Key Stats for Lockheed Martin Stock

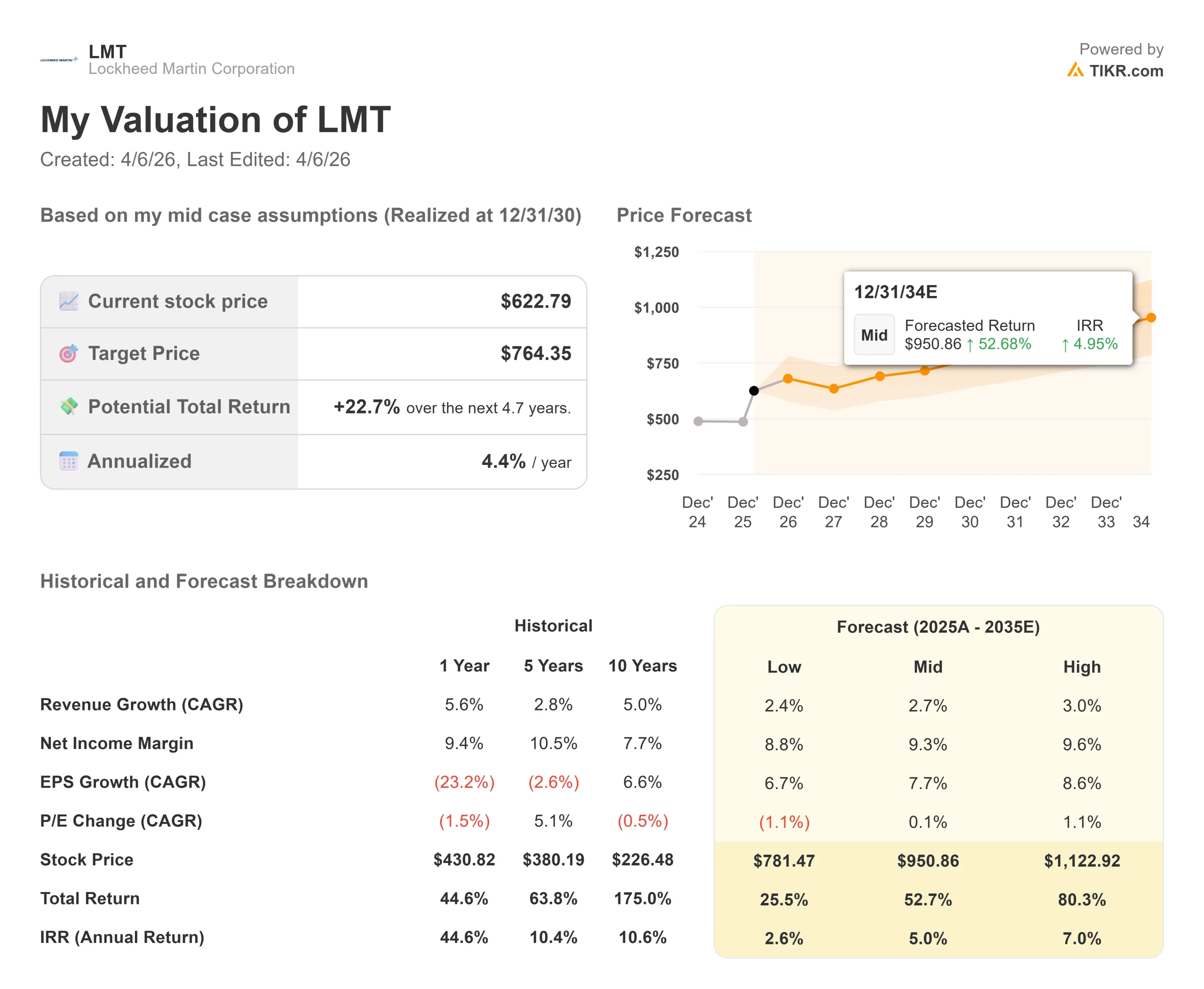

- Current Price: $622.79

- Target Price (Mid): $764.35

- Street Target: $665.65

- Potential Total Return: +22.7%

- Annualized IRR: 4.4% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

While the S&P 500 has churned through tariff fears and macro uncertainty this year, Lockheed Martin (LMT) has climbed more than 26% year to date, making it one of the clearest safe-haven trades in a turbulent market.

