Key Takeaways:

- AI Innovation: Manhattan just launched commercial AI agents, creating immediate upsell opportunities across its cloud customer base.

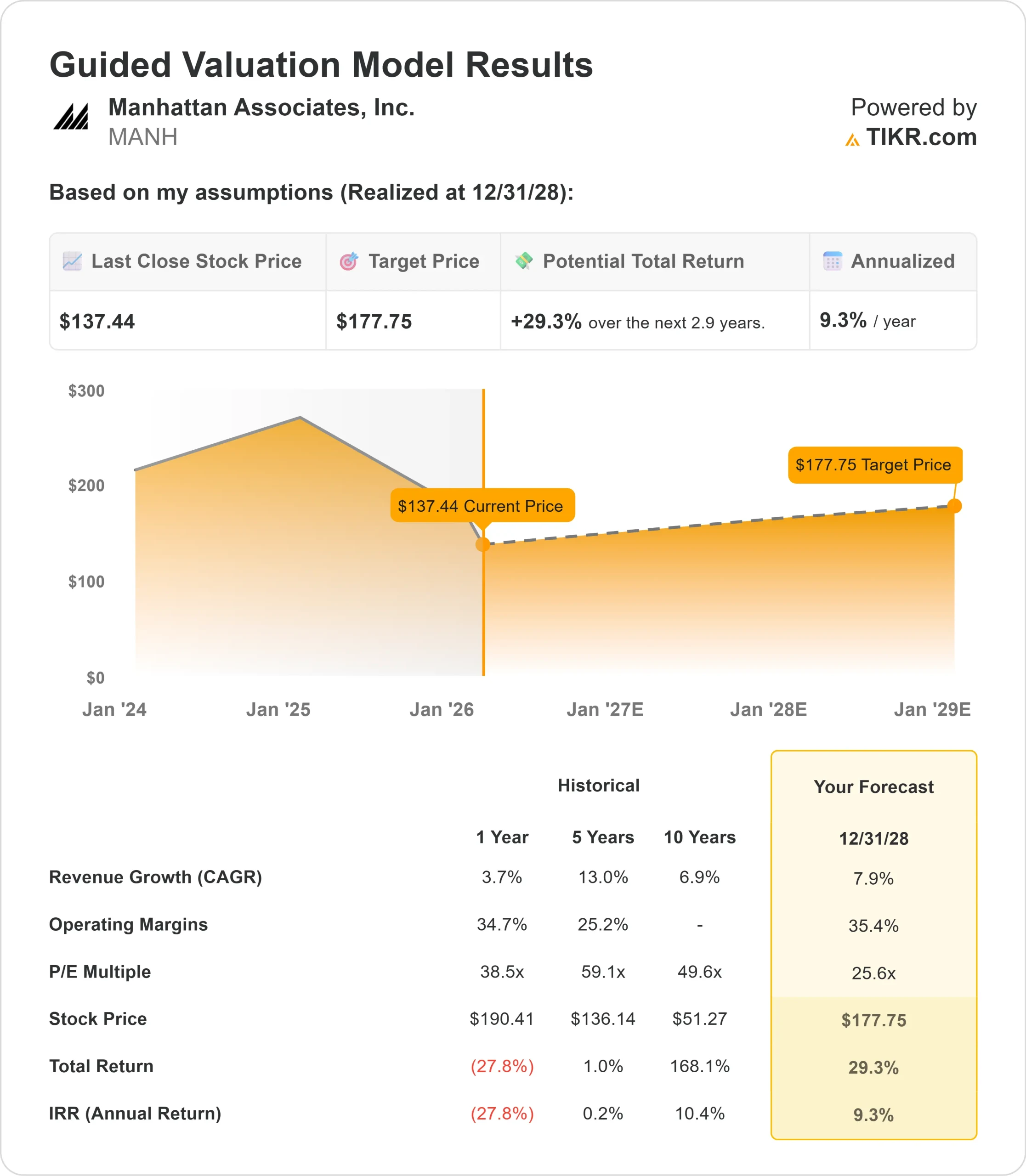

- Price Projection: Based on current execution, MANH stock could reach $178 by December 2028.

- Potential Gains: This target implies a total return of 29% from the current price of $137.

- Annual Return: Investors could see roughly 9% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Manhattan Associates (MANH) delivered a record fourth quarter in 2025, with cloud bookings hitting all-time highs and the company raising its 2026 guidance across the board.

