Key Takeaways:

- Infrastructure Tailwinds: Vulcan Materials benefits from federal and state infrastructure spending momentum, and B. Riley set a $345 price target citing margin expansion and M&A capacity as growth drivers.

- Earnings Momentum: Vulcan Materials delivered $2 billion in Q3 revenue, up 14% year over year, while EPS rose 80% to $3, marking 11 consecutive quarters of double-digit profitability improvement.

- Price Projection: Based on 6.3% revenue growth, 23% operating margins, and a 30x exit multiple, Vulcan Materials stock could reach $348 by December 2027.

- Modeled Upside: This implies 9% total upside from the current $320 price and a 5% annualized return over 2 years, reflecting limited valuation expansion.

Breaking Down the Case for Vulcan Materials Co.

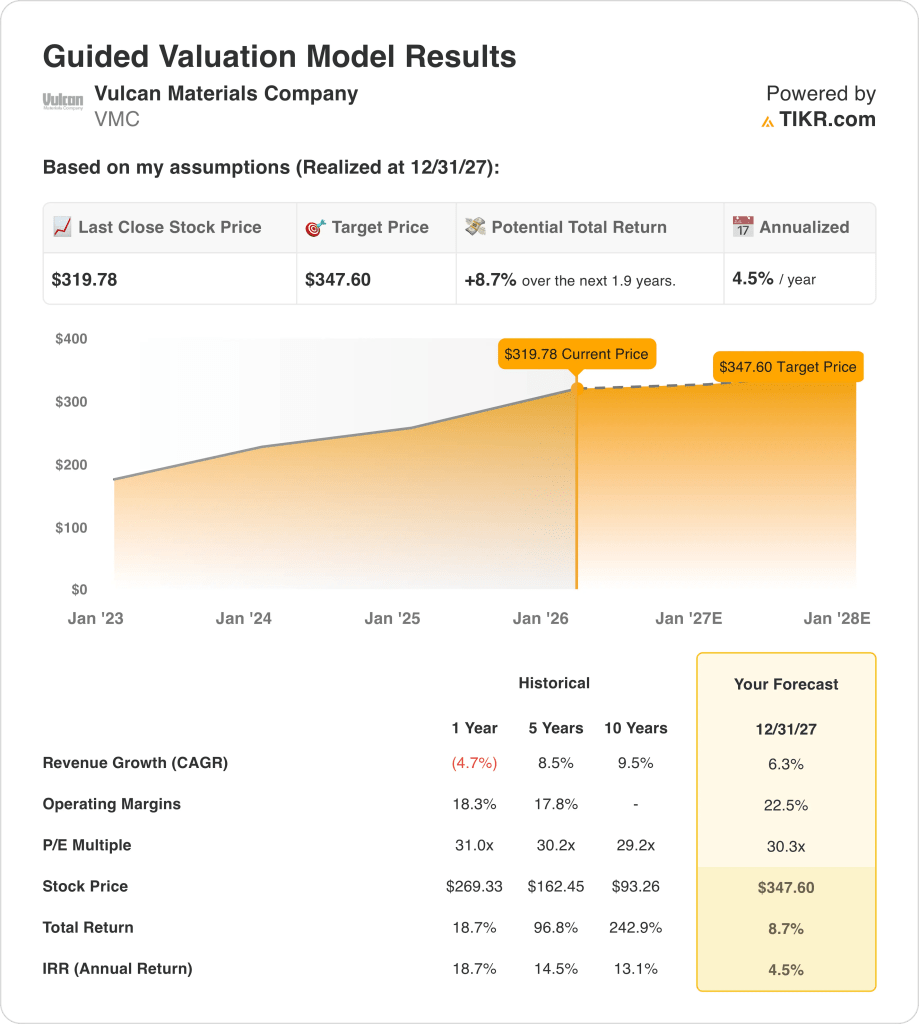

Vulcan Materials Company (VMC) approaches its Feb. 17 fourth-quarter earnings release following a 10.9% stock gain in 2025, as investors weigh infrastructure demand against valuation near 38x earnings.

