Key Takeaways:

- AI Momentum: Over 1 billion AI actions executed on the platform in 2025, with AI products adding 1.5 points to ARR growth.

- Price Projection: Based on current execution, WDAY stock could reach $192 by January 2028.

- Potential Gains: This target implies a total return of 33% from the current price of $145.

- Annual Return: Investors could see roughly 16% growth over the next 2 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Workday (WDAY) delivered solid third-quarter fiscal 2026 results with 15% subscription revenue growth and 28.5% non-GAAP operating margin, demonstrating the strength of its unified HR and finance platform.

CEO Carl Eschenbach highlighted the company’s competitive advantage: organizations are struggling with disconnected systems and poor data quality as they attempt to implement AI.

- Workday’s unified platform delivers business-ready AI that helps companies adapt quickly and drive measurable outcomes.

- The company’s AI momentum is accelerating rapidly. More than 75% of core customers now use Workday Illuminate AI, generating over 1 billion AI actions in 2025 alone.

- Three-quarters of new deals and 35% of customer expansions included AI products, with standout performers like Evisort achieving record quarters and Extend Pro growing net new ACV by over 50% year-over-year.

- Workday’s recent acquisitions strengthen its AI capabilities. The Paradox acquisition closed in Q3 and immediately contributed to revenue. Sana, an AI-native platform, will reimagine Workday’s user experience and bring hyper-personalized skill development to Workday Learning.

- The pending Pipedream acquisition adds 3,000 prebuilt connectors, enabling Workday agents to truly get work done across the enterprise.

Despite strong fundamentals and market-leading AI capabilities, Workday trades at $145, leaving room for upside for investors who recognize the company’s position in critical enterprise software infrastructure.

See analysts’ full growth forecasts and estimates for WDAY stock (It’s free) >>>

What the Model Says for Workday Stock

We analyzed Workday’s transformation into a leading AI-powered platform for HR and finance.

Organizations need unified data and business context to implement AI successfully. Workday’s platform provides both, with one of the largest and cleanest curated datasets for HR and finance in the industry.

This positions the company to capture AI spending that might otherwise go to point solutions.

Customer retention remains healthy at 97% gross revenue retention, while headcount across the customer base continues growing modestly.

The company is expanding beyond large enterprises through Workday GO, which now includes Global Payroll and an AI-powered deployment agent that cuts implementation time by 25%.

International markets delivered solid performance across EMEA, APAC, and Japan. The new EU Sovereign Cloud lets customers run AI-powered solutions entirely within the EU, addressing data sovereignty requirements.

New offices in Dubai and expanded operations in India open additional growth opportunities.

Using a forecast of 12.4% annual revenue growth and 31.8% operating margins, our model projects the stock will rise to $192 within 2 years. This assumes a 14x price-to-earnings multiple.

That represents compression from Workday’s historical P/E averages of 25.3x (one year) and 33.4x (three years). The lower multiple reflects the stock’s recent underperformance and market uncertainty around AI monetization timelines, despite strong early traction.

The real value lies in Workday’s unique position to monetize AI across its customer base while maintaining healthy margins through operational efficiency.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for WDAY stock:

1. Revenue Growth: 12.4%

Workday’s growth centers on AI-driven platform expansion and international market penetration.

Management expects FY27 subscription revenue growth of approximately 13%, supported by strong Q3 performance and Q4 cRPO guidance of 15-16%.

AI products added 1.5 points to ARR growth in Q3. As adoption expands, this contribution should increase. For example, when Workday sells its HiredScore recruiting agent, it generates $2.50 in revenue for every dollar of standard recruiting revenue.

The Workday GO expansion targets the mid-enterprise market with Global Payroll and simplified deployment.

Combined with continued penetration of large enterprises adding both HR and finance (50% of new deals in Q3), the company has multiple growth vectors supporting double-digit expansion.

2. Operating margins: 31.8%

Workday targets continued margin expansion while investing in AI capabilities.

The company achieved 28.5% non-GAAP operating margin in Q3 and expects approximately 29% for full-year FY26.

Management is driving efficiency through automation and scale, while making targeted investments in AI talent, new markets such as the Middle East and India, and the mid-enterprise segment.

The financial framework targets margin expansion on both GAAP and non-GAAP bases through FY28.

3. Exit P/E Multiple: 14x

The market currently values Workday at 14.2x earnings. We assume the P/E holds steady at 14x over our forecast period.

This conservative multiple reflects recent stock weakness and market skepticism about AI revenue conversion, despite Workday’s demonstrated tangible AI monetization.

As the company continues proving AI-driven growth and margin expansion, the multiple should re-rate higher toward historical averages.

