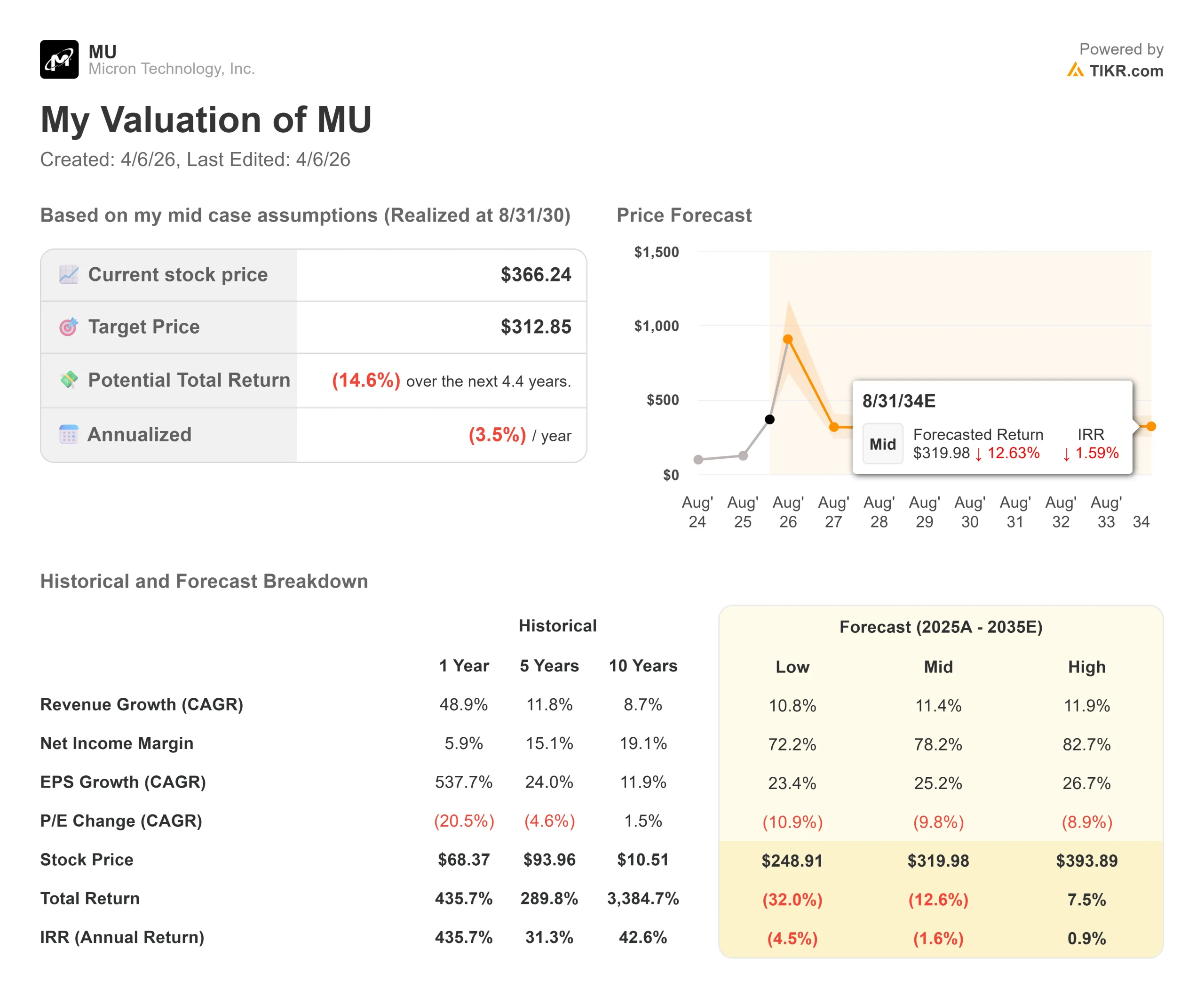

Key Stats for Micron Stock

- Current Price: $374.11

- Target Price (Mid): $312.85

- Street Target: $525.48

- Potential Total Return (Mid): (14.6%)

- Annualized IRR: (3.50%) / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Few stocks have whipsawed investors as violently as Micron Technology (MU) in the past three weeks.

On March 18, Micron delivered one of the strongest earnings beats in recent semiconductor history. Revenue nearly tripled year-over-year to $23.86 billion, non-GAAP EPS came in at $12.20 against a TIKR consensus estimate of $9.16, and management reported quarterly free cash flow of $6.9 billion, a company record.

Q3 revenue guidance came in at $33.5 billion, a figure Sanjay Mehrotra, Chairman, President and CEO, said on the earnings call, “exceeds the full year revenue for every year in our company’s history through fiscal 2024.” The stock fell 3.78% that day.

What followed was worse. On March 24, Google Research published TurboQuant, a compression algorithm its developers claim reduces the KV cache, the high-speed memory store that allows AI models to retrieve prior calculations without reprocessing them, by up to six times with no accuracy loss.

Memory stocks sold off immediately.

By March 30, Micron hit a maximum drawdown of 30.31% from its recent high on volume nearly double its three-month average. The AI memory trade, among the market’s most crowded bull positions entering 2026, was suddenly in question.

