Key Takeaways:

- Turnaround Progress: CEO Elliott Hill’s restructuring is gaining traction, with North America growing 9% in Q2 2026.

- Price Projection: Based on current execution, NKE stock could reach $83 by May 2028.

- Potential Gains: This target implies a total return of 33% from the current price of $62.35.

- Annual Return: Investors could see roughly 13% growth over the next 2.3 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Nike (NKE) delivered mixed second-quarter fiscal 2026 results as CEO Elliott Hill’s turnaround enters what he calls the “middle innings.” The company posted modest 1% revenue growth while navigating a deliberate reset of its Classics franchises and marketplace positioning.

- Hill highlighted that the Win Now actions are taking hold, with the sport offense—Nike’s new organizational structure focused on athlete-centered innovation—beginning to bear fruit.

- North America led the way with 9% growth, and wholesale up 24%, validating the strategy of rebuilding partner relationships and diversifying the product portfolio.

- Running continued to gain momentum, with over 20% growth for the second consecutive quarter and market share gains across all channels.

- The Structure 26 stability shoe had strong sell-through, and Nike is preparing to launch Structure Plus in January alongside Nike Mind, a new training platform.

- Despite progress, significant challenges remain. Greater China declined 16% as the company works to break a cycle of promotions and aged inventory.

- CFO Matt Friend acknowledged taking unplanned inventory write-offs in China this quarter. The region won’t see improvement until Nike elevates its store fleet, rebuilds local teams, and shifts from competing on price to showcasing innovation.

- Margins remain under pressure from two forces: intentional marketplace cleanup and $1.5 billion in annualized tariff costs, representing a 320-basis-point gross headwind.

- However, North America showed that the strategy works—gross margins declined by just 330 basis points despite a 520-basis-point tariff impact, indicating the underlying business is healing.

Hill announced organizational changes, with all geographies now reporting directly to him and a new COO focused on operational efficiency.

The company sees a clear path back to double-digit EBIT margins through growth, improved full-price mix, supply chain leverage, and disciplined cost management.

See analysts’ full growth forecasts and estimates for NKE stock (It’s free) >>>

What the Model Says for Nike Stock

We analyzed Nike’s transformation from a Classics-heavy portfolio to a diversified, sport-led strategy across three brands: Nike, Jordan, and Converse.

The company is rightsizing Classics franchises, which declined over $4 billion from peak levels and are down roughly 20% year-over-year.

This reset creates room for performance categories like Running, Football, Basketball, and Training to capture a larger portfolio share.

North America demonstrates the playbook works. The geography cleaned up inventory, reconnected with wholesale partners, reduced promotional activity on Nike.com, and refocused on sport-specific innovation.

Management expects to sustain this momentum as similar actions roll out across EMEA and APLA.

International markets present both near-term headwinds and long-term opportunities. Greater China requires fresh capabilities and patience, but Hill’s direct oversight and diagnosis of structural issues—mono-brand distribution, insufficient retail investment, price-driven competition—provide a credible reset framework.

- Football offers immediate upside, with bookings nearly 40% higher than at the World Cup 2022.

- The Aero-FIT apparel platform launching in March represents genuine innovation that can scale across sports.

- Partnerships like SKIMS are expanding internationally after their success in North America.

Using a forecast of 3.2% annual revenue growth and 8.6% operating margins, our model projects the stock will rise to $83 within 2.3 years. This assumes a 31.6x price-to-earnings multiple.

That represents modest compression from Nike’s historical averages of 32.9x (five years) and 31x (ten years). The valuation acknowledges execution risk across China, Converse, and margin recovery while recognizing structural advantages in sport marketing, innovation pipelines, and distribution reach.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for NKE stock:

1. Revenue Growth: 3.2%

Nike’s growth centers on portfolio diversification away from Classics toward performance.

Running delivered over 20% growth, with market-share gains. Football bookings are up 40% ahead of the World Cup.

Basketball is being “dimensionalized” through women’s (Sabrina, Caitlin Clark) alongside established franchises.

The spring and summer order books are improving season over season, signaling wholesale confidence.

However, growth must overcome ongoing Classics resets and headwinds from China. Management expects modest growth in North America in Q3, with reduced liquidation activity compared with prior quarters.

2. Operating margins: 8.6%

Nike’s EBIT margins compressed to 8% over the latest 12 months due to market cleanup, inventory obsolescence, and tariff headwinds.

However, the path forward is clear: top-line growth, improved full-price mix as promotional activity normalizes, supply chain leverage from wholesale expansion, and tighter operating overhead management.

North America’s margin performance—declining by just 330 basis points despite a 520-basis-point tariff impact—proves that the Win Now actions are working.

As other geographies follow the North America playbook, margin expansion should accelerate.

3. Exit P/E Multiple: 31.6x

The market values Nike at 32.9x earnings. We assume the P/E remains relatively stable at 31.6x over our forecast period.

Near-term uncertainty around China execution and Converse repositioning limits multiple expansion.

However, Nike’s unmatched sport marketing platform, innovation capabilities across footwear and apparel, and integrated direct-to-consumer and wholesale distribution justify a premium valuation.