CEO Eric Clark highlighted momentum across the business. Cloud revenue grew 20% in Q4, while the company’s remaining performance obligation (RPO) surged 25% year-over-year to $2.2 billion.

More than 75% of new cloud bookings came from net new logos, demonstrating Manhattan’s ability to capture market share in the competitive supply chain software space.

- The company introduced a new metric, “ramped ARR” (annualized recurring revenue at full pricing), which reached $600 million at year-end, up 23% from 2024.

- This metric provides better visibility into Manhattan’s cloud revenue trajectory since many contracts reach full pricing by year four.

- Several weeks ago, Manhattan announced commercial availability of its AI agents and Agent Foundry. Early adopter feedback suggests these tools deliver significant value by increasing automation and productivity.

- Unlike competitors that require costly data lake implementations, Manhattan’s API-first architecture enables customers to activate AI agents immediately within their existing Active platform.

- The company’s diverse customer base spans retail, grocery, industrial, life sciences, and third-party logistics.

- Recent Q4 wins included a Fortune 100 home improvement company, an upscale department store chain, and the world’s largest medical surgical products provider.

- For 2026, management expects RPO to reach $2.62 to $2.68 billion (representing 18% to 20% growth), total revenue of $1.14 billion (6% growth, or 10% excluding legacy maintenance and license declines), and cloud revenue of $492 million (21% growth).

See analysts’ full growth forecasts and estimates for MANH stock (It’s free) >>>

What the Model Says for Manhattan Associates Stock

We analyzed Manhattan’s transformation into a dominant supply chain software provider, with expanding AI capabilities.

The company benefits from three powerful demand drivers.

- First, new customer acquisition continues at a rapid pace, with Manhattan winning deals across multiple verticals.

- Second, the installed base of on-premise customers represents a massive conversion opportunity. Manhattan launched fixed-fee conversion programs in mid-2025 that are now accelerating.

- Third, AI agents create an entirely new revenue stream. For the first time since launching cloud products, Manhattan can offer immediate upsells to every cloud customer simultaneously. The company hired 100 new service associates in January 2026 to support this opportunity.

Using a forecast of 7.9% annual revenue growth and 35.4% operating margins, our model projects the stock will rise to $178 within 2.9 years. This assumes a 25.6x price-to-earnings multiple.

That represents compression from Manhattan’s historical P/E averages of 38.5x (one year) and 59.1x (five years). The lower multiple acknowledges near-term investments in sales, marketing, and services capacity to capture the AI opportunity.

The real value lies in Manhattan’s ability to monetize AI agents while maintaining industry-leading retention rates and expanding its unified platform across warehouse, transportation, order management, and point-of-sale applications.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MANH stock:

1. Revenue Growth: 7.9%

Manhattan’s growth centers on winning new logos, converting on-premise customers to cloud, and cross-selling additional products.

The company delivered exceptional new-customer performance in 2025, but management expects the mix to normalize over time to one-third new logos, one-third conversions, and one-third expansions.

Cloud conversions are accelerating. Manhattan now offers fixed-fee, fixed-timeline deals that give customers confidence in implementation speed.

The company already closed several conversions in early 2026.

AI agents represent fresh upside. Manhattan is offering low-risk 90-day pilots with forward-deployed engineers to demonstrate value.

Early adopters indicate these agents drive significant productivity gains through increased automation.

2. Operating margins: 35.4%

Manhattan has expanded adjusted EBITDA margins to 36.4% for the full year, driven by operational efficiency and disciplined cost management.

The company targets 75 basis points of margin expansion in 2026 when excluding legacy maintenance and license headwinds.

However, Manhattan is investing heavily in growth through new sales hires, expanded partner programs, and the addition of 100 service associates in January.

3. Exit P/E Multiple: 25.6x

The market values Manhattan at 26.4x earnings today. We assume a slight compression to 25.6x over our forecast period.

This conservative multiple accounts for execution risk around AI monetization timing and the ongoing cloud transition.

Given Manhattan’s consistent AI revenue contribution and win rates above 70%, the company should command a premium valuation.

