Key Takeaways:

- Breeze Integration Milestone: Valvoline Inc. completed its acquisition of 162 Breeze Autocare stores for $593 million in December 2025, expanding its network toward a 3,500-store target and adding $160 million in projected revenue for the 10 months of fiscal 2026 ownership.

- Q1 Momentum Reset: Valvoline Inc. delivered Q1 2026 net sales of $462 million and adjusted EPS of $0.37, reflecting 15% revenue growth and 6% same-store sales expansion that beat Street expectations and reaffirmed fiscal 2026 guidance of $2.0 billion to $2.1 billion in revenue.

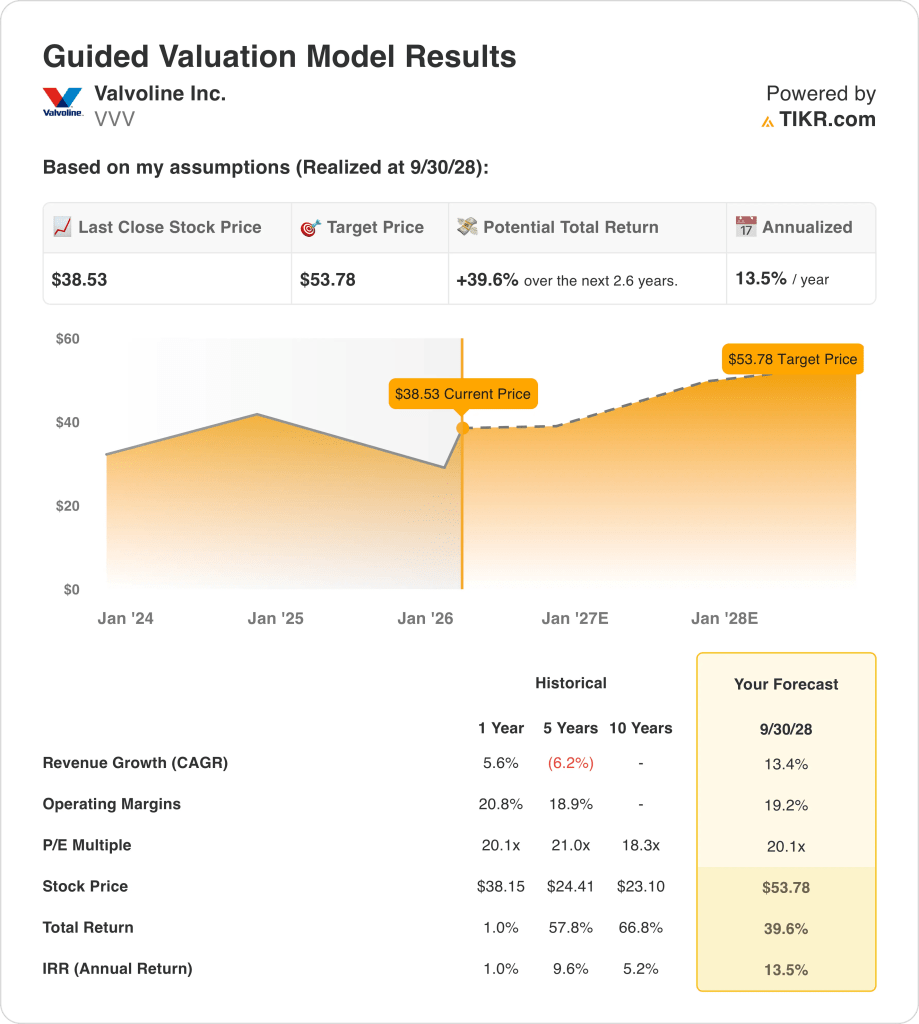

- Price Target Framework: Based on 13% revenue growth, 19% operating margins, and a 20x exit multiple, Valvoline Inc. stock could reach $54 by September 2028 from $39 today.

