Key Stats for Elevance Health Stock

- Past-6-Month Performance: 18%

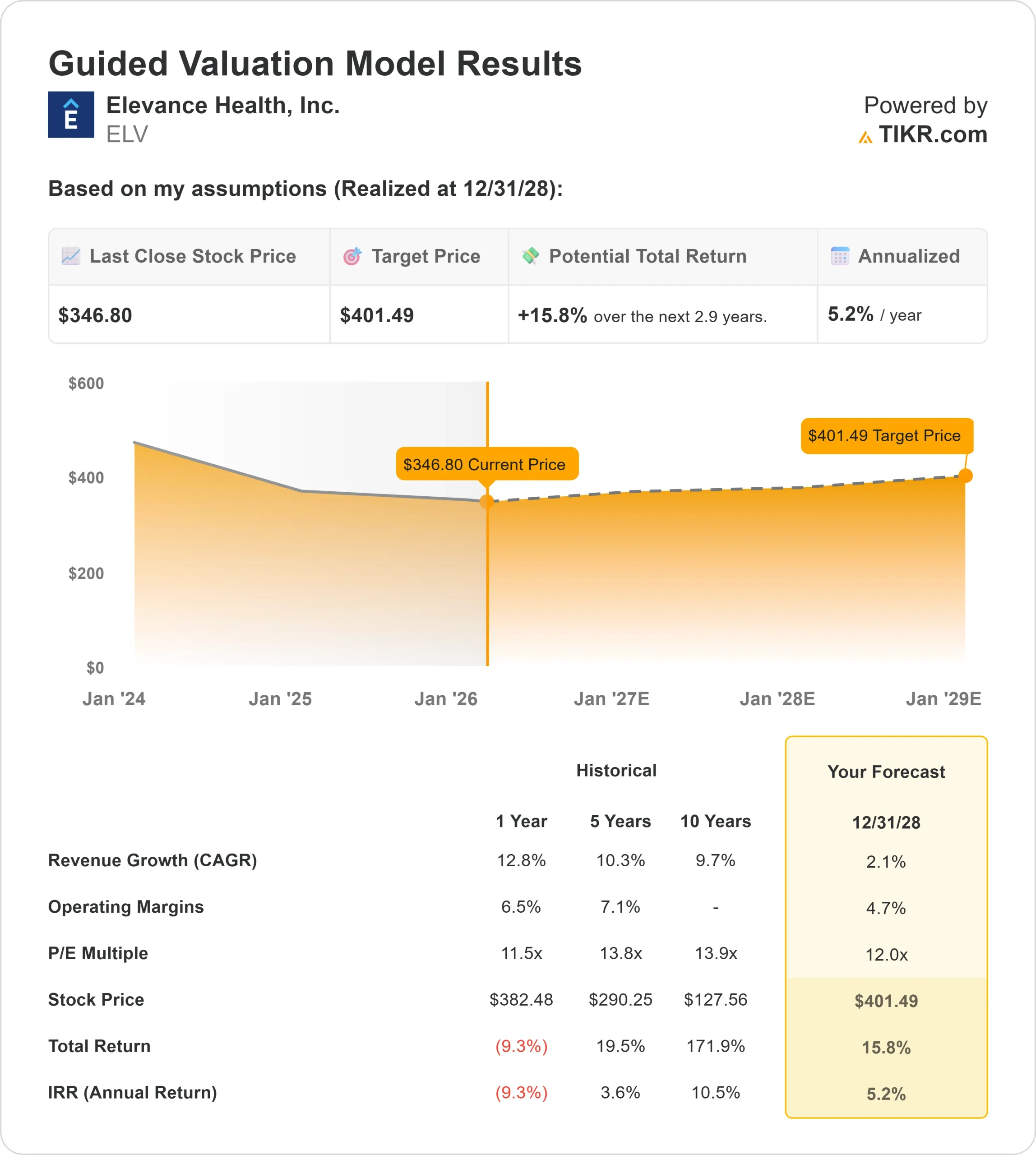

- 52-Week Range: $274 to $459

- Valuation Model Target Price: $401

- Implied Upside: 16%

Value your favorite stocks like Elevance Health with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Elevance Health stock is up about 18% over the last 6 months, recently trading near $347 per share, as investors responded to improving earnings visibility and disciplined portfolio repositioning across its Medicare and Commercial businesses.

