Key Takeaways:

- AI Integration: Procore’s AI agents are saving customers thousands of labor hours, positioning the company to lead construction’s digital transformation.

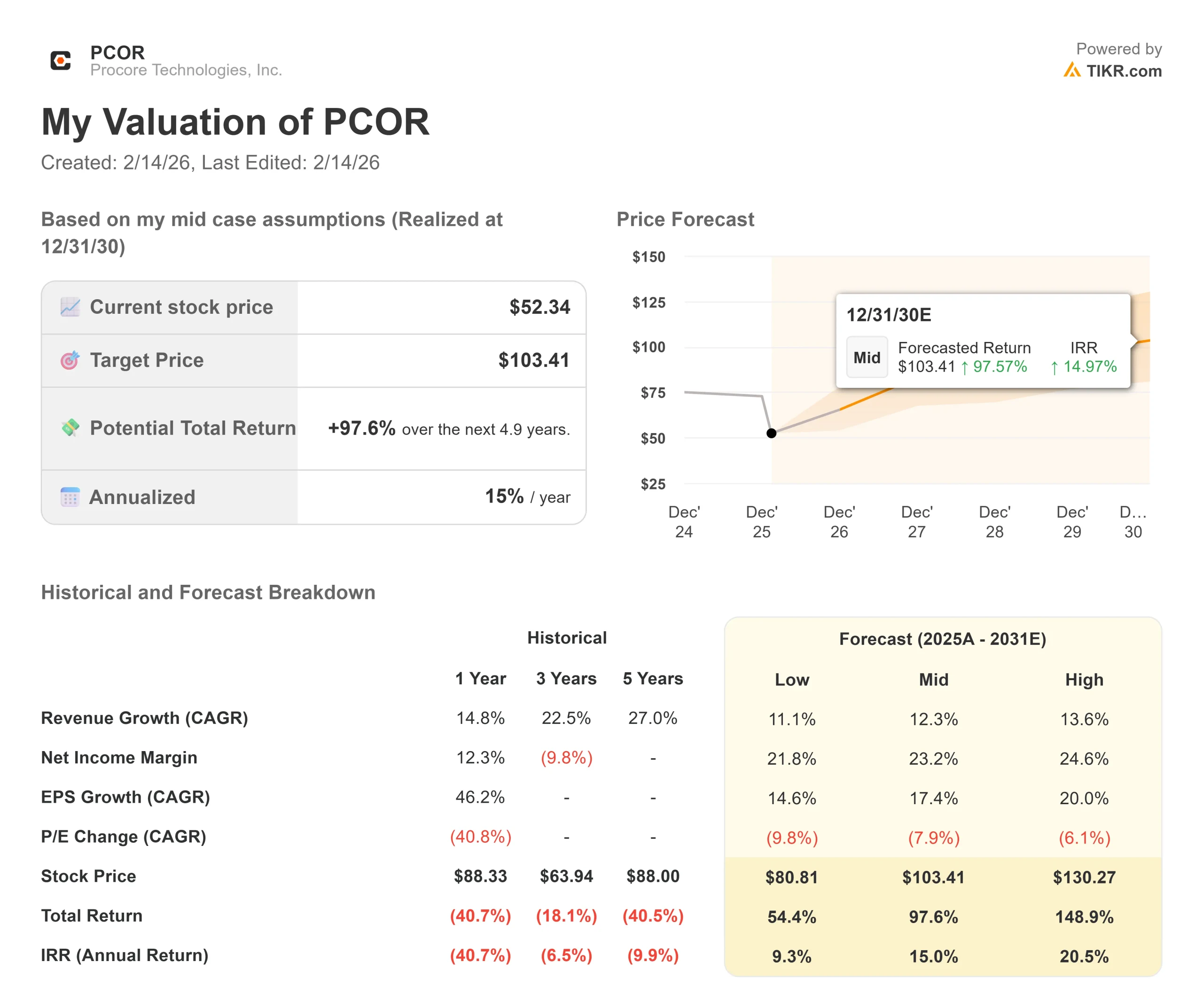

- Price Projection: Based on current execution, PCOR stock could reach $78 by December 2028.

- Potential Gains: This target implies a total return of 49% from the current price of $52.

- Annual Return: Investors could see roughly 15% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Procore Technologies (PCOR) delivered exceptional fourth-quarter results in fiscal 2025, with CEO Ajei Gopal reporting revenue growth of 15% and non-GAAP operating margin expansion of 400 basis points year-over-year.

- Revenue reached $349 million in Q4, exceeding guidance, while the company added three new ENR 400 logos and expanded relationships with over 70 existing ENR 400 customers.

- Management highlighted robust demand across general contractors, owners, and the emerging data center construction market.

- The construction industry faces a chronic labor shortage of nearly 350,000 workers in the U.S. alone. Procore’s AI agents are addressing this challenge head-on by automating tasks that historically consumed hours of manual effort.

