Key Stats for Freeport-McMoRan Stock

- Past-6-Month Performance: 47%

- 52-Week Range: $28 to $70

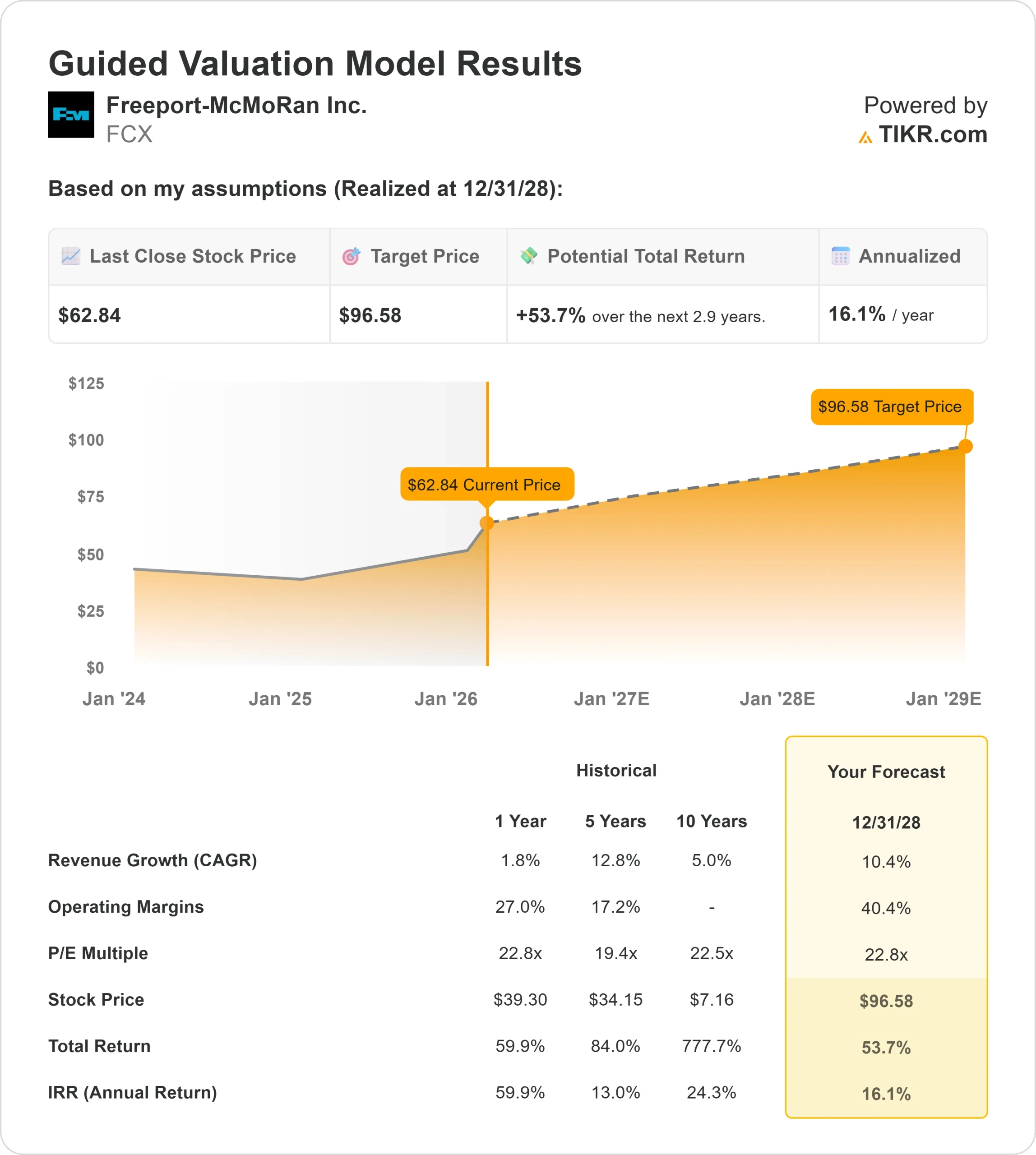

- Valuation Model Target Price: $97

- Implied Upside: 54%

Value your favorite stocks like Freeport-McMoRan with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Freeport-McMoRan stock rose about 47% in the last 6 months, climbing to $62.84 per share as copper prices strengthened and investors positioned for improving production and cash flow into 2026. Shares advanced steadily alongside rising commodity prices and clearer visibility on the company’s operational recovery.

The stock moved higher primarily because copper prices strengthened materially and management delivered financial results that demonstrated strong operating leverage.

In 2025, LME copper averaged $4.51 per pound and recently traded about 30% above that average, directly increasing revenue and cash flow expectations.

Management reported adjusted EBITDA of nearly $10 billion for 2025 and consolidated unit net cash costs of $1.65 per pound, while U.S. operating income in Q4 was 3.5x the prior-year quarter, showing how quickly higher copper prices translate into profit growth.

Analyst activity and institutional flows reinforced the rally. BNP Paribas Exane raised its price target to $75 from $56 and maintained an Outperform rating, signaling stronger conviction in long-term earnings power.

Public Sector Pension Investment Board increased its stake by 635.3% to 801,584 shares valued at $31.44 million, while State of New Jersey Common Pension Fund D boosted its position by 6.4% to 508,117 shares worth $19.93 million.

Institutional ownership now stands near 80.8%, reflecting broad confidence in the copper cycle.

Despite insider selling by Chairman Richard Adkerson, who sold 248,031 shares at $62.80 and 152,960 shares at $64.65, and EVP Douglas Currault II, who sold 75,000 shares at $64.52, the stock continued climbing.