The platform’s competitive moat is strengthening. Customers increasingly view Workday as their AI strategy partner rather than evaluating fragmented point solutions, as evidenced by Microsoft partnering with Workday to manage both human and digital workers.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Enterprise software faces execution risks around AI adoption and competitive dynamics. Here’s how Workday stock might perform under different scenarios through January 2030:

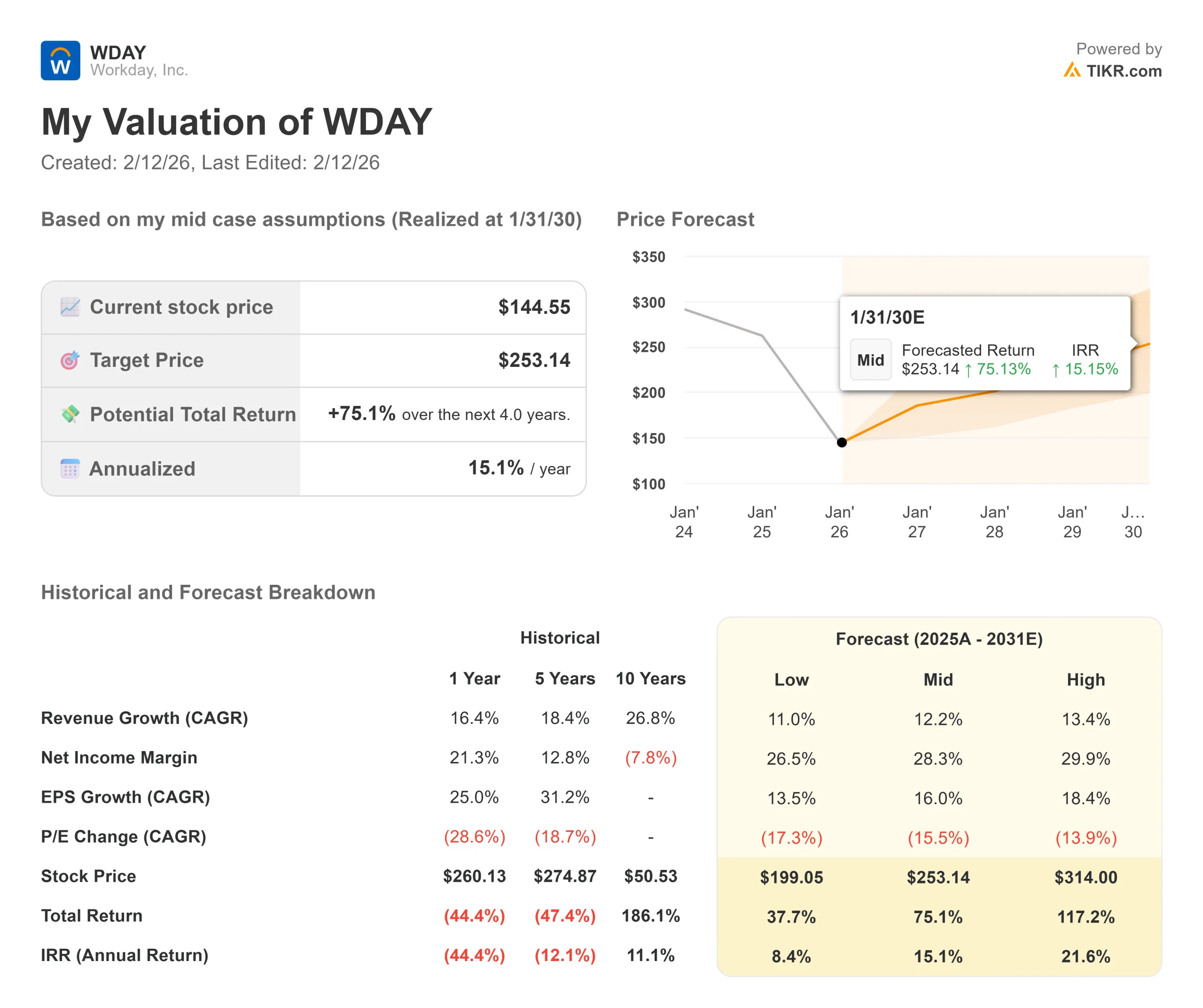

- Low Case: If revenue growth slows to 11% and net income margins compress to 26.5%, investors still see a 38% total return (8.4% annually).

- Mid Case: With 12.2% growth and 28.3% margins, we expect a total return of 75% (15.1% annually).

- High Case: If AI acceleration drives 13.4% revenue growth while Workday maintains 29.9% margins, returns could hit 117% total (21.6% annually).

See what analysts think about WDAY stock right now (Free with TIKR) >>>

The range reflects execution on AI monetization, success expanding into new markets and customer segments, and the ability to maintain pricing power while delivering measurable business value through purpose-built AI agents for HR and finance.

How Much Upside Does Workday Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!