Key Takeaways:

- AI Momentum: Now Assist surpassed $600 million in ACV with strong customer adoption across industries.

- Price Projection: Based on current execution, NOW stock could reach $172 by December 2028.

- Potential Gains: This target implies a total return of 71% from the current price of $100.74.

- Annual Return: Investors could see roughly 20% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

ServiceNow (NOW) delivered exceptional fourth-quarter results in 2025, beating expectations across all key metrics despite a challenging market environment that led to a 50% decline in its stock price over the past year.

CEO Bill McDermott highlighted the company’s position as the AI control tower for business reinvention, emphasizing that enterprise AI requires workflow orchestration to deliver real ROI. Mobile data consumption patterns show enterprises are rapidly adopting AI capabilities.

- The company reported subscription revenue of $3.466 billion, growing 19.5% year-over-year in constant currency and exceeding guidance by 150 basis points.

- ServiceNow’s Now Assist platform demonstrated this shift, with deals over $1 million nearly tripling quarter over quarter.

- The company closed 35 deals exceeding $1 million in Q4 alone, with customers expanding their AI deployments across multiple use cases.

- One consumer services company illustrated this trend by flipping its support model from 80% human-led to 80% automated after generating a 400% ROI on customer service agents. They subsequently needed 8x more assist capacity as they transitioned operations to predominantly automated interactions.

- The company’s AI control tower deal volume nearly tripled sequentially in Q4. This platform addresses critical enterprise concerns about managing autonomous agents across their operations, providing real-time monitoring, security controls, and governance that traditional tools cannot deliver.

ServiceNow benefits from multiple demand drivers beyond AI adoption. The company’s security and risk business is growing 100% year-over-year, driven by pending acquisitions of Veza and Armis, which will deliver comprehensive visibility and identity governance capabilities.

Together with ServiceNow’s business context CMDB, this creates an end-to-end security stack that can see, decide, and act across all kinds of assets – hardware, software, and AI agent assets in the same system.

Customer count grew to over 8,800, with 603 generating over $5 million in ACV. More impressively, customers contributing $20 million or more increased by more than 30% year over year, reflecting the platform’s growing strategic relevance.

Traditional metrics continue performing well. The renewal rate reached 98% in Q4, underscoring the value customers place on the platform. Technology workflows accelerated with ITOM growing nearly 50% year-over-year. CRM had its largest quarter in history.

See analysts’ full growth forecasts and estimates for NOW stock (It’s free) >>>

What the Model Says for ServiceNow Stock

We analyzed ServiceNow’s transformation into an AI control tower for enterprise business processes. The company benefits from several tailwinds working simultaneously.

First, enterprises are consolidating fragmented tool stacks. One public sector deal replaced 479 legacy tools with ServiceNow. Another customer saved $682 million by switching from a legacy CRM system.

Second, AI adoption is creating new revenue streams through consumption-based pricing. The hybrid model gives customers predictability through subscriptions while allowing them to scale usage with assist packs as they deploy more AI agents.

Third, strategic partnerships with Microsoft, Anthropic, and OpenAI are deepening product integration and expanding use cases across the platform.

Using a forecast of 19.3% annual revenue growth and 33.5% operating margins, our model projects the stock will rise to $172 within 2.9 years. This assumes a 24.2x price-to-earnings multiple.

That represents significant compression from ServiceNow’s historical P/E averages of 49.6x (one year) and 54x (three years). The lower multiple reflects near-term concerns about AI monetization timelines and competitive dynamics in enterprise software.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for NOW stock:

1. Revenue Growth: 19.3%

ServiceNow’s growth is driven by the shift to agentic AI and workflow automation. The company reported 19.5% constant-currency subscription growth in Q4, with strong performance across all product lines.

Management expects momentum to continue as enterprises move from pilot projects to production deployments of AI agents.

The 25% growth in monthly active users shows that seat compression fears are overblown.

2. Operating margins: 33.5%

ServiceNow expanded operating margins by 150 basis points in 2025 to reach 31%. The company is guiding to 32% for 2026, demonstrating strong operating leverage.

AI is actually helping margins through internal efficiency gains. Management noted that AI-enabled OpEx savings are contributing to margin expansion.

3. Exit P/E Multiple: 24.2x

The market currently values ServiceNow at 24.2x earnings, matching our target multiple. As the company proves out AI monetization and maintains high growth rates, this multiple should hold or potentially expand.

