Key Stats for International Business Machines Stock

- 52-Week Range: $221 to $325

- Current Price: $238

- Street Mean Target: $309

- Street High Target: $390

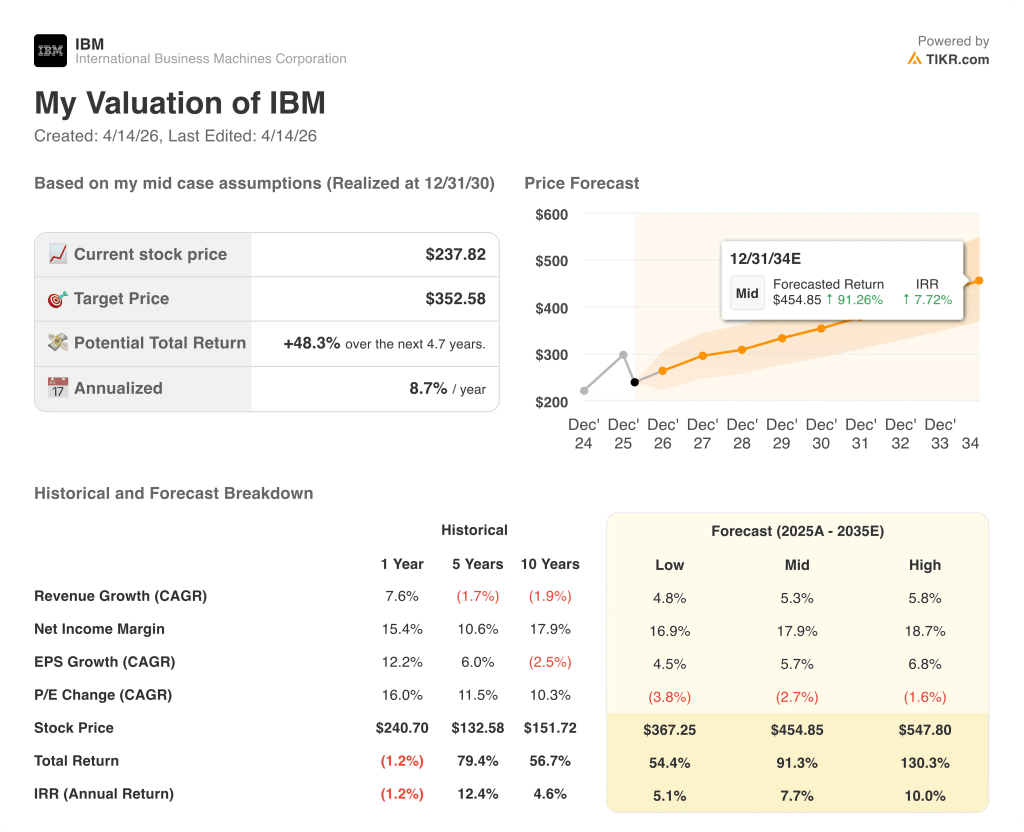

- TIKR Model Target (Dec. 2030): $353

What Happened?

International Business Machines (IBM), a 114-year-old enterprise technology company that sells hybrid cloud infrastructure, AI software, and consulting services to the world’s largest corporations, ended 2025 with its strongest free cash flow generation in over a decade, yet IBM stock has fallen roughly 22% year-to-date on fears that have more to do with narrative than fundamentals.

The selloff accelerated on February 24 after AI lab Anthropic announced that its Claude Code tool could modernize COBOL, a programming language that runs on IBM mainframe computers, the company’s massive-scale transaction processing hardware used by banks, insurers, and governments worldwide.

IBM shares plunged 13.2% that session, their steepest single-day drop since October 2000, though the stock recovered most of the move within two trading days after IBM’s software chief Rob Thomas publicly argued that COBOL translation misses the point: the mainframe’s value is its integrated hardware-software architecture, resilience at nine-nines uptime, and lowest unit cost for high-volume transaction workloads, not the language running on top of it.

Underneath the noise, IBM’s 2025 operating results told a materially different story: total revenue grew 7.6% to $67.54 billion, the software segment reached 9% growth for the year (its highest annual rate on record), and the company’s z17 mainframe posted its strongest start in any product cycle in roughly 20 years.

On March 17, IBM closed its $11 billion all-cash acquisition of Confluent, a real-time data streaming platform built on Apache Kafka used by more than 6,500 enterprises including 40% of the Fortune 500, adding a critical layer to IBM’s hybrid AI strategy by moving trusted data continuously across cloud and on-premise systems for analytics and AI agent workflows.