The rebound came quickly.

On April 1, shares surged as analysts pushed back on the demand-destruction thesis. Bank of America Securities analyst Vivek Arya argued that efficiency gains of this magnitude historically drive more usage rather than lower procurement, a version of the Jevons Paradox that has repeatedly held in semiconductor cycles.

Morgan Stanley reaffirmed its Overweight rating, calling the selloff excessive. As of April 6, MU trades at $374.11, roughly 16% above its March 30 trough but still 20.6% below its 52-week high of $471.34.

The question is whether, after a 30% crash, Micron finally represents real value.

See historical and forward estimates for Micron stock (It’s free!) >>>

Is Micron Undervalued Today?

On forward multiples, Micron looks startlingly cheap.

The stock trades at 2.93x NTM EV/EBITDA, against a peer group median of 14.15x across comparable semiconductor companies on TIKR. SK Hynix, Micron’s closest HBM (high-bandwidth memory, the premium memory type powering AI accelerator chips) competitor, sits at just 3.04x. Intel trades at 16.80x NTM EV/EBITDA despite substantially weaker margins. On NTM P/E, Micron is at 4.05x against a peer median of 24.44x.

These are the multiples of a business the market expects to mean-revert hard.

The bull case argues that mean-reversion may not arrive as quickly as those multiples imply.

Mark Murphy, Executive Vice President and CFO, told investors on the Q2 call that Micron “generated record free cash flow, reduced our debt and closed the quarter with the highest net cash position in our history,” ending Q2 with $16.7 billion in cash and a net cash balance of $6.5 billion. Gross margins reached 75% in Q2, and Q3 guidance calls for 81%, a figure that would have seemed implausible for a company historically treated as a commodity supplier.

DRAM inventory days remain below 120, supporting near-term pricing strength.

The structural demand case is harder to dismiss than the TurboQuant selloff implied.

Mehrotra told investors that AI demand is driving DRAM and NAND data center bit TAM (total addressable market, the overall revenue pool available) to exceed 50% of industry TAM for the first time in calendar 2026, with both AI and traditional server demand simultaneously constrained by supply.

Micron has begun volume shipments of HBM4 for NVIDIA’s Vera Rubin GPU platform and signed its first five-year SCA (strategic customer agreement, a long-term supply commitment beyond typical short-term contracts), signaling that at least one major customer has locked in supply at scale.

In robotics, Mehrotra described the category as a “20-year growth vector,” noting that humanoid robots will require compute platforms rivaling a Level 4 autonomous vehicle (full self-driving capability with no human input required), each demanding significant memory capacity.

The bears are not arguing with the direction of demand; they are arguing about duration. TurboQuant is still a laboratory result with no production deployment.

See how Micron performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $374.11

- Target Price (Mid): $312.85

- Potential Total Return: (14.6%)

- Annualized IRR: (3.50%) / year

See analysts’ growth forecasts and price targets for Micron stock (It’s free!) >>>

Even after a 30% crash, the TIKR mid-case model produces a target of $312.85 by August 31, 2030, a total return of (14.6%) and an annualized IRR of (3.50%) per year from the model entry price of $366.24. This is not a pessimistic model. It assumes 11.4% revenue CAGR through 2030, driven by HBM content growth and data center DRAM share gains, and projects net income margins reaching 72.2% (a model forecast assumption, not a near-term figure). The problem is P/E multiple compression: the model assumes P/E contracts at a (9.8%) CAGR as the cyclical peak fades and the market re-rates memory toward commodity pricing. That re-rating absorbs the earnings growth and leaves the investor underwater.

The high case offers more comfort, but not much. Under bull assumptions, 11.9% revenue CAGR and 82.7% net income margins, the model yields $393.89 by 8/31/30, a total return of 7.5% and an IRR of 0.9%. The Street consensus target of $525.48 implies a far more optimistic multiple outcome than either TIKR scenario captures. That gap is the whole debate: if the market re-rates memory as a sustainably high-margin strategic asset, the Street wins. If history repeats and margin compression follows the capex cycle, the TIKR model is closer to right.

Of 46 analysts covering the stock, 28 rate it Buy, 10 Outperform, 5 Hold, 1 Underperform, and 1 Sell. The primary upside risk to the TIKR model is that if Micron sustains gross margins above 70% through the next cyclical trough, the multiple compression assumption breaks down and the stock is significantly undervalued at current prices. The primary downside risk is that the fiscal 2027 capex step-up coincides with a demand air pocket, forcing simultaneous margin compression and inventory build.

Conclusion: Watch Q3 FY2026 non-GAAP gross margin against the 81% guidance when Micron reports in late June 2026. At or above 81%, HBM pricing power is intact and the TurboQuant selloff was the overreaction most analysts believe it was. Below 80%, the burden of proof shifts back to the bulls.

Micron is a genuine AI infrastructure beneficiary, the only U.S.-based advanced memory manufacturer, and a company that just delivered the most profitable quarter in its history. At $374, the TIKR mid-case model cannot justify it on a total return basis through 2030. Both of those things are true simultaneously.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Micron?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Micron, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Micron alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!