ServiceNow trades at a discount to its historical valuation despite having a stronger competitive position today.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

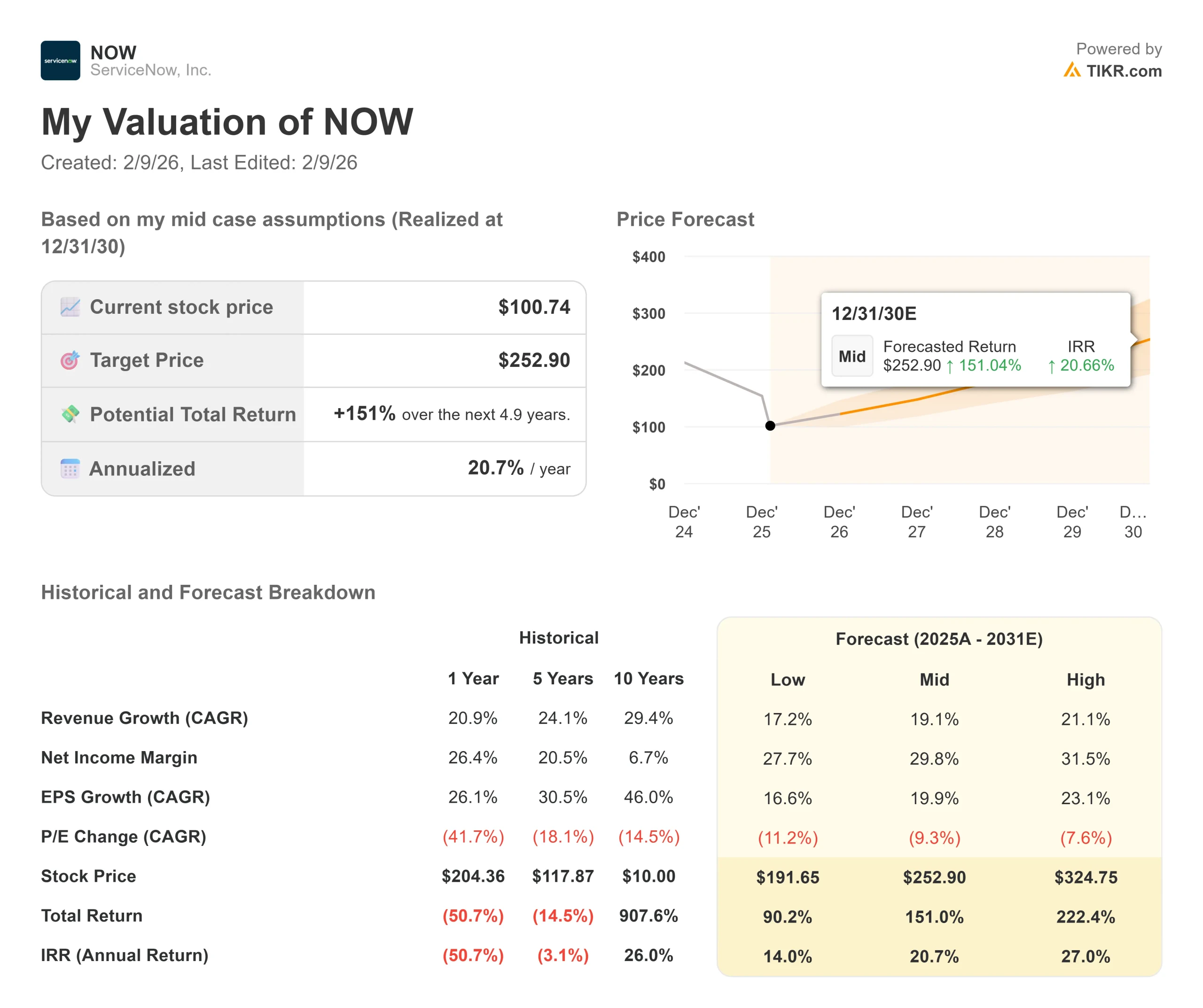

Enterprise software faces execution risk and competitive threats. Here’s how ServiceNow stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 17.2% and net income margins compress to 27.7%, investors still see a 90% total return (14% annually).

- Mid Case: With 19.1% growth and 29.8% margins, we expect a total return of 151% (20.7% annually).

- High Case: If AI adoption accelerates, driving 21.1% revenue growth while ServiceNow maintains 31.5% margins, returns could hit 222% total (27% annually).

See what analysts think about NOW stock right now (Free with TIKR) >>>

The range reflects execution on AI monetization, successful integration of acquisitions, and the company’s ability to consolidate enterprise software spend onto its platform.

In the low case, competitive pressure from AI-native startups or hyperscalers could slow growth.

In the high case, ServiceNow becomes the dominant platform for enterprise AI, capturing share from legacy software vendors while expanding into new markets.

How Much Upside Does ServiceNow Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!