The Birmingham-based aggregates producer reported Q3 revenue of $2.29 billion on Oct. 30, up 14.4% year over year, while EPS climbed 80% to $2.83 on improved pricing and freight discipline.

Meanwhile, cash gross profit per ton reached $11.51, up 13% year over year and marking the 11th consecutive quarter of double-digit profitability improvement, despite ongoing transportation cost pressure.

Aggregate shipments totaled 64.7 million tons in Q3, up 12%, although management expects shipment growth to moderate to 3% in 2025 as private construction softens.

Vulcan Materials Company guided 2025 adjusted EBITDA between $2.35 billion and $2.45 billion, implying 17% growth at the midpoint as federal and state infrastructure spending accelerates.

Currently, analysts expect Q4 revenue of $1.96 billion, down 2.7% year over year, and EPS of $2.11 versus $2.17 last year, creating a near-term execution hurdle.

Shares trade near $320 against a model target of $347.60 and 8.7% upside, leaving valuation tension between sustained infrastructure tailwinds and earnings sensitivity into 2026.

What the Model Says for VMC Stock

Vulcan Materials faces tightening investor scrutiny ahead of February 17 earnings as infrastructure demand remains solid but private construction moderates and shares trade near $320 after a 10.9% gain in 2025.

The model assumes 6.3% revenue growth through 2027, below the 5-year 8.5% CAGR, reflecting slower shipment growth after 12% third-quarter volume expansion and management’s 3% shipment outlook.

Operating margins are modeled at 22.5%, above the 1-year 18.3% level, incorporating pricing discipline and cash gross profit per ton of $11.51 following 11 consecutive quarters of double-digit improvement.

The 30.3x exit multiple aligns closely with the current 34.09x NTM P/E market assumption, embedding limited re-rating potential and recognizing cyclical risk in aggregates demand.

These inputs produce a $347.60 target price versus the current $319.78, implying 8.7% total upside and a 4.5% annualized return over 1.9 years.

A 4.5% annualized return sits well below a 10% equity hurdle rate, offering insufficient compensation for capital intensity and shipment volatility.

The model signals a Sell, as risk-adjusted returns fail to justify holding the stock at 30.3x earnings.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Vulcan Materials stock:

1. Revenue Growth: 6.3%

Vulcan Materials stock delivered 8.5% revenue CAGR over 5 years but declined 4.7% in the last year as shipment growth slowed after a 12% third-quarter volume increase.

Recent results showed $2.29 billion third-quarter revenue, up 14.4%, yet management guides aggregate shipments up 3% in 2025, framing moderation after pandemic and infrastructure surges.

Sustaining 6.3% growth requires continued federal spending and stable private demand, and any shipment shortfall compresses operating leverage and weakens earnings trajectory quickly.

This is above the 1-year revenue change of -4.7%, because infrastructure funding stabilizes volumes after a cyclical reset, and valuation depends on steady mid-cycle demand recovery.

2. Operating Margins: 22.5%

Vulcan Materials stock reported 18.3% operating margins over the last year, below the 5-year average of 17.8%, as freight costs and mix volatility influenced profitability.

Third-quarter cash gross profit per ton reached $11.51, up 13%, and marked the 11th consecutive quarter of double-digit improvement, supporting margin recovery into 2027.

Reaching 22.5% margins requires disciplined pricing and shipment consistency, and lower volumes or transport inflation compress fixed-cost absorption and erode incremental profitability.

This is above the 1-year operating margin of 18.3%, because pricing discipline and portfolio mix lift earnings power, and valuation relies on sustained cost control at higher throughput.

3. Exit P/E Multiple: 30.3x

The 30.3x exit P/E capitalizes normalized net income in 2027 and treats earnings durability as cyclical but supported by infrastructure visibility and pricing history.