Management’s world-class gross retention rates provide confidence. The ramped ARR metric assumes no churn and no price increases, creating upside potential as customers renew at higher pricing.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

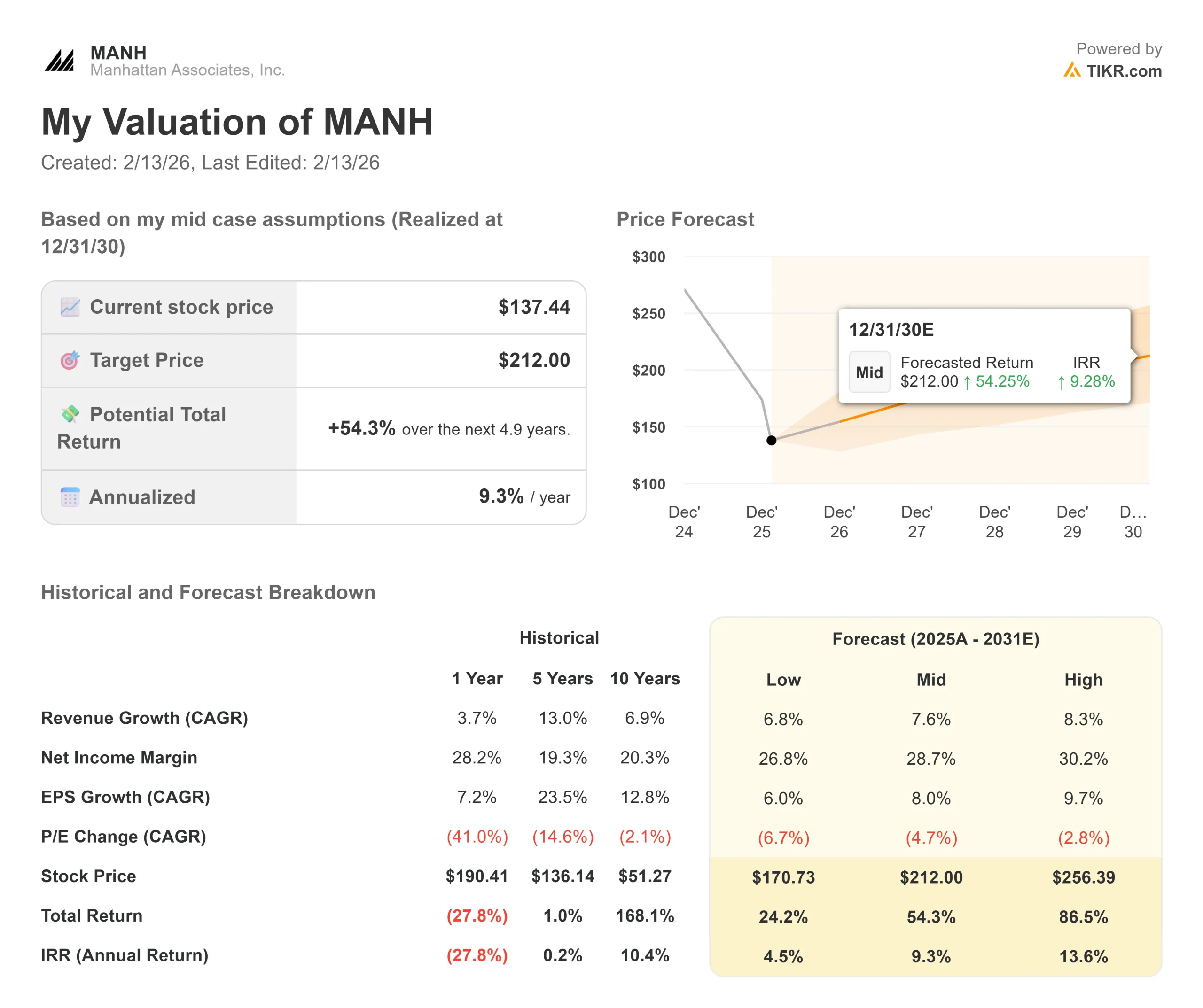

Supply chain software faces technology transitions and implementation cycles. Here’s how Manhattan stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 6.8% and net income margins compress to 26.8%, investors still see a 24% total return (4.5% annually).

- Mid Case: With 7.6% growth and 28.7% margins, we expect a total return of 54% (9.3% annually).

- High Case: If AI adoption accelerates and drives 8.3% revenue growth while Manhattan maintains 30.2% margins, returns could hit 87% (13.6% annually).

See what analysts think about MANH stock right now (Free with TIKR) >>>

The range reflects execution on AI monetization, successful cloud conversions, and competitive positioning.

In the bear case, AI adoption disappoints or capacity constraints limit growth.

In the bull case, AI creates substantial incremental revenue while operational leverage drives faster margin expansion.

How Much Upside Does Manhattan Associates Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!