 seats, Copilot still has significant room for growth. The company also reported 4.7 million paid GitHub Copilot subscribers, up 75% year over year.

Microsoft now expects fiscal 2026 operating margins to be “up slightly” for the full year, a modest improvement from previous guidance.

However, rising memory prices could add volatility to both capital expenditures and cloud margins going forward.

Estimate a company’s fair value instantly (Free with TIKR) >>>

How Much Upside Does Microsoft Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!