Key Takeaways:

- Supply Chain Complexity: Trade uncertainty and AI adoption are driving 19% adjusted EBITDA growth for the logistics network leader.

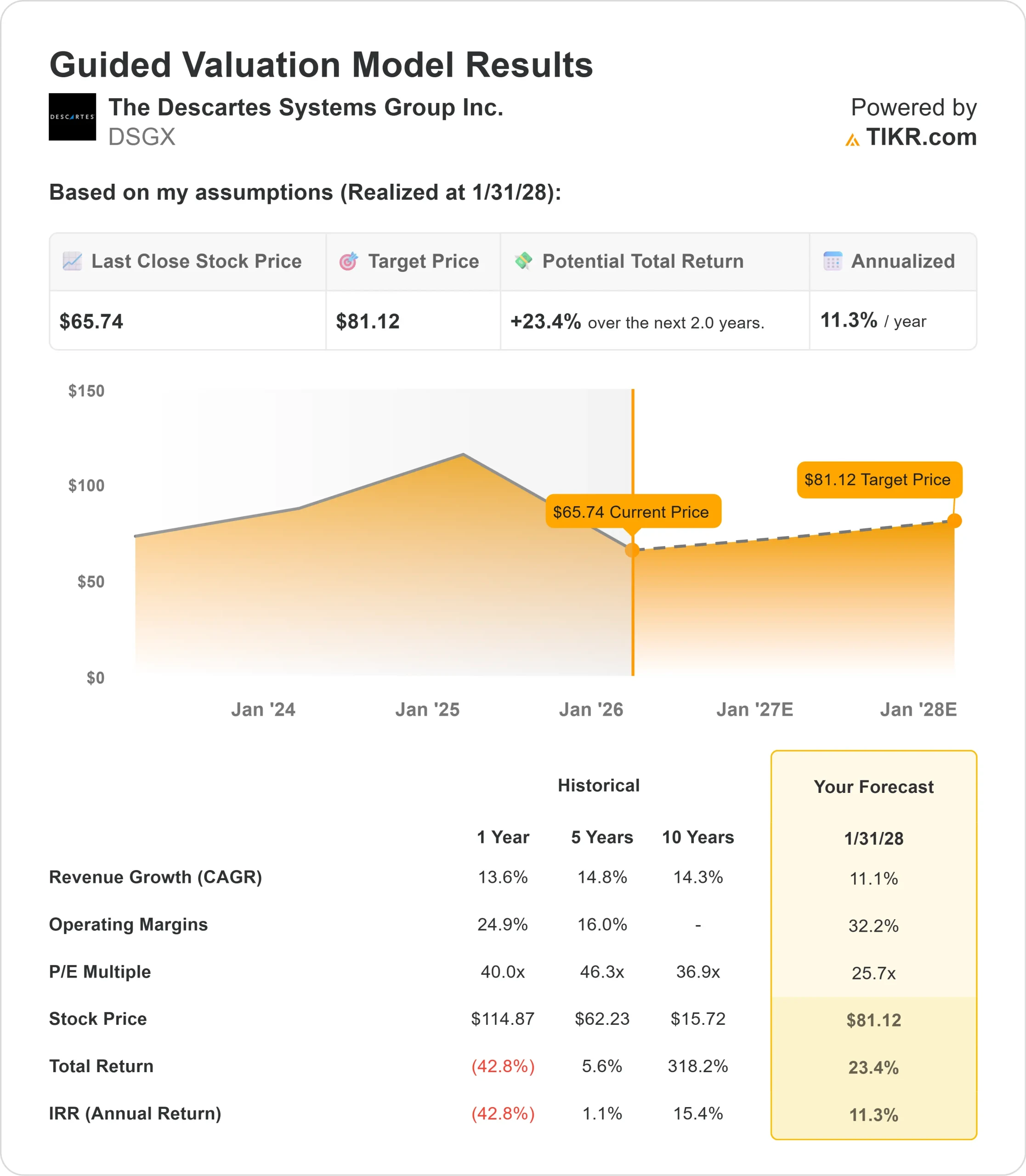

- Price Projection: Based on current execution, DSGX stock could reach $81 by January 2028.

- Potential Gains: This target implies a total return of 23% from the current price of $66.

- Annual Return: Investors could see roughly 11% growth over the next 2 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Descartes Systems Group (DSGX) delivered exceptional third-quarter results in fiscal 2026 with record revenues and profits across the board. The company posted total revenues of $188 million, up 11% year-over-year, while adjusted EBITDA surged 19% to $86 million.