Shares rebounded from prior weakness as cost trend stabilization and pricing discipline helped restore confidence in the company’s earnings outlook.

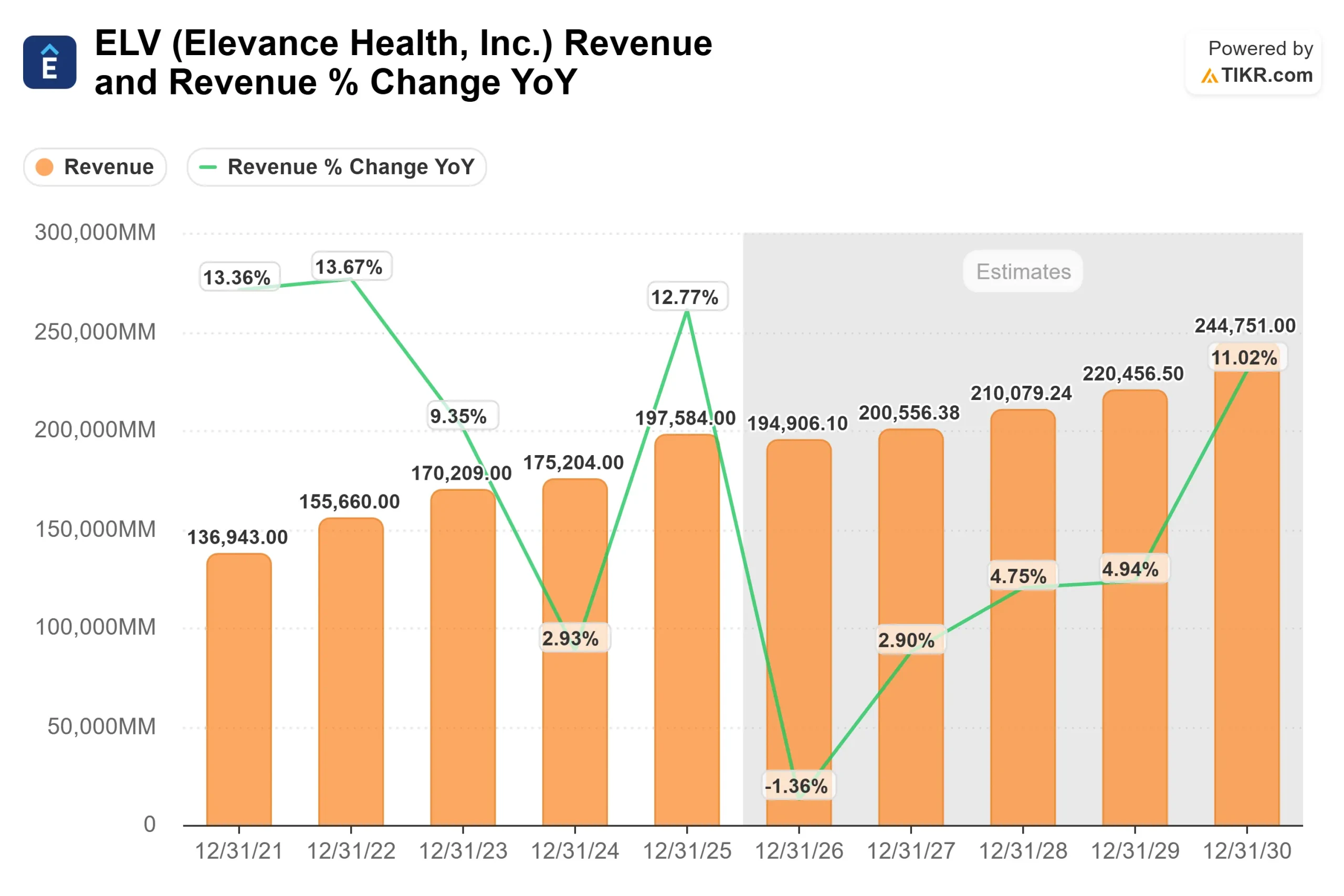

The stock moved higher after management clarified its 2026 strategy despite near-term pressure. Elevance reported Q4 adjusted EPS of $3.33 on $49.3 billion in revenue, up 10% year over year, and guided to adjusted EPS of at least $25.50 in 2026.

While 2026 represents a reset year with Medicaid operating margins of approximately -1.75% and Medicare Advantage membership declining in the high teens percentage range, management expects Medicare Advantage margins to improve to at least 2%.

CEO Gail Boudreaux said, “2026 is a year of execution and repositioning,” while reaffirming a return to at least 12% adjusted EPS growth in 2027.

Institutional positioning has been mixed but constructive. M&G PLC increased its stake by 9.1% to 1,015,113 shares worth approximately $327.9 million, and Public Sector Pension Investment Board boosted its holdings by 515.5% to 106,682 shares valued at $34.47 million.

Although some firms trimmed exposure, institutional investors collectively own roughly 89.24% of the stock, reinforcing long-term conviction in the company’s diversified earnings base.

With shares still below the $459 52-week high, the six-month rally reflects growing confidence that margin compression may prove cyclical rather than structural.

The next catalyst is evidence that medical cost trends moderate and Medicare margin improvement materializes in 2026.

See analysts’ growth forecasts and price targets for Elevance Health (It’s free) >>>

Is Elevance Health Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 2.1%

- Operating Margins: 4.7%

- Exit P/E Multiple: 12x

Revenue growth is projected to dip in 2026 to $194.9 billion before recovering to $200.6 billion in 2027 and $210.1 billion in 2028, reflecting normalization after elevated utilization pressure.

