Key Takeaways:

- Tariff-Driven Ad Shock: Pinterest absorbed a tariff-related pullback from large retail advertisers, and Q4 revenue of $1,319 million missed expectations while global MAUs still hit a record 619 million, up 12%.

- AI And Go-To-Market Reset: Pinterest announced a restructuring of less than 15% and shifted resources toward AI-led products, while installing a new Chief Business Officer to accelerate sales execution and broaden the advertiser mix beyond large retailers.

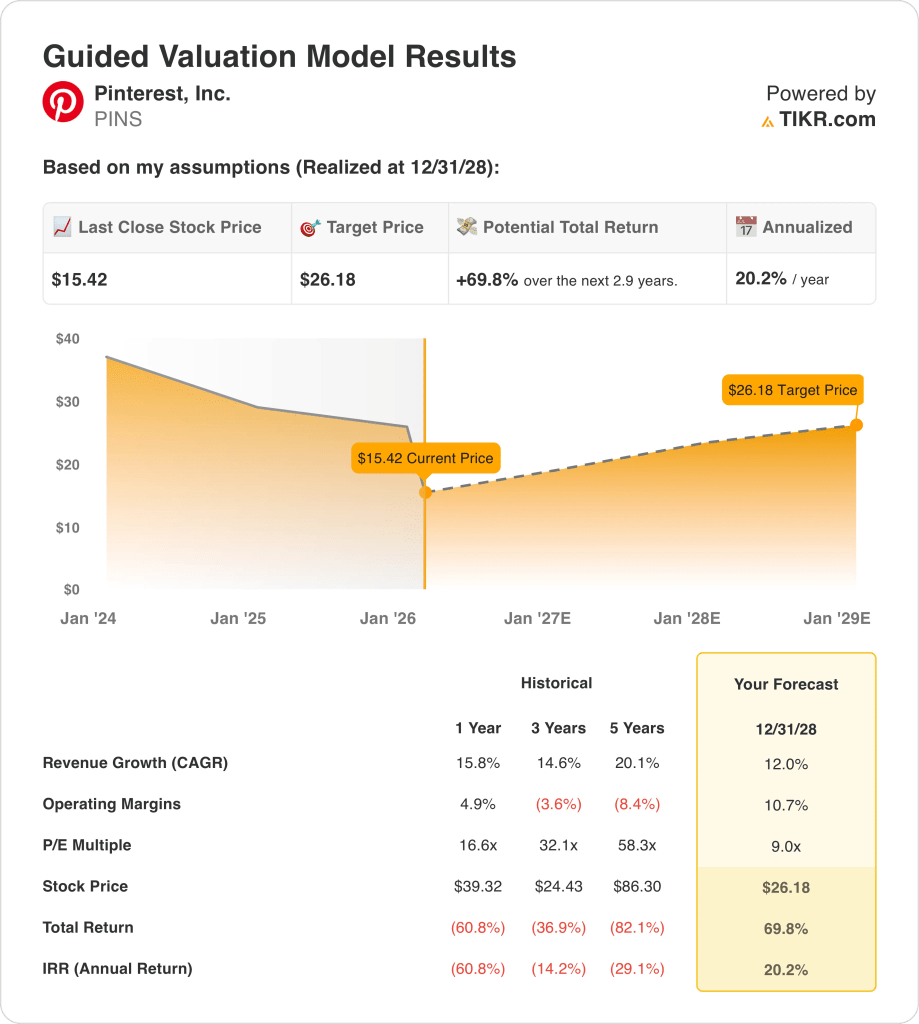

- Valuation Target: Pinterest stock could reach $26 by 2028 as the model assumes 12% revenue growth and a 11% operating margin while the market prices the business at a 9x P/E multiple.

- Modeled Upside: Pinterest implies 70% upside from the current $15 price to $26 by 2028, representing about 20% annualized returns over roughly 3 years based on valuation math.

Breaking Down the Case for Pinterest, Inc.