Bulls argue the world has entered a durable rearmament cycle and that Lockheed sits at the center of it. Bears counter that 20.81x NTM earnings leave little room for execution risk after a move this large.

When Chairman, President, and CEO Jim Taiclet reported full-year 2025 results on January 29, the company posted a record $194 billion backlog, 6% year-over-year sales growth, and free cash flow above prior expectations.

The stock gained 1.88% on earnings day.

Taiclet described it as “a year of unprecedented demand for Lockheed Martin capabilities.” The $194 billion backlog, roughly 2.5 times annual revenue, means most of the company’s top line through 2027 is already contractually committed.

What followed that call accelerated the thesis.

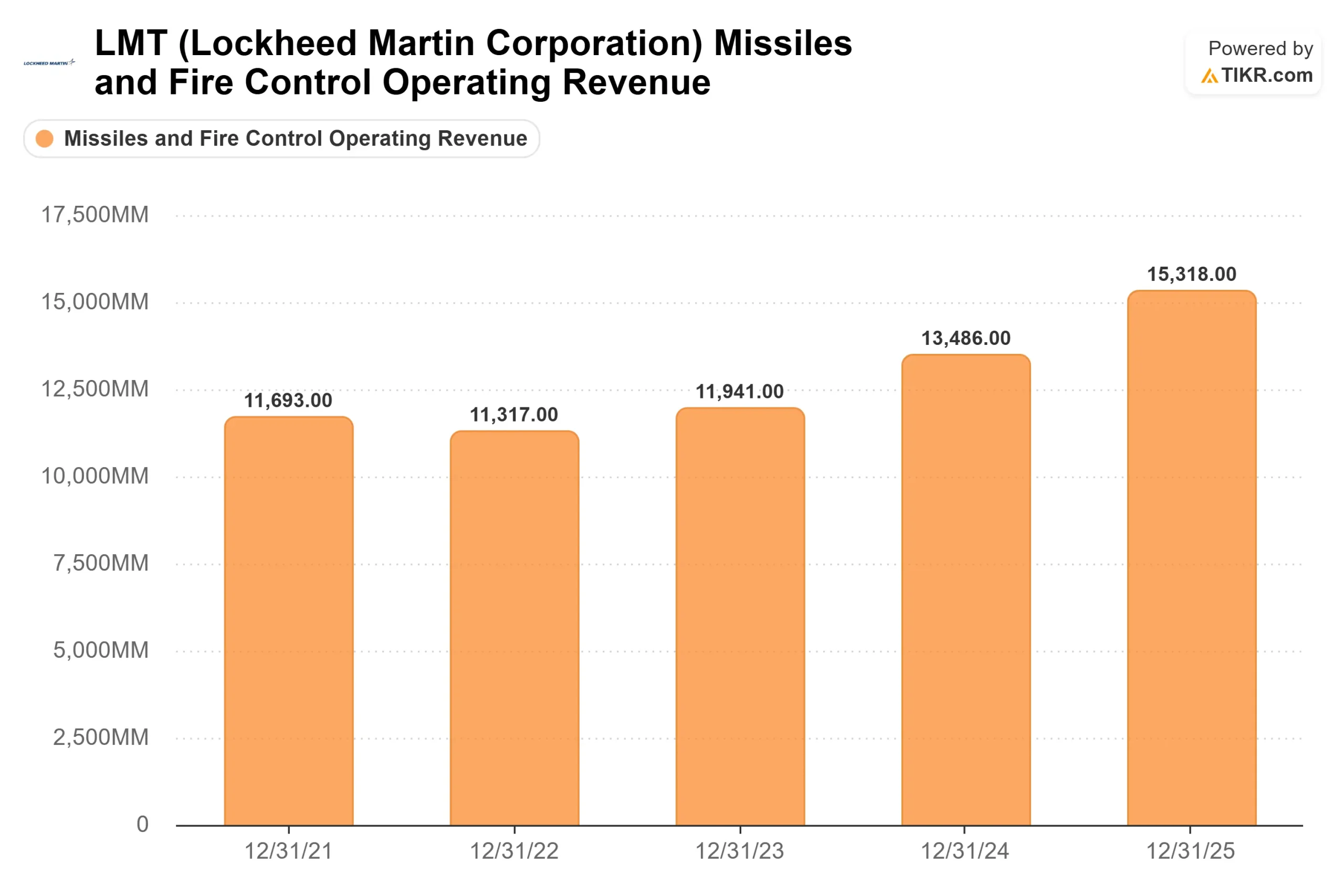

In January, Lockheed signed a framework agreement with the U.S. government to increase annual PAC-3 MSE (Missile Segment Enhancement, a hit-to-kill interceptor) production capacity from approximately 600 to 2,000 interceptors per year under a seven-year term.