The current Market assumption shows 34.09x NTM P/E, and the model adopts 30.3x to avoid layering optimism over projected margin expansion to 22.5%.

This multiple reflects normalization rather than expansion, and any earnings miss at elevated valuation levels accelerates compression as capital intensity limits balance sheet flexibility.

This is below the 1-year P/E multiple of 31.0x, because shipment cyclicality and capital intensity constrain sustained re-rating, and valuation discipline assumes limited multiple expansion.

What Happens If Things Go Better or Worse?

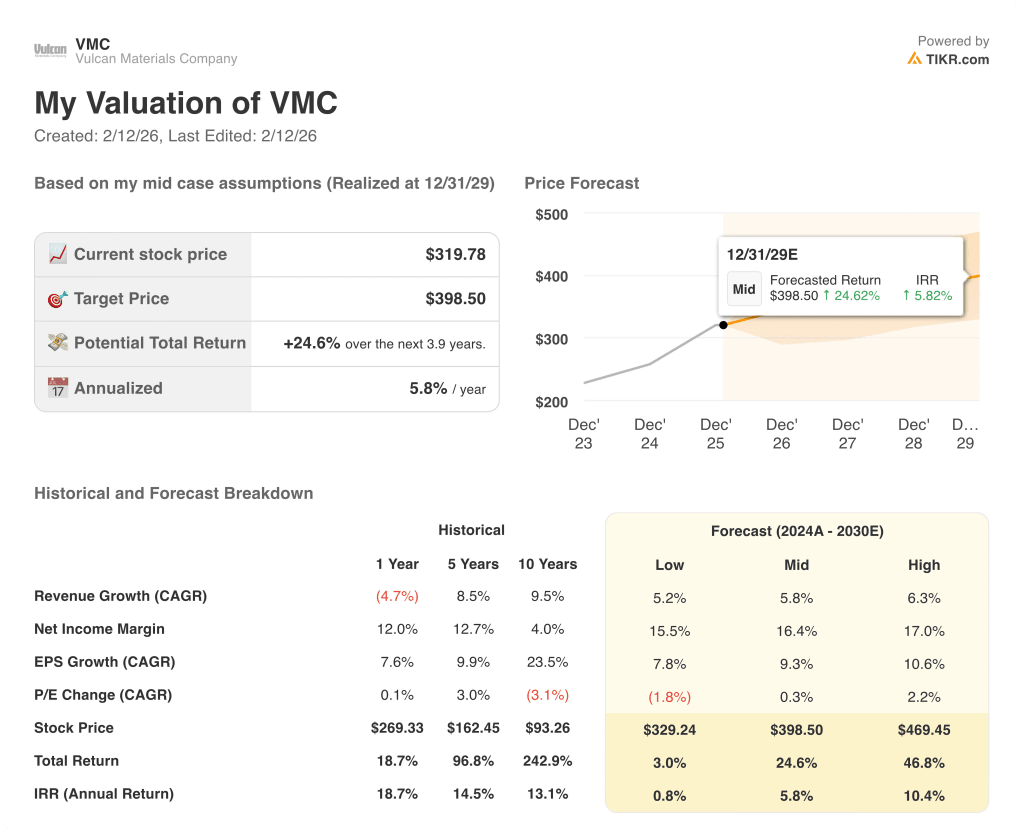

Vulcan Materials stock results hinge on aggregate shipment volumes, pricing discipline, and infrastructure funding momentum, setting up a range of operating trajectories through 2029.

- Low Case: If public spending slows and private construction weakens, revenue grows 5.2% and net margins reach 15.5% → 0.8% annualized return.

- Mid Case: With steady infrastructure demand and continued pricing gains, revenue grows 5.8% and net margins improve to 16.4% → 5.8% annualized return.

- High Case: If shipment growth accelerates and cost control lifts profitability, revenue reaches 6.3% and net margins expand to 17.0% → 10.4% annualized return.

How Much Upside Does Vulcan Materials Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!