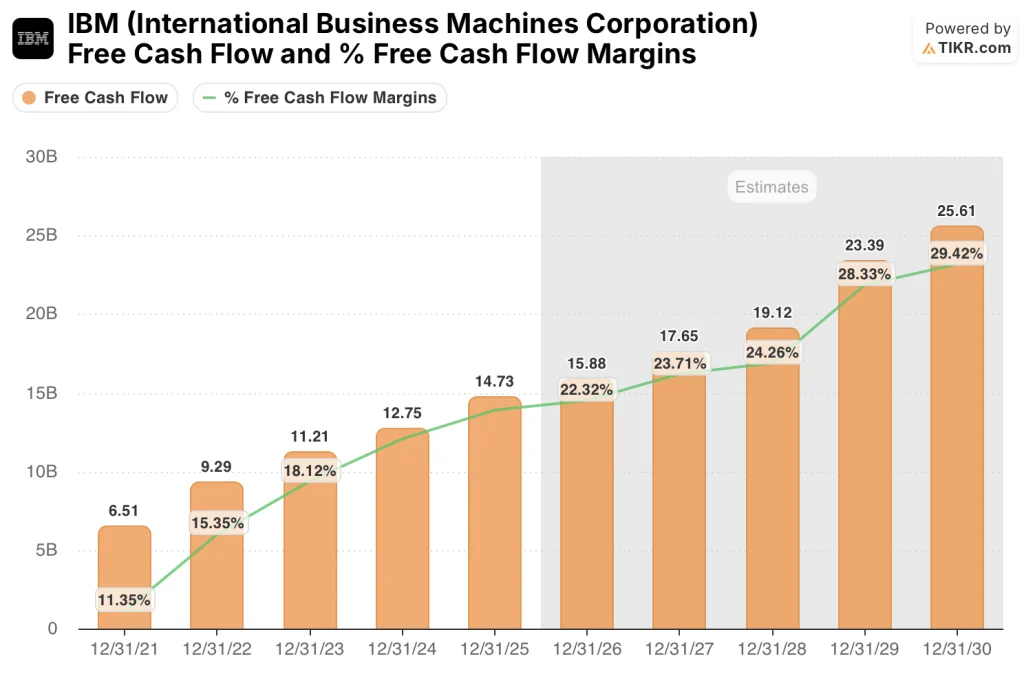

Arvind Krishna, IBM’s Chairman, President and CEO, stated on the Q4 2025 earnings call that “we are excited about the progress we made in 2025, delivering 6% revenue growth, our highest level of revenue growth in many years and $14.7 billion of free cash flow, our highest level of cash generation in over a decade,” tying the result directly to the company’s multi-year strategic repositioning toward software-led, hybrid cloud and AI platform economics.

The cumulative generative AI book of business across software and consulting reached $12.5 billion exiting 2025, with IBM guiding for software segment revenue growth of 10% in 2026, an acceleration that management says is anchored to recurring revenue compounding, Confluent synergies, and an expanding enterprise AI platform that now processes more than 12.5 billion AI-related transactions daily on the z17 mainframe.

Wall Street’s Take on IBM Stock

IBM’s record $14.7 billion free cash flow in 2025 was not a one-time event: it was the third consecutive year of double-digit FCF growth, and the company has guided for a further $1 billion increase in 2026, compounding a cash generation engine that the stock’s 22% YTD drawdown has simply failed to price.

IBM’s free cash flow grew 15.6% to $14.73 billion in 2025, reaching a free cash flow margin of 21.8%, the highest in the company’s reported history, driven by software mix expansion and the $4.5 billion annual run-rate productivity savings IBM has accumulated since 2022 through internal AI deployment.

Consensus estimates project FCF rising to around $16 billion in 2026 as Confluent absorbs roughly $600 million of dilution that is already baked into guidance.

Ten outright buys and two outperforms from a 20-analyst coverage group point toward a mean target of $309 with the stock trading at $238, a 30% implied upside that has widened sharply since the February selloff; analysts are specifically waiting for Q1 2026 results on April 22 to confirm whether software acceleration to double-digit growth is tracking against the 10% full-year guide.

The $172 spread between the $218 low target and the $390 high target reflects a genuine debate about Confluent: bears anchor near the low on $600 million of confirmed 2026 dilution and a consulting business that grew just 1% in Q4 2025, while bulls near the high expect Confluent’s real-time data platform to accelerate IBM’s watsonx AI agent revenue the same way HashiCorp accelerated automation bookings by delivering EBITDA accretion ahead of schedule within its first full year inside IBM.