Pinterest, Inc. (PINS) fell 17% to $15 after Q4 results highlighted tariff-driven pressure on large retailer ad budgets and guided Q1 revenue to $951 million to $971 million, below the $980 million consensus.

Q4 revenue reached $1.32 billion, while adjusted EBITDA of $542 million held margin at 41%, even as management flagged weaker demand visibility from UCAN and Europe advertisers.

For 2025, Pinterest stock’s revenue totaled $4.22 billion and gross profit reached $3.38 billion, supporting an 80% gross margin despite higher infrastructure spend tied to user growth and AI capacity.

Total operating expenses of $3.06 billion left operating income at $320 million and operating margin at 8%, showing the business returned to positive EBIT after negative margins in 2022 and 2023.

In an earnings call for Q4 of 2025, CEO Bill Ready said the company “absorbed an exogenous shock this year related to tariffs,” and he framed the 2026 plan around accelerating monetization so revenue better tracks 619 million users and 80 billion monthly searches.

Management paired that reset with a restructuring of less than 15% to reallocate talent toward AI-focused teams, and the company expects 2026 adjusted EBITDA margin near 30% even after $100 million of annualized OpEx savings gets partly reinvested.

The debate now centers on whether a $15 stock price and a 9x P/E exit multiple fairly reflect 12% modeled growth and a 11% operating margin by 2028 after Q1 guidance of 11% to 14% growth resets market expectations.

What the Model Says for PINS Stock

According to market assumption, Pinterest stock trades at 2.16x next year’s sales and 9.02x next year’s earnings, down from 4.90x sales and 17.14x earnings as investors reset expectations after tariff-related weakness.

The model applies 12% revenue growth and 10.7% operating margins versus 12.4% 2026 revenue growth and 7.9% EBIT margins implied in forward estimates, alongside a 9x exit multiple that aligns with the current 9.02x market assumption.

At $15.42, the stock is valued at 5.74x next year’s EBITDA and 8.07x next year’s free cash flow, while analysts expect $4.75 billion in revenue and 29.6% EBITDA margins in 2026, pointing to profit recovery.

That valuation model framework produces a $26.18 target price with 70% total upside and 20.2% annualized return over 2.9 years, and the model therefore signals a Buy as depressed multiples price cyclical risk below normalized cash flow power.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PINS stock:

1. Revenue Growth: 12%

Pinterest stock revenue grew 15.8% in 2025 after 19.3% in 2024, showing deceleration as tariff pressure hit large retail advertisers and shifted mix toward smaller and international accounts.

Consensus projects 12.4% revenue growth for 2026 on $4.75 billion of sales, supported by 619 million MAUs and 80 billion monthly searches, while pricing pressure and advertiser mix remain headwinds.

The 12.0% market assumption requires sustained advertiser diversification and improved monetization per user, and revenue undershoot quickly reduces operating leverage given fixed AI and sales investments.

This is below the 1-year revenue growth of 15.8%, as retailer concentration and pricing declines constrain near-term acceleration and limit valuation re-expansion without execution gains.

2. Operating Margins: 10.7%

Pinterest stock delivered 7.6% EBIT margin in 2025 after negative margins in 2022 and 2023, showing recovery but still below prior profitability levels.

Forward estimates imply 7.9% EBIT margin for 2026 while EBITDA margins hold near 29.6%, with cost discipline offset by higher GPU and AI infrastructure spending.

The 10.7% market assumption depends on fixed-cost leverage from revenue scaling and stable ad pricing, and margin slippage materially reduces earnings power at a 9x exit multiple.

This is above the 1-year EBIT margin of 7.6%, as incremental margin expansion relies on ad pricing stability and sales execution while cost growth remains embedded.

3. Exit P/E Multiple: 9x

Pinterest stock trades at 9.02x NTM price to normalized earnings under market assumption after shares fell 17% on tariff-driven weakness from large retail advertisers and Q1 guidance of $951 million to $971 million.

