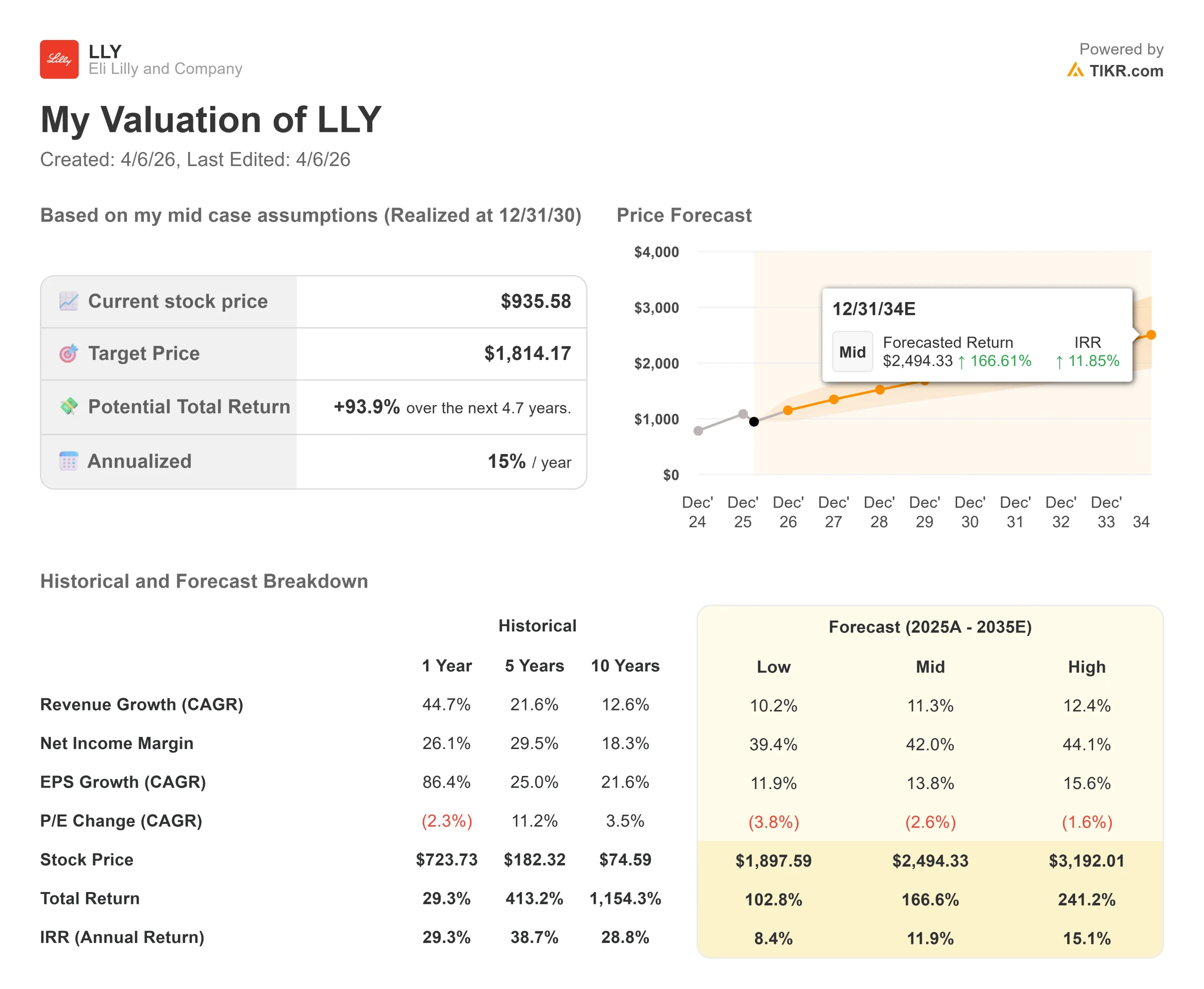

Key Stats for Eli Lilly Stock

- Current Price: $932.84

- Target Price (Mid): $1,814.17

- Street Target: $1,209.21

- Potential Total Return: +93.9%

- Annualized IRR: 15.00% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Eli Lilly (LLY) has shed over 13% since January 1, even as revenue grew 44.7% in 2025 and the company launched what may be its most commercially significant product in years.

Bulls point to a market where obesity drug penetration sits at mid-single digits and a pipeline with multiple active Phase 3 programs. Bears point to pricing pressure from the Trump administration, looming pharmaceutical tariffs, and a 2026 guidance range that disappointed parts of Wall Street.

The unresolved question is whether LLY has already priced in the bad news or whether the headwinds are still arriving.

The immediate catalyst is Foundayo, Lilly’s brand name for orforglipron, a once-daily oral GLP-1 receptor agonist (a pill that mimics appetite-regulating hormones) approved by the FDA on April 1 and shipping as of today. Shares rose roughly 4% on the approval.

In the ATTAIN-1 trial, participants on the highest dose lost an average of 27.3 pounds (12.4% of body weight) compared to 2.2 pounds for the placebo group. Unlike earlier oral GLP-1 formulations, Foundayo requires no food or water restrictions at dosing. It is priced at $25 per month for commercially insured patients and $149 for self-pay individuals.