In late March, Lockheed and the Department of War announced a framework to quadruple Precision Strike Missile (PrSM) production capacity, building on a prior $4.94 billion U.S. Army contract.

Both are framework agreements requiring Congressional appropriations and final contract definitization before they become binding. They represent committed intent, not booked revenue.

See historical and forward estimates for Lockheed Martin stock (It’s free!) >>>

Is Lockheed Martin Undervalued Today?

At $622.79, LMT trades at 20.81x NTM normalized earnings and 14.37x NTM EBITDA. Both are near multi-year highs.

LMT does not look obviously expensive. General Dynamics (GD) trades at 21.35x NTM P/E and RTX Corporation at 28.75x. The median NTM P/E across TIKR’s 37-company aerospace and defense peer group is 28.75x, meaning LMT actually trades at a discount to the sector median.

The discount reflects LMT’s lower near-term revenue growth rate, currently tracking at 5.6% in 2025, versus faster-growing peers that have re-rated more aggressively.

The near-term margin picture is the most credible bear argument.

On the earnings call, CFO Evan Scott acknowledged that the start-up nature of production ramps in Missiles and Fire Control creates near-term margin dilution risk as Lockheed builds new facilities and scales a workforce across five states. Management guided for approximately 25% segment operating profit growth in 2026, but that growth is coming off a compressed base, not a healthy one, and is contingent on ramps executing on schedule.

The demand side is harder to argue against. The Trump administration has proposed a defense budget of up to $1.5 trillion for 2027, up from $900 billion appropriated for 2026, a proposal still requiring Congressional approval, but one that signals the direction of spending.

Domestically, TIKR’s segment data shows U.S. revenue accounted for $53.7 billion of LMT’s $75.0 billion total 2025 revenue, roughly 71.6% of the top line. International exposure, primarily through F-35 export relationships with European NATO allies, adds a secondary tailwind as European defense budgets continue breaking records.

Aeronautics revenue reached $30.6 billion in 2025, underpinned by a record 191 F-35 deliveries for the year, with sustainment demand growing as the installed fleet expands.

See how Lockheed Martin performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $622.79

- Target Price (Mid): $764.35

- Potential Total Return: +22.7%

- Annualized IRR: 4.4% / year

See analysts’ growth forecasts and price targets for Lockheed Martin stock (It’s free!) >>>

The TIKR mid-case model targets $764.35 by December 31, 2030, built on a 2.7% revenue CAGR and a 9.3% net income margin. The two revenue drivers are steady F-35 production and sustainment in Aeronautics, and the multi-year MFC ramp as PAC-3 and PrSM framework agreements convert to contracted deliveries. The margin driver is operating leverage as higher-volume programs scale through their start-up phases.

At 4.4% annualized, the mid-case return is honest: LMT offers exceptional business quality and backlog visibility, but moderate IRR after a 26% run. The upside case requires missile ramps to execute ahead of schedule and defense budgets to exceed current proposals. The downside case is not a business collapse, it is stalled appropriations, continued margin compression, and multiple mean-reversion, leaving the stock flat for years while the fundamentals slowly catch up to the price.

One execution risk worth flagging: Taiclet acknowledged on the earnings call that Lockheed’s classified Aeronautics program carries ongoing design and integration risk over the next few years, though no additional charges were recorded in Q4 2025 and executive leadership is directly monitoring the program. A surprise charge there would be the most likely single catalyst for a meaningful pullback.

Conclusion: At Q1 2026 earnings on April 23, the number to watch is the Missiles and Fire Control segment operating margin. If start-up dilution is worse than guided, it puts the full-year operating profit target at risk and raises questions about the missile growth timeline. If MFC margins hold near their 2025 level, the bull thesis is running ahead of schedule.

LMT is a high-quality business with a $194 billion backlog and durable demand tailwinds. At $622.79, it offers a reasonable return for long-term patient investors. The 26% YTD run has already captured most of the near-term upside, and the next leg depends on clean execution.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Lockheed Martin?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lockheed Martin, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lockheed Martin alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Lockheed Martin on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!