CEO Ed Ryan emphasized how global trade chaos is creating strong demand for Descartes’ solutions.

- Over the past 90 days alone, customers navigated a tariff truce between China and the U.S., expansions on metals and furniture tariffs, new reciprocal trade agreements, and constantly shifting denied-party screening requirements.

- This uncertainty drives customers to Descartes for tariff data, sanctioned-party screening, and trade-flow research.

- The company’s foreign trade zone solutions saw particularly strong uptake as importers sought ways to defer tariffs and manage cash flow more effectively.

- The company’s MacroPoint business achieved a market-leading 90% truck-tracking rate by using AI agents to engage drivers.

- This represents a dramatic improvement from 87% just months earlier, accomplished by automating outreach to more than 300,000 truckers and adding 180,000 new drivers to the network.

- E-commerce customs clearance became another major growth driver after the U.S. eliminated the de minimis exemption.

- Foreign sellers suddenly needed to file customs declarations and pay tariffs on shipments that had previously been exempt. Descartes’ high-velocity processing capabilities captured significant market share as competitors struggled to handle millions of daily transactions.

Despite strong fundamentals and a recession-resistant business model, Descartes trades at $66, offering upside for investors who recognize the company’s position as critical infrastructure for global trade.

See analysts’ full growth forecasts and estimates for DSGX stock (It’s free) >>>

What the Model Says for Descartes Systems Stock

We analyzed Descartes as it transformed into the world’s dominant logistics network operator, serving 26,000 customers globally.

The company benefits from structural tailwinds that compound over time. Trade complexity continues to increase regardless of economic conditions, requiring more sophisticated compliance and data solutions.

AI adoption accelerates demand for clean, formatted, real-time data flowing across Descartes’ Global Logistics Network.

Management’s recent AI hackathon generated more than 50 employee suggestions for new services, many of which have already been deployed.

Examples include natural-language searches of import data, automated denied-party screening logic, free-trade eligibility assessments, and AI-powered tariff classification recommendations.

The network model creates powerful defensibility. Competitors cannot replicate functionality without connecting to the same trading partners and accumulating comparable datasets—a process that takes years and incurs substantial losses before reaching profitability.

This explains why no significant new network competitor has emerged in two decades.

Using a forecast of 11% annual revenue growth and 32% operating margins, our model projects the stock will rise to $81 within 2 years. This assumes a 26x price-to-earnings multiple.

That represents a slight compression relative to Descartes’ historical P/E averages of 40x (one year) and 46x (three years).

The lower multiple reflects near-term uncertainty from transportation volume fluctuations and the market’s tendency to undervalue network businesses during volatile periods.

The real value lies in Descartes’ compounding growth model—organic expansion plus strategic acquisitions—within a mission-critical network that becomes more valuable as it scales.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DSGX stock:

1. Revenue Growth: 11.1%

Descartes delivered 7% organic services growth in Q3, accelerating from 4% in the first half. Services revenue now represents 93% of total revenue and drives profitability.

The company’s growth centers on structural demand rather than cyclical factors.

- Global trade intelligence solutions grew robustly as customers navigated tariff complexity.

- E-commerce customs filing nearly doubled after regulatory changes.

- MacroPoint tracking revenue increased as AI improvements drove higher billable loads.

- Cross-selling continues expanding, now reaching 65-70% of revenue as customers adopt multiple solutions across the network.

Management expects to maintain 10-15% adjusted EBITDA growth annually through a combination of organic expansion and strategic M&A.

2. Operating margins: 32.2%

Descartes operates at a 46% adjusted EBITDA margin after expanding 300 basis points from restructuring actions earlier this year. The company eliminated millions in annual costs while maintaining service quality.

Network businesses naturally expand margins as they scale because infrastructure costs grow more slowly than revenue.

Adding new customers or transactions to existing networks requires minimal incremental investment.

3. Exit P/E Multiple: 25.7x

The market currently values Descartes at 26x earnings. We assume modest compression to 26x over our forecast period.

Near-term uncertainty from transportation volumes and general market volatility weighs on the multiple.

However, Descartes’ network model, cash generation, and AI positioning should command premium valuations as execution continues.