- Return Profile: Valvoline Inc. implies 40% total upside from $39 to $54 over 3 years, equating to a 14% annualized return under current margin expansion and network scaling assumptions.

Breaking Down the Case for Valvoline Inc.

Valvoline Inc. (VVV) operates and franchises over 2,200 quick-lube service centers across the United States and Canada, delivering preventive automotive maintenance services that include 15-minute oil changes, battery replacements, tire rotations, and manufacturer-recommended maintenance through its asset-light retail model.

Financially, the company generated $1.71 billion in revenue for fiscal 2025, reflecting 6% growth, while gross profit reached $640 million and gross margins expanded to 37%, yet operating expenses of $328 million compressed operating margins to 18% as investments in technology infrastructure and store expansion absorbed profitability gains.

The acquisition of 162 Breeze Autocare stores closed on December 1, 2025, for $593 million and added significant scale to the network, yet also introduced $33 million in incremental annual interest expense from a new $740 million Term Loan B that pushed net leverage to 3.3x adjusted EBITDA from 2.5x prior levels.

Q1 2026 results delivered $462 million in net sales and adjusted EPS of $0.37, beating consensus estimates of $0.33, as system-wide same-store sales grew 6% and adjusted EBITDA margins expanded 60 basis points to 25%, while management reaffirmed full-year fiscal 2026 guidance of $2.0 billion to $2.1 billion in revenue and $1.60 to $1.70 in adjusted EPS despite near-term margin pressure from integrating immature Breeze locations.

CEO Lori Flees stated on the Q1 earnings call, “We delivered strong Q1 results and another double-digit increase in both system-wide store sales and net sales, and we are well positioned as we continue to advance our strategic priorities and create long-term value for our shareholders.”

Meanwhile, CFO Kevin Willis projected that Breeze stores would contribute “around $160 million top line for the ten months that we will own the business in fiscal 2026” and added that the company plans to reduce leverage to 2.5x “as quickly as possible” before resuming share repurchase activity, signaling capital allocation discipline amid accelerated network expansion.

The investment tension centers on whether Valvoline’s aggressive store expansion and Breeze integration can offset near-term margin dilution of 100 basis points and elevated interest costs of $33 million annually, while maintaining sufficient earnings momentum to support a 20x forward multiple against a backdrop of $39 current stock price and 14% projected annualized returns through September 2028.

What the Model Says for VVV Stock

Valvoline Inc. stock reflects an aggressive expansion strategy through the $593 million Breeze acquisition that added 162 stores and $160 million in estimated fiscal 2026 revenue, yet near-term margin dilution of 100 basis points and elevated leverage at 3.3x EBITDA constrain profitability during the integration phase.

Therefore, the market assumption supports 13.4% revenue growth, 19.2% operating margins, and a 20.1x exit multiple, producing a $53.78 target price by September 2028, with growth assumptions sitting above the 5.6% fiscal 2025 revenue expansion yet below the 19.5% fiscal 2026 consensus projection.

This valuation delivers 39.6% total upside and a 13.5% annualized return from $38.53, representing returns that exceed a typical 10% equity hurdle rate yet embed execution risk tied to store maturation, deleveraging timelines, and sustained same-store sales momentum.

Given modeled returns of 13.5% annualized that compensate for integration complexity and leverage reduction priorities, the model signals a Buy, favoring capital appreciation over preservation as network scaling and margin recovery support earnings power through fiscal 2028.

With a 13.5% annualized return exceeding the 10% equity hurdle, the model supports capital appreciation as Breeze integration risk is offset by store network scaling and margin normalization, justifying a Buy.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Valvoline stock:

1. Revenue Growth: 13.4%

The 13.4% growth assumption sits materially above the 5-year historical CAGR of negative 6.2%, yet this comparison is distorted by the fiscal 2022 spinoff from Ashland that created a structural revenue reset, while the 1-year growth of 5.6% better reflects current baseline performance before the Breeze contribution layers on top.

Current execution supports 13.4% growth as Q1 2026 delivered 