Q4 2025 earnings, reported February 4, were strong on paper, but the stock fell 7.79% on the day. Revenue reached $19.29 billion, beating the consensus estimate of $17.94 billion by over $1.3 billion, while adjusted EPS of $7.54 topped the average estimate of $6.91.

The sell-off reflected concern that the 2026 guidance range of $80 billion to $83 billion in revenue and $33.50 to $35.00 in non-GAAP EPS was insufficiently aggressive.

On the call, CEO David Ricks said the company “delivered robust revenue growth, advanced our pipeline, expanded our manufacturing footprint, and helped over 70 million people around the world” in 2025.

Foundayo lands in a difficult policy environment. Lilly has publicly opposed pharmaceutical tariffs, stating that broad tariffs “would raise costs, limit patient access, and undermine American leadership, especially for companies already investing heavily in domestic manufacturing.”

CEO Ricks has also pushed back against codifying most-favored-nation (MFN) drug pricing, a policy that would tie U.S. prices to the lowest prices charged in other developed countries, into law.

The tension between operational momentum and policy risk defines where the stock sits today.

See historical and forward estimates for Eli Lilly stock (It’s free!) >>>

Is Eli Lilly Undervalued Today?

At $932.84, LLY trades at 26.99x NTM P/E (price-to-earnings) and 21.41x NTM EV/EBITDA.

That multiple carries a significant premium relative to peers.

Roche trades at 10.89x NTM EV/EBITDA and 15.64x NTM P/E. Novo Nordisk, Lilly’s most direct GLP-1 competitor, trades at 8.44x NTM EV/EBITDA and 11.33x NTM P/E.

Whether Lilly’s premium holds depends almost entirely on how much incremental revenue its oral obesity franchise can generate from a market that remains underpenetrated.

The case for the premium is grounded in scale and access.

Foundayo targets patients that injectables cannot easily reach: the needle-averse, the schedule-constrained, and patients priced out of branded pens. Some Wall Street analyst projections put Foundayo’s long-term peak sales above $40 billion, with 2026 estimates ranging from $1.5 billion to $2.8 billion.

To avoid the supply shortages that plagued injectable rollouts, Lilly pre-built $1.5 billion in Foundayo inventory ahead of today’s launch.

The risk case has two legs.

First, pricing policy: MFN drug pricing and pharmaceutical import tariffs both create margin uncertainty that is difficult to model precisely.

Second, competition: Novo Nordisk published cross-trial data in early April claiming its oral Wegovy outperformed Foundayo on weight loss metrics. Cross-trial comparisons carry methodological limitations, but they shape prescriber behavior.

The Centessa Pharmaceuticals acquisition, valued at up to $7.8 billion including contingent payments, adds near-term debt and integration complexity as Lilly diversifies into sleep and wake disorders.

On the Q4 call, Chief Scientific Officer Dr. Daniel Skovronsky described three distinct incretin platforms moving forward simultaneously: tirzepatide, orforglipron, and retatrutide, alongside two additional Phase 3 programs, oloralintide and brinepatide, each targeting separate metabolic mechanisms.

A company with this pipeline depth rarely trades cheaply.

The question is whether “expensive relative to peers” and “poor risk-reward at today’s price” are the same thing.

See how Eli Lilly performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $932.84

- Target Price (Mid): $1,814.17

- Potential Total Return: +93.9%

- Annualized IRR: 15.00% / year

See analysts’ growth forecasts and price targets for Eli Lilly stock (It’s free!) >>>

The TIKR mid-case model projects LLY at $1,814.17 by December 31, 2030, a total return of +93.9% and an annualized IRR of 15.00% per year from today’s price.

The two primary revenue drivers are Mounjaro and Zepbound’s continued global expansion and Foundayo’s commercial ramp. The model assumes a revenue CAGR of 11.3%, grounded in management’s 2026 guidance midpoint of $81.5 billion. The margin driver is operating leverage: LTM gross margin stands at 83.0%, and the mid case assumes net income margins of 42.0% as the manufacturing infrastructure built since 2020 generates returns at scale. Free cash flow is projected to grow from $9.0 billion in 2025 to $47.4 billion by 2030E.

The high case (12.4% revenue CAGR, 44.1% net income margins) yields a target of $3,192.01 and a total return of 241.2% by December 31, 2030. That scenario requires Foundayo to achieve blockbuster scale and retatrutide to reach broad commercial approval within the decade.

The primary downside risk: if MFN pricing is codified, if Novo Nordisk captures dominant oral GLP-1 market share, or if obesity market growth disappoints the mid-single-digit penetration thesis, the 11.3% revenue CAGR assumption comes under pressure. The low case still projects a target of $1,897.59 and an IRR of 8.4% per year.

Conclusion: Watch Foundayo’s first disclosed revenue figure at Lilly’s next earnings report, confirmed for April 30, 2026. Any result approaching $500 million for a partial first quarter would signal the oral GLP-1 market is expanding faster than base-case assumptions.

Lilly grew revenue 44.7% in 2025, is launching its biggest new product today, and trades 17.7% below its 52-week high. The TIKR model projects a 15.00% annualized return through 2030 under the mid-case scenario. Whether that materializes depends most on how the oral obesity market develops and whether pricing policy pressure remains manageable.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Eli Lilly?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Eli Lilly, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Eli Lilly alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Eli Lilly on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!