Key Takeaways:

- IAM Growth: DocuSign’s Intelligent Agreement Management platform now has 25,000+ customers, up from 10,000 in April.

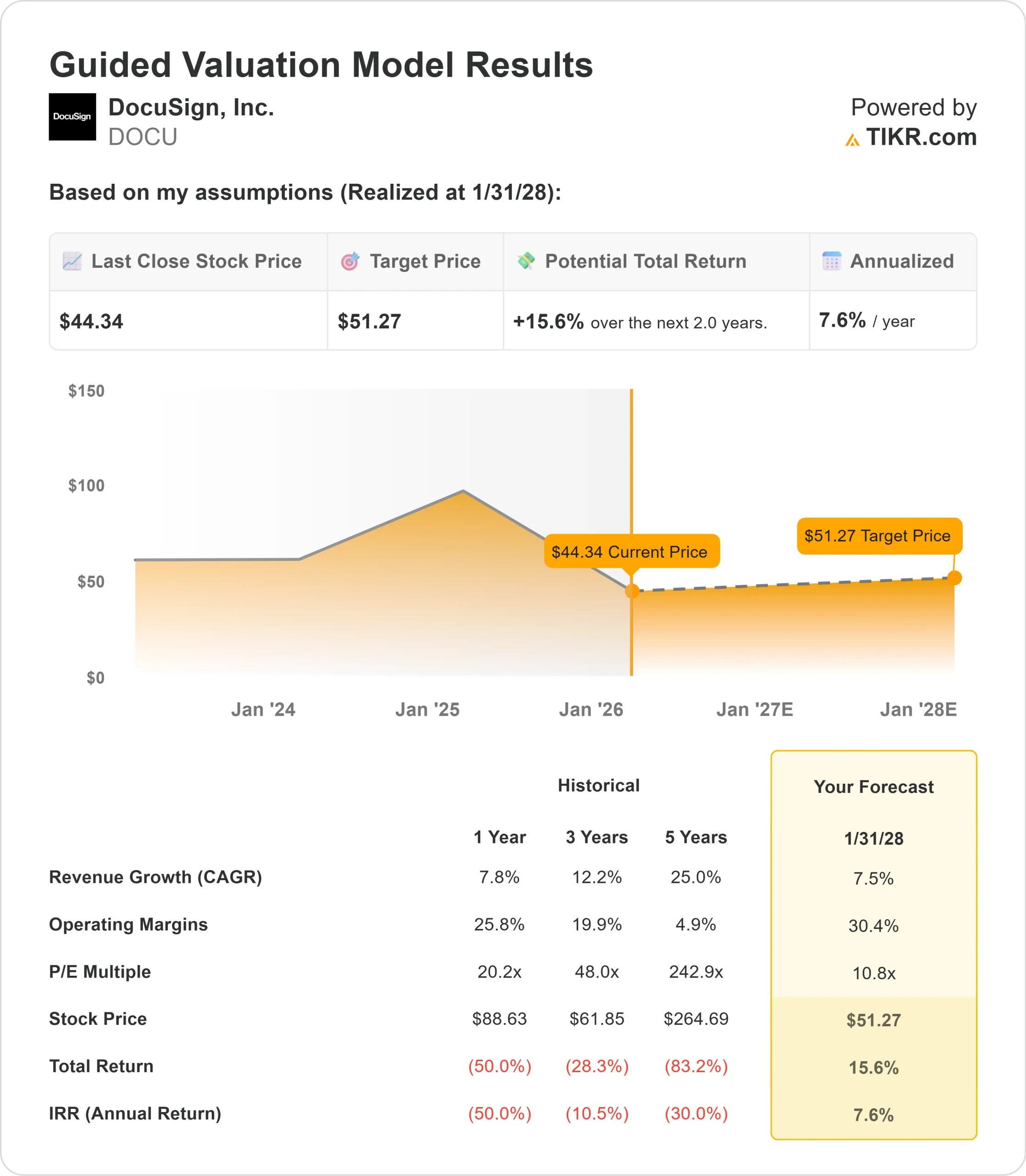

- Price Projection: Based on current execution, DOCU stock could reach $51 by January 2028.

- Potential Gains: This target implies a total return of 16% from the current price of $44.

- Annual Return: Investors could see roughly 8% growth over the next 2 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

DocuSign (DOCU) delivered a standout third quarter in fiscal 2026 with revenue of $818 million, up 8% year-over-year, and billings of $829 million, up 10% year-over-year.