Given Elevance’s scale of more than $200 billion in annual revenue, earnings durability depends more on pricing alignment and cost discipline than aggressive enrollment expansion.

Analyst estimates reflect slower top-line expansion in the near term, but they also incorporate gradual stabilization in risk-based membership and improved premium yields.

As Medicare Advantage bids are repriced and Medicaid rates move closer to actual cost trends, revenue visibility could improve even without meaningful enrollment growth.

The 4.7% operating margin assumption reflects gradual recovery as Medicaid rate adjustments and Medicare Advantage repricing take effect. Even modest improvements in medical loss ratio can materially expand earnings due to scale.

Carelon adds another structural lever, as pharmacy, oncology, behavioral health, and risk-based service programs support margin resilience and external growth beyond core insurance membership.

The 12x exit multiple aligns with historical trading levels and does not assume multiple expansion.

Based on these inputs, the valuation model estimates a target price of $401, implying about 16% total upside over roughly 2.9 years and a 5% annualized return, indicating the stock appears undervalued at current prices.

Results over the next year hinge on execution across several higher-impact areas. Medicare Advantage repricing, stabilization in outpatient utilization, and improved Medicaid rate alignment remain central to restoring margin confidence.

Further expansion in Carelon’s external growth, including specialty pharmacy, oncology management, and behavioral health programs, could support earnings durability even if core membership growth remains muted.

At the same time, capital returns funded by free cash flow, including share repurchases and dividends, continue to enhance per-share earnings growth.

At current levels, Elevance Health appears undervalued, with future performance driven primarily by margin stabilization, disciplined underwriting, Carelon expansion, and capital allocation rather than rapid revenue acceleration.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>