- In one example, a superintendent used Procore AI to identify a structural column issue through video analysis. The AI agent automatically pulled relevant drawings, created work orders, and scheduled rework—tasks that would have required several hours manually.

- Customer Haskell reported immediate ROI from deploying Procore AI on a single project, saving superintendents hours per day. Within six months, they expanded to multiple projects and planned a portfolio-wide deployment.

- The company’s DataGrid acquisition accelerates this AI strategy by adding advanced reasoning capabilities and broader third-party integrations.

- Procore’s competitive advantages extend beyond technology. With nearly 3 million active users and a vast proprietary dataset capturing dynamic project changes, the company has built a digital window into the built world.

- This network effect creates switching costs—customers who leave for cheaper alternatives often return, as demonstrated by a Georgia contractor who came back and expanded to a high six-figure deal after departing in 2024.

The data center construction market presents additional upside. While currently representing just 2% of total U.S. construction activity, AI infrastructure investment is driving unprecedented growth.

Procore’s largest international Q4 deal was a seven-figure annual contract with a U.K. hyperscaler building data centers globally.

Management achieved FedRAMP moderate authorization during the quarter, unlocking opportunities with federal and state government customers.

The company also sees substantial white space with owners—diverse customers spanning technology, energy, utilities, education, healthcare, and real estate—who represent a significant growth lever alongside subcontractors.

The company now trades at $52 after falling 30% over the past year, creating a potential opportunity for investors who recognize Procore’s position as the mission-critical platform for construction.

See analysts’ full growth forecasts and estimates for PCOR stock (It’s free) >>>

What the Model Says for Procore Stock

We analyzed Procore’s transformation into construction’s definitive vertical software platform and its emerging AI leadership position.

The company benefits from structural tailwinds as the construction industry digitizes operations.

Despite macroeconomic headwinds—with the U.S. Census reporting negative growth for the combined nonresidential and multifamily sectors—Procore continues to gain market share, with over $1 trillion in active construction volume commitments on its platform.

Management expects fiscal 2026 revenue between $1.489 billion and $1.494 billion, representing 13% growth, with non-GAAP operating margins expanding to 17.5-18%.

Free cash flow margins are projected at 19%, up 270 basis points year-over-year.

Using a forecast of 13.3% annual revenue growth and 20.6% operating margins, our model projects the stock will rise to $78 within 2.9 years. This assumes a 27.2x price-to-earnings multiple.

That represents compression from Procore’s historical P/E average of 48.7x over the past year. The lower multiple acknowledges near-term uncertainty from challenging construction market conditions and the company’s evolution toward profitability-focused growth.

The real value lies in capturing long-term trends in construction digitization while monetizing AI capabilities that deliver measurable ROI for customers.

Procore’s volume-based pricing model provides structural protection—revenue scales with project size rather than seat count, insulating the business as AI improves productivity.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PCOR stock:

1. Revenue Growth: 13.3%

Procore’s growth centers on market share gains in a massive addressable market.

The company delivered 15% revenue growth in fiscal 2025 despite headwinds in the construction industry.

Strong momentum with ENR 400 customers, expanding owner relationships, and emerging data center opportunities support continued growth.

Management’s fiscal 2026 guidance of 13% growth reflects a prudent outlook given macro uncertainty, while AI monetization represents incremental upside not yet reflected in projections.

2. Operating margins: 20.6%

Procore expanded adjusted operating margins by 400 basis points in fiscal 2025 through operational efficiency and disciplined expense control.

Management guides to 17.5-18% operating margins for fiscal 2026, representing another 340-390 basis points of expansion.

The company has largely completed go-to-market investments and now focuses on productivity improvements.

Continued leverage across all operating expense lines, combined with AI-driven internal efficiencies, supports our assumption of 20.6% margins through 2029.

3. Exit P/E Multiple: 27.2x

The market currently values Procore at 29x earnings. We assume modest compression to 27.2x over our forecast period.

Near-term softness in the construction market and the transition to profitability-focused growth weigh on the multiple.

However, as Procore demonstrates AI monetization success and the construction cycle eventually recovers, the company should command a premium multiple relative to software peers given its vertical market leadership, network effects, and structural growth opportunities.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Construction software companies face technology adoption cycles and economic sensitivity. Here’s how Procore stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth moderates to 11.1% and net income margins reach 21.8%, investors could see a 54% total return (9.3% annually).

- Mid Case: With 12.3% growth and 23.2% margins, we expect a total return of 98% (15.0% annually).

- High Case: If AI monetization accelerates, driving 13.6% revenue growth while Procore achieves 24.6% margins, returns could hit 149% total (20.5% annually).

See what analysts think about PCOR stock right now (Free with TIKR) >>>

The range reflects execution on AI monetization, construction market recovery timing, and continued market share gains.

In the low case, construction headwinds persist longer than expected or competitive pressures intensify.

In the high case, AI adoption exceeds expectations, data center construction accelerates faster than anticipated, and margin expansion outpaces guidance as the company achieves greater scale efficiencies.

How Much Upside Does Procore Technologies Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!