CEO Allan Thygesen highlighted the growing value proposition.

- One of DocuSign’s top 10 customers became the second-largest this quarter through a multimillion-dollar commitment to IAM.

- Companies using IAM generate new documents 99% faster and reduce agreement finalization time by 96%.

- The company’s strategic shift toward Intelligent Agreement Management (IAM) is gaining momentum.

- More than 25,000 paying customers have adopted IAM by the end of Q3, and the platform is on pace to represent a low double-digit percentage of recurring revenue at year-end.

- The broader eSignature business also performed well. Dollar net retention improved by two percentage points year-over-year to 102%, with utilization rates at multiyear highs and consistent growth in envelopes sent.

- International revenue reached 30% of total revenue for the first time, growing 14% year-over-year.

Despite these fundamentals and a category-leading platform position, DocuSign trades at $44, offering upside for investors who recognize the company’s transformation from a single-product eSignature provider into a comprehensive agreement management platform.

See analysts’ full growth forecasts and estimates for DOCU stock (It’s free) >>>

What the Model Says for DocuSign Stock

We analyzed DocuSign’s evolution into the category leader in intelligent agreement management.

The company benefits from multiple demand drivers. IAM customers show higher retention rates than the corporate average, and they typically increase their eSignature usage after moving to the platform.

The expansion opportunity is substantial—DocuSign has nearly 270,000 active direct customers, providing significant headroom for IAM adoption.

DocuSign’s competitive advantages center on three pillars.

- First, the company has an unmatched library of consented, private agreements. Training IAM on this proprietary data delivers a 15-percentage-point improvement in precision and recall compared with models trained on public contract data.

- Second, DocuSign maintains over 1,000 third-party integrations and enterprise-ready APIs. Recent partnerships with ChatGPT, Anthropic Claude, and Salesforce Agentforce position DocuSign as the essential agreement layer across the enterprise.

- Third, customers trust DocuSign’s enterprise-scale security. In a recent survey, 70% of professionals said they trust a dedicated enterprise contract AI solution over a general-purpose model for handling agreements.

Using a forecast of 7.5% annual revenue growth and 30.4% operating margins, our model projects the stock will rise to $51 within 2 years. This assumes a 10.8x price-to-earnings multiple.

That represents compression from DocuSign’s historical P/E averages of 20.2x (one year) and 48x (three years). The lower multiple reflects the stock’s significant decline over the past year and market uncertainty around the pace of IAM adoption.

The real value lies in capturing DocuSign’s transformation into a platform company while maintaining strong profitability and free cash flow generation.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DOCU stock:

1. Revenue Growth: 7.5%

DocuSign’s growth centers on IAM platform adoption across its installed base. The company delivered 8% revenue growth in Q3, with IAM contributing an increasing share.

Management expects IAM to represent a low double-digit percentage of the subscription book by year-end.

The first renewal cohorts show gross retention rates several percentage points higher than the corporate average, validating the platform’s value.

International markets provide additional upside, now representing 30% of revenue and growing 14% year-over-year.

The company is expanding solution-selling motions across sales, procurement, HR, and customer experience use cases.

2. Operating margins: 30.4%

DocuSign delivered a 31.4% non-GAAP operating margin in Q3, up nearly 2 percentage points year-over-year.

This performance reflects higher revenue, continued cost discipline, and operational efficiency gains.

The company maintains a measured approach to hiring while investing in strategic areas like product development and security.

Management expects to achieve flat year-over-year operating margins for fiscal 2026 despite headwinds from cloud migration costs.

3. Exit P/E Multiple: 10.8x

The market currently values DocuSign at 11.1x earnings on an NTM basis. We assume a slight compression to 10.8x over our forecast period.

This conservative multiple reflects uncertainty around the pace of platform transformation and competitive dynamics in the agreement management space.

