Key Stats for Home Depot Stock

- 52-Week Range: $315 to $427

- Current Price: $341

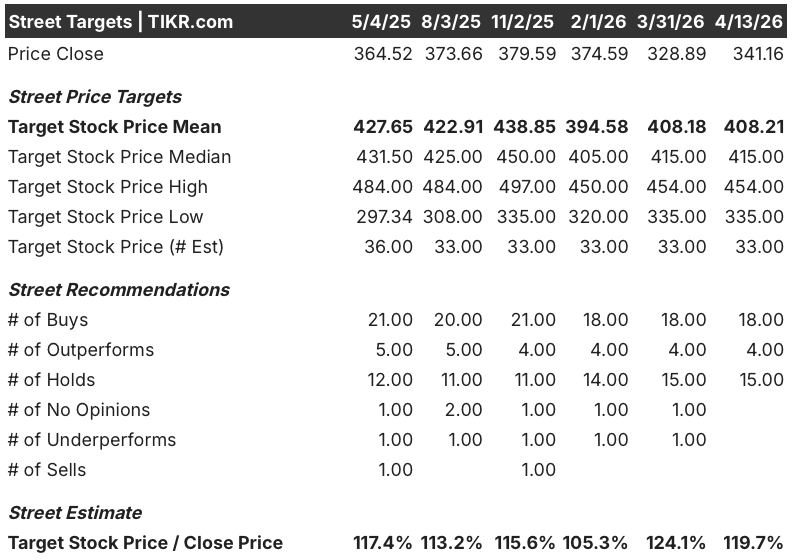

- Street Mean Target: $408

- Street High Target: $454

- TIKR Model Target (Jan. 2031): $537

What Happened?

Home Depot (HD), the world’s largest home improvement retailer with 2,359 stores and over $164 billion in annual revenue, is being priced by the market as if its customers are financially stressed — when the actual data says something entirely different.

The company posted Q4 fiscal 2025 adjusted EPS of $2.72, beating the $2.54 analyst consensus, as professional contractor demand held firm and January storm activity provided a late-quarter sales lift.

Full-year fiscal 2025 revenue reached $164.68 billion, up 3% year over year, with the SRS Distribution platform (a specialty trade distributor covering roofing, pool, and landscaping) growing organic sales by a low single-digit percentage despite the worst annual roofing shipment volumes in the industry since 2019.

In March, SRS agreed to acquire Mingledorff’s, a wholesale HVAC (heating, ventilation, and air conditioning) distributor with 42 locations across five southeastern states, adding a fifth product vertical to the platform and expanding Home Depot’s total addressable market from $1.1 trillion to $1.2 trillion.

Home Depot also named Dr. Franziska Bell as EVP and Chief Technology Officer effective April 6, bringing a former Ford Motor chief data, AI, and analytics officer in to lead enterprise-wide deployment of agentic AI across associate tools, customer-facing platforms, and the Pro ecosystem.

CEO Ted Decker stated on the Q4 2025 earnings call that “we’ve been looking for Two Sigma, on-time and complete for our delivery to our Pros, and we achieved that this past year,” anchoring delivery reliability as a structural competitive advantage rather than a short-term operational target.

CFO Richard McPhail told investors at the J.P. Morgan Retail Round Up Forum on April 9 that when he surveys customers and asks Pros what their clients are saying, the answer is consistent: “It’s not that I don’t have the ability to spend. It’s that it just doesn’t feel like the right time” — a distinction that separates a psychology-driven freeze from a fundamentally impaired consumer.

Wall Street’s Take on Home Depot Stock

The market is mispricing Home Depot stock by conflating a housing activity freeze with a consumer health problem: homeowners have seen housing wealth increases of 80% to 90% over six years, are at full employment, and have growing incomes — they are simply waiting for the moment when spending feels right.

HD’s normalized EPS is expected to grow from $14.69 in fiscal 2026 to around $15 in fiscal 2027 and roughly $16 in fiscal 2028, a roughly 8% acceleration that will be driven by mid-single-digit organic SRS growth, the full-year GMS contribution, and operating expense leverage as the acquisition base matures — all of which are independent of any housing recovery.

Covering analysts give Home Depot stock 22 buys or outperforms against 15 holds and a lone underperform, with a mean price target of $408 and a median of $415, implying roughly 20% upside from the current price of $341, with Wall Street specifically waiting for any signal that the housing turnover rate — stuck at 3% of homes changing hands for nearly four years — breaks toward its historical 4% to 5% norm.

The target spread runs from around $335 on the low end to $454 on the high end, with the low end assuming housing turnover stays frozen through at least 2027 and the high end pricing in a meaningful affordability improvement as mortgage rates drift below 6% and unlock the kitchen, flooring, and lighting categories that are currently under the most pressure.