The company ended Q3 with $279 million in cash, zero debt, and a $350 million undrawn credit facility—providing ample firepower for acquisitions and opportunistic share buybacks through its newly authorized normal course issuer bid.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Logistics networks face volume cycles and regulatory changes. Here’s how Descartes stock might perform under different scenarios through January 2030:

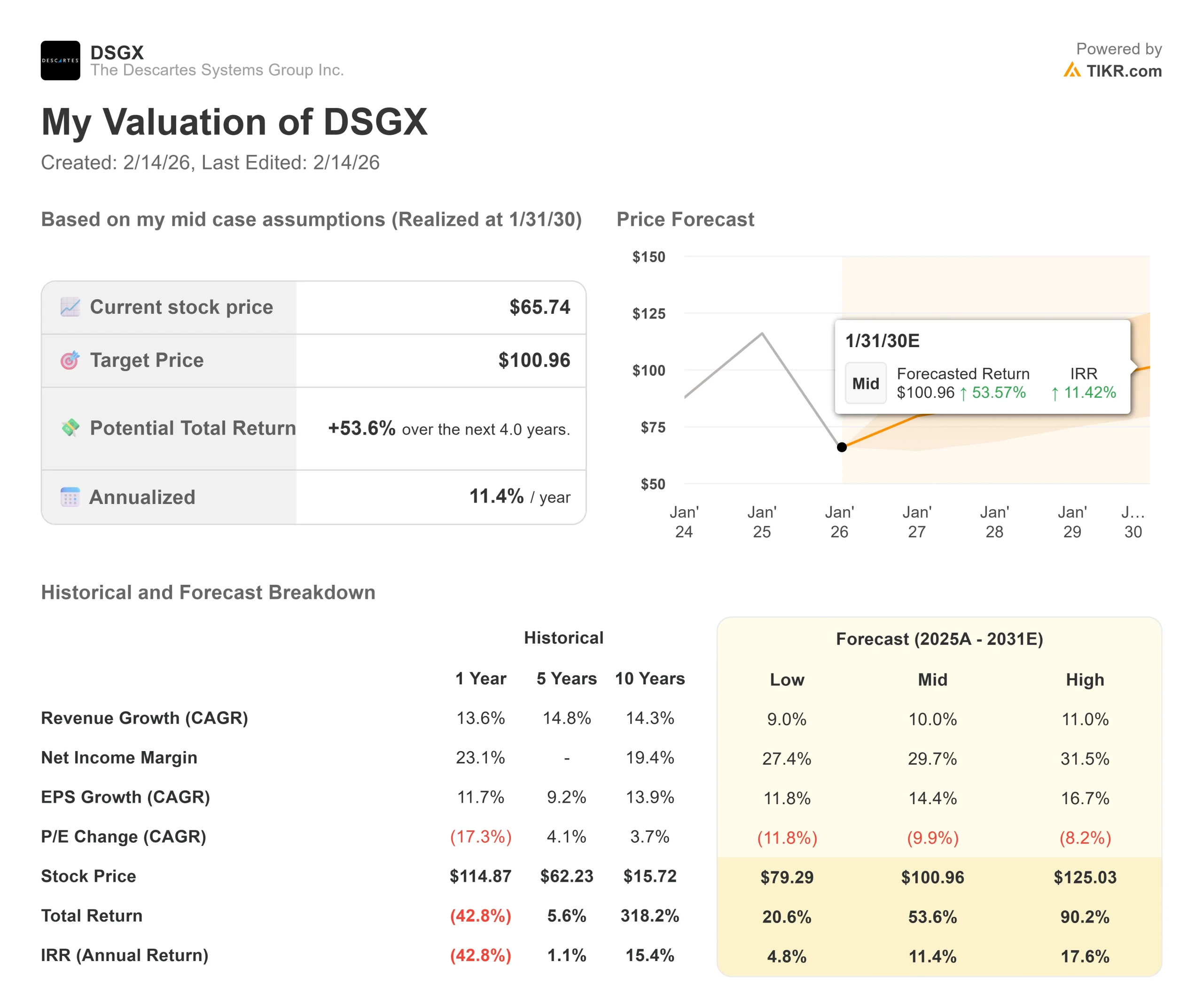

- Low Case: If revenue growth slows to 9% and net income margins compress to 27%, investors still see a 21% total return (5% annually).

- Mid Case: With 10% growth and 30% margins, we expect a total return of 54% (11% annually).

- High Case: If AI-driven demand acceleration drives 11% revenue growth while Descartes maintains 32% margins, returns could hit 90% total (18% annually).

See what analysts think about DSGX stock right now (Free with TIKR) >>>

The range reflects execution on AI monetization, success in capturing market share during industry consolidation, and the company’s ability to maintain pricing power as it becomes more embedded in customers’ operations.

In the worst case, transportation volumes decline significantly, and competitive pressures emerge.

In the best case, AI drives faster-than-expected network demand, cross-selling accelerates beyond historical rates, and acquired companies integrate ahead of schedule.

How Much Upside Does Descartes Systems Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!