However, as DocuSign demonstrates sustained IAM adoption and customers realize measurable productivity gains, the company should command a higher valuation than current levels suggest.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

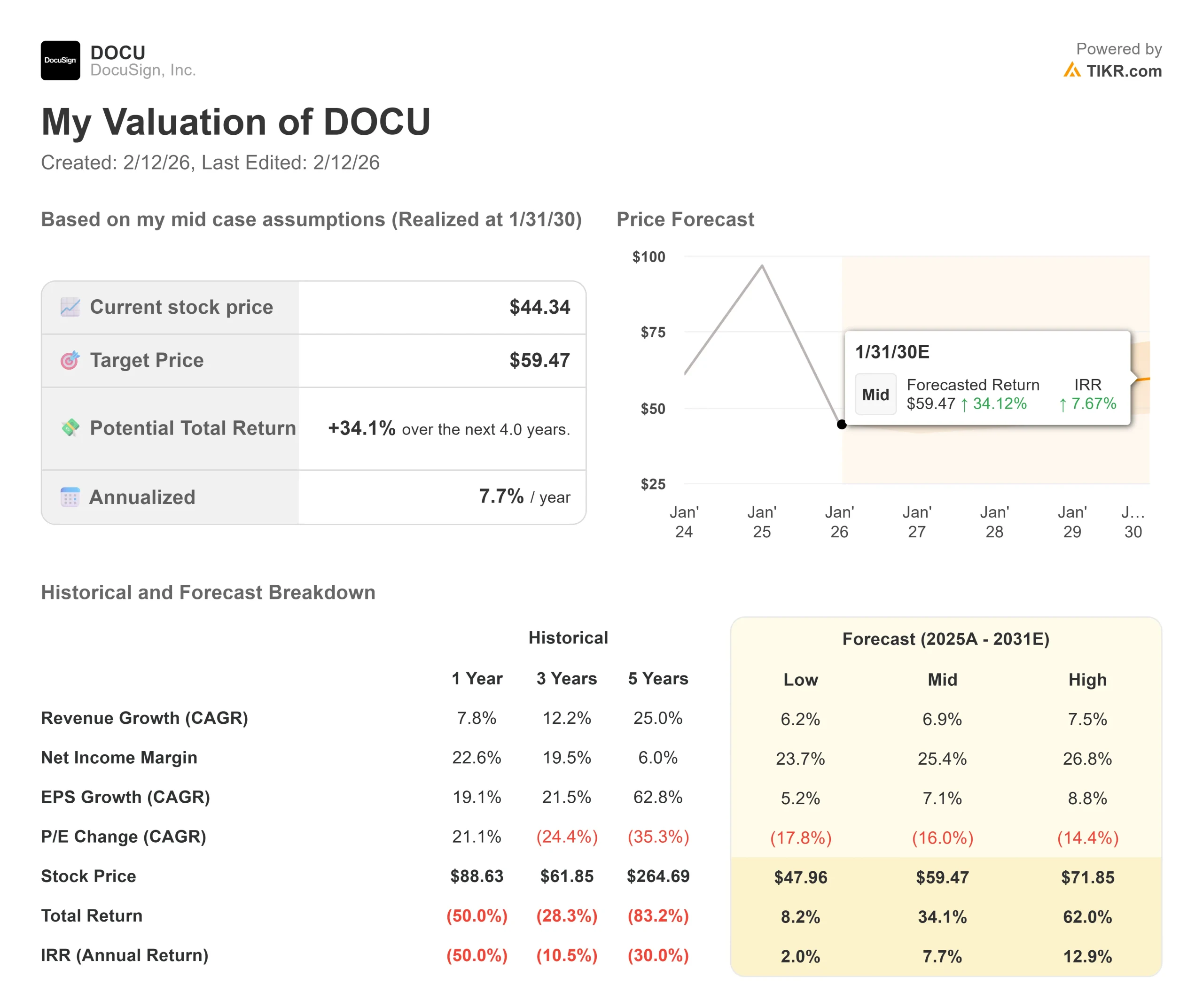

Technology platform transitions carry execution risk. Here’s how DocuSign stock might perform under different scenarios through January 2030:

- Low Case: If revenue growth slows to 6.2% and net income margins compress to 23.7%, investors still see an 8.2% total return (2.0% annually).

- Mid Case: With 6.9% growth and 25.4% margins, we expect a total return of 34.1% (7.7% annually).

- High Case: If IAM adoption accelerates to drive 7.5% revenue growth while DocuSign maintains 26.8% margins, total returns could reach 62.0% (12.9% annually).

See what analysts think about DOCU stock right now (Free with TIKR) >>>

The range reflects execution on IAM deployment, successful navigation of the eSignature-to-platform transition, and the company’s ability to expand across enterprise agreement workflows.

In the low case, IAM adoption slows or competitive pressures intensify.

In the high case, the platform vision materializes faster than expected, driving both revenue acceleration and margin expansion as customers consolidate agreement workflows onto DocuSign.

How Much Upside Does DocuSign Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!