Trading at roughly 22.6x forward fiscal 2027 EPS against a 5-year historical average closer to 23-25x at comparable or softer growth rates, with normalized EPS set to accelerate from roughly 2.5% growth in fiscal 2027 to roughly 8% in fiscal 2028 as acquisition drag fades, Home Depot stock appears undervalued for investors who believe the psychological freeze resolves before the multiple contracts further.

McPhail’s April 9 framing that the homeowner “financial position is solid and frankly, better than it’s ever been pre-COVID” directly contradicts the stressed-consumer narrative embedded in the current share price, and represents the clearest reframe available: when sentiment turns, the spending capacity is already in place.

A prolonged mortgage rate environment above 6% combined with broad-based home price corrections in Sun Belt markets that begin to impair homeowner balance sheets rather than merely slow turnover would break this thesis by converting a psychology problem into a real one.

Home Depot’s Q1 fiscal 2026 earnings, expected in May, will be the first test of whether the mid-single-digit EPS decline McPhail guided for is tracking to the low or high end of that range, with comparable sales performance and SRS organic growth the specific figures to watch for any leading signal.

Home Depot Stock Financials

Home Depot grew total revenue from $159.51 billion in fiscal 2025 to $164.68 billion in fiscal 2026, a 3% increase that reflects the partial-year GMS contribution rather than any improvement in the underlying housing demand environment.

Operating income declined 3% to $20.89 billion as SG&A rose 6.8% to $30.7 billion, primarily reflecting the GMS expense base and higher intangible amortization tied to the SRS and GMS acquisitions, compressing operating margins from 13.5% to 12.7%.

The gross margin compression tells a more precise story: gross profit margins declined from 33.6% in fiscal 2022 to 33% in fiscal 2026, a 30-basis-point contraction driven entirely by the mix-dilutive effect of lower-margin wholesale distribution revenue from SRS and GMS, with McPhail confirming at the April 9 forum that excluding GMS, the core retail gross margin landed exactly on management’s expectation for the year.

Management guided to approximately 33.1% gross margin for fiscal 2027, with GMS annualization headwinds concentrated in the first half and normalizing in the second, making Q1 fiscal 2027 the likely trough for margin pressure before the income statement begins to reflect the operating leverage McPhail described at the December investor conference.

What Does the Valuation Model Say?

The TIKR mid-case model targets $537 for Home Depot stock by fiscal 2031, implying a 57% total return from current levels on roughly 6% EPS CAGR assumptions and a net income margin recovery toward 9.5%, both of which sit below McPhail’s own market-recovery framework of 5% to 6% top-line growth with bottom-line growing faster — meaning the base case is built on conservative inputs relative to what management has told investors to expect.

With the stock at a roughly 22.6x forward multiple against a 23-25x historical range, EPS accelerating from low-single-digit to high-single-digit growth as acquisition drag fades over the next two years, and the TIKR base case implying 57% upside before any housing recovery premium, Home Depot stock is undervalued by a margin that widens materially if housing turnover normalizes on any timeline before 2028.

The Home Depot investment case hinges on one variable: does the psychology-driven housing freeze resolve in 12 to 18 months, or does it extend long enough to push the earnings recovery timeline past what consensus is currently pricing in?

Bull Case: The Sentiment Unlock

- McPhail confirmed at the April 9 J.P. Morgan forum that homeowners have seen housing wealth gains of 80% to 90% over six years, are at full employment, and have growing incomes — the spending capacity exists; only the willingness is frozen

- Mortgage rates trended toward 6% in early 2026, and any further move toward 5.5% represents the largest single affordability improvement since 2022, directly unlocking turnover and the high-margin kitchen, flooring, and lighting categories currently under the most pressure

- SRS organic sales are guided to grow mid-single digits in fiscal 2027 independent of housing recovery, and Mingledorff’s HVAC distribution adds a $100 billion TAM expansion that gives SRS a fifth cross-sell vertical before the roofing market even normalizes

- The TIKR high case targets $853 by 2031, implying roughly 150% total return on roughly 7% EPS CAGR and 9.9% net income margins, achievable if the market recovery materializes in late 2026 or early 2027

Bear Case: The Freeze Extends

- McPhail explicitly stated that the company has “not yet seen a catalyst for an inflection in housing activity” and guided Q1 fiscal 2027 to mid-single-digit EPS declines before the year improves, meaning near-term earnings momentum is negative before it turns positive

- Comparable sales guidance of flat to 2% for fiscal 2027 assumes the broader industry is negative 1% to positive 1%, leaving Home Depot entirely dependent on share gains rather than market tailwinds for any upside to that range

- SRS roofing industry shipments were down 28% year over year in Q4, and the pricing pressure McPhail said would bleed into Q1 fiscal 2027 could weigh on SRS margins before the HVAC and GMS verticals generate meaningful cross-sell contribution

- The TIKR low case targets $578 by 2031, implying around 69% total return but only roughly 6% annualized, a return that barely compensates for multi-year housing stall risk in the current macro environment

Should You Invest in The Home Depot, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HD stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Home Depot, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HD stock on TIKR for Free →