Investors appeared focused on copper fundamentals and the production ramp-up at Grasberg rather than insider portfolio adjustments.

See analysts’ growth forecasts and price targets for Freeport-McMoRan (It’s free) >>>

Is Freeport-McMoRan Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 10.4%

- Operating Margins: 40.4%

- Exit P/E Multiple: 22.8x

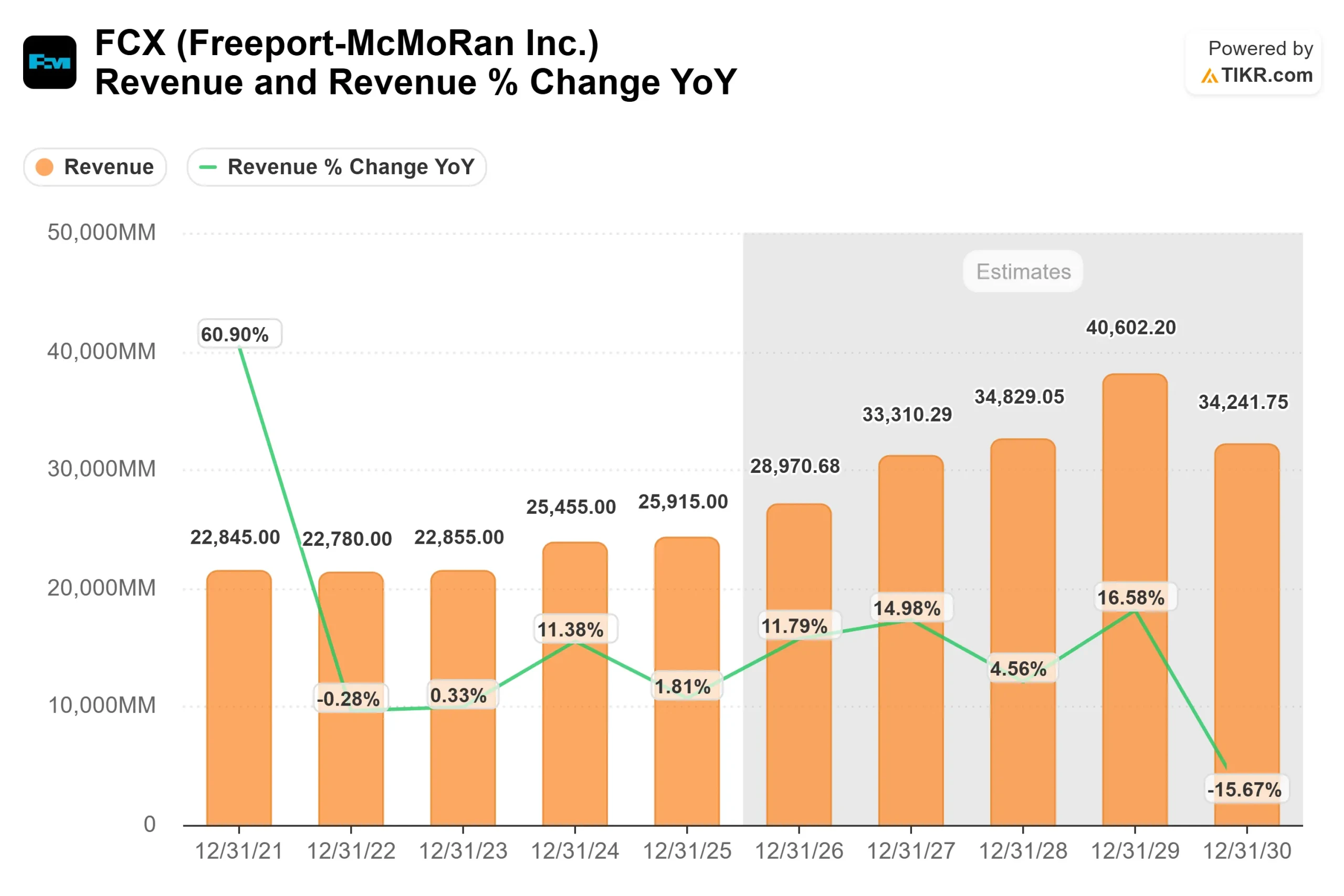

Revenue growth is supported by the phased restart at Grasberg, where management expects 85% of district production restored in the second half of 2026, alongside scaling U.S. leach production to 300 million pounds in 2026.

Company projections show revenue rising from $25,915 million in 2025 to $33,310 million in 2027, reflecting higher copper volumes and tight global supply conditions.

Copper market fundamentals remain constructive. Electrification, AI data centers, renewable energy, and grid modernization continue driving structural demand growth, while new mine supply remains constrained.

With earnings highly sensitive to copper pricing, sustained price strength can materially expand cash flow.

Margin expansion remains central to the story. Trailing twelve-month gross margins are 37.1% and EBIT margins are 25.1%, meaning incremental copper price gains flow disproportionately to operating income.

The company’s Q4 results demonstrated that leverage clearly, with U.S. operating income rising 3.5x year over year.

Freeport maintains financial flexibility. Net debt stands at $6,668 million with net debt to EBITDA of 0.72x, providing capacity to fund growth initiatives such as Bagdad expansion and continued leach innovation while maintaining shareholder returns.

Based on these inputs, the valuation model estimates a target price of $97, implying 54% total upside over roughly 2.9 years and a 16% annualized return.

With shares at $62.84, Freeport-McMoRan appears undervalued, with performance into 2026 likely driven by copper price strength, production ramp-up execution, and sustained operating leverage.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>