With FCF growing at a 16% rate in 2025 and the market implying a P/FCF multiple below 15x on 2026 consensus of around $16 billion, a level that sits below IBM’s own 5-year average P/FCF and well below the multiple the company commanded when FCF margins were meaningfully lower, IBM stock appears undervalued at a time when the business is generating cash at the highest margin in its history.

IBM’s internal deployment of Project Bob, an AI-based software development system using frontier models including Anthropic Claude, is delivering 45% productivity gains across 20,000 IBM developers, a client-zero proof point that is not yet reflected in consensus Consulting margin estimates.

If Confluent integration stalls and the $600 million dilution drags into 2027 without the expected EBITDA accretion, the FCF growth case breaks and the re-rating thesis evaporates.

The April 22 Q1 2026 earnings call is the near-term test: watch for software segment revenue growth confirming the 10% full-year guide and any update on Confluent day-one revenue synergies.

International Business Machines Stock Financials

IBM generated $67.54 billion in total revenue in 2025, up 7.6% year-over-year, the sharpest annual growth rate the company has posted since at least 2018 and a meaningful acceleration from the 1.4% growth delivered in 2024.

The gross profit expansion tells the more important story: IBM’s gross profit grew 10.5% in 2025 to $39.30 billion, pushing gross margins to 58.2% from 56.7% the prior year, a 150-basis-point improvement that reflects the continued shift toward higher-margin software revenue now representing roughly 45% of the total business.

Operating income reached $12.57 billion in 2025, up 28.4% year-over-year, with operating margins expanding to 18.6% from 15.6% in 2024, the steepest single-year improvement in at least four years and a direct consequence of the software mix tailwind compounding alongside $4.5 billion in accumulated productivity savings.

R&D spending increased to $8.31 billion in 2025, up from $7.48 billion the prior year, as IBM invests in quantum computing, watsonx AI products, and hybrid cloud infrastructure at a pace that has grown total R&D spend by roughly $2.5 billion since 2019, building the innovation pipeline that supports the 10% software growth guide for 2026.

What Does the Valuation Model Say?

IBM’s TIKR mid-case model projects a target price of around $353, representing 48% total return from current levels over roughly 4.7 years, anchored to a revenue growth CAGR assumption of around 5% that aligns directly with the company’s stated Investor Day model and IBM’s 2025 actual revenue growth of 7.6%, which exceeded that pace.

At a P/FCF below 15x on record-margin cash generation compounding at double-digit rates, with $14.73 billion of 2025 actual FCF and consensus pointing toward around $16 billion in 2026, IBM stock appears undervalued against the durability of its cash engine and the still-unpriced revenue contribution from Confluent.

The IBM stock investment case does not turn on whether AI disrupts COBOL: it turns on whether Confluent replicates HashiCorp’s accretion playbook inside IBM’s go-to-market machine.

Bull Case: Confluent Follows the HashiCorp Playbook

- HashiCorp delivered EBITDA accretion ahead of schedule within its first full year inside IBM, the explicit template management cited when outlining Confluent expectations on the Q4 2025 earnings call

- IBM guided $500 million of operational spend run-rate synergies from Confluent by end of 2027, with revenue synergies from IBM’s global distribution of Confluent’s 6,500-enterprise installed base adding on top

- Software segment ARR exited 2025 at $23.6 billion, growing over $2 billion year-over-year, with Confluent not yet in the base; consensus projects software at around 10% growth in 2026 closing by midyear

- IBM’s FedRAMP authorization for 11 watsonx AI products on AWS GovCloud and the $151 billion SHIELD IDIQ defense contract open a federal revenue channel where Confluent’s real-time data streaming is immediately relevant

Bear Case: Dilution Drag Outlasts the Thesis

- Confluent adds roughly $600 million of confirmed 2026 dilution from stock-based compensation and interest expense, with EBITDA accretion expected only in year one post-close, not at the time of closing

- Red Hat grew just 8% in Q4 2025 versus a mid-teens longer-run target, held back by U.S. federal government shutdown disruption and weaker ACV bookings; a second consecutive quarter below expectations would compress the software segment multiple

- IBM Consulting grew only 1% in Q4 2025 and faces structural pricing pressure from AI coding tools affecting the labor-intensive middle-market engagements that represent the core of the services revenue mix

- The $17 million DOJ settlement over DEI practices, while financially immaterial, adds regulatory headline risk during a period when government contract concentration makes political exposure relevant to the revenue model

Should You Invest in International Business Machines Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up IBM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track International Business Machines Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze IBM stock on TIKR for Free →