As the turnaround progresses and management demonstrates sustainable profitable growth, the multiple should hold or expand modestly.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

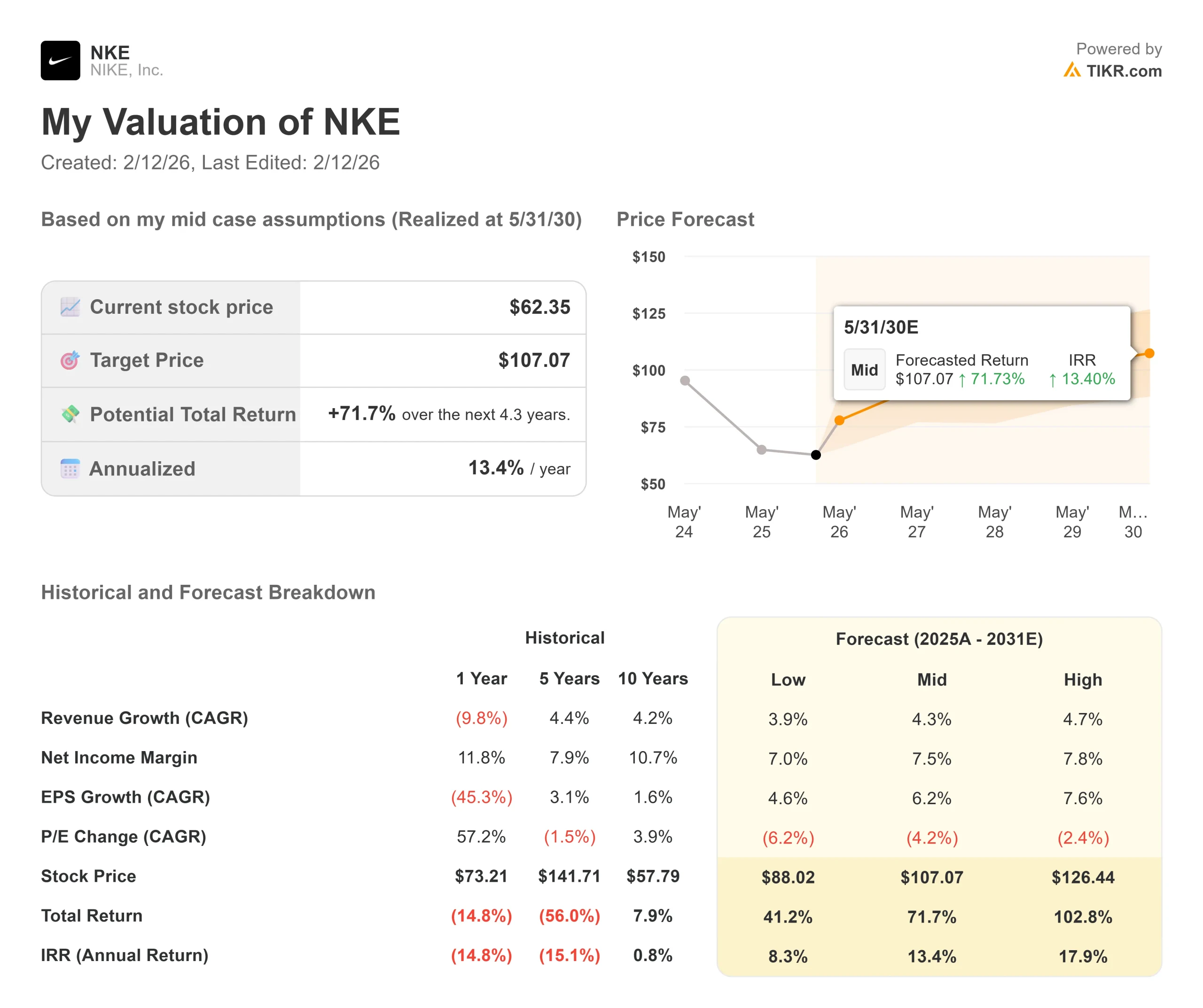

Turnarounds face execution challenges and market dynamics. Here’s how Nike stock might perform under different scenarios through May 2030:

- Low Case: If revenue growth moderates to 3.9% and net income margins compress to 7%, investors still see a 41% total return (8% annually).

- Mid Case: With 4.3% growth and 7.5% margins, we expect a total return of 72% (13% annually).

- High Case: If innovation accelerates, driving 4.7% revenue growth while Nike achieves 7.8% margins, returns could hit 103% total (18% annually).

See what analysts think about NKE stock right now (Free with TIKR) >>>

The range reflects execution of the sport offense, a successful China reset, margin recovery from tariff mitigation, operational efficiency, and the ability to sustain North America momentum while accelerating other geographies.

In the low case, China deteriorates further, wholesale partnerships weaken, or innovation fails to resonate.

In the high case, the Win Now playbook scales faster than expected, the Football World Cup 2026 drives outsized growth, and margin improvement exceeds guidance as operational efficiency gains compound.

How Much Upside Does Nike Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!