The model applies a 9.0x exit P/E on 2028 normalized earnings, matching current market assumption while incorporating 12.0% revenue growth and 10.7% operating margins without assuming valuation expansion.

This multiple assumes monetization improves through AI-led products and sales restructuring, and failure to offset retailer concentration risk limits earnings durability and pressures the 9.0x valuation anchor.

This sits below the 1-year P/E of 16.6x, as investor caution around advertiser pullbacks and restructuring execution constrains Pinterest stock from reclaiming prior premium levels.

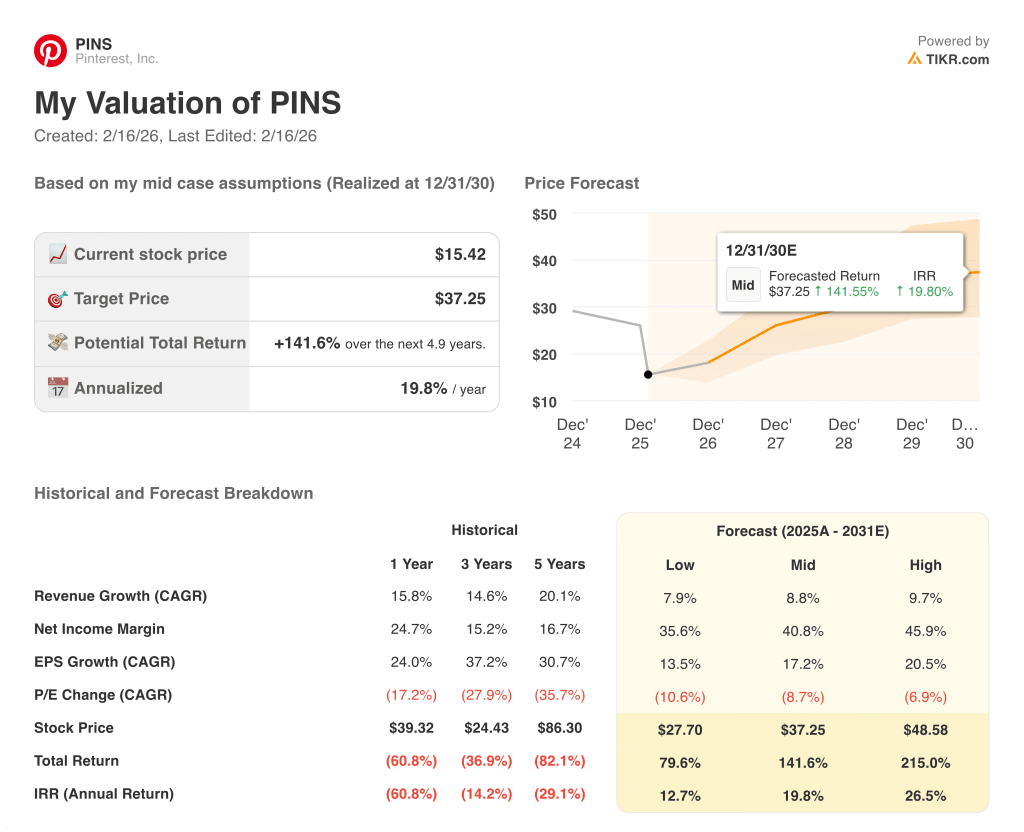

What Happens If Things Go Better or Worse?

Pinterest stock results are shaped by tariff-driven retailer pullbacks, 619 million MAUs monetization, AI product execution, and cost control discipline through 2030.

- Low Case: If retailer weakness persists and monetization lags, revenue grows 7.9% and net margins reach 35.6% → 12.7% annualized return.

- Mid Case: With AI tools scaling and advertiser mix stabilizing, revenue grows 8.8% and net margins reach 40.8% → 19.8% annualized return.

- High Case: If monetization accelerates and cost leverage expands, revenue grows 9.7% and net margins reach 45.9% → 26.5% annualized return.

How Much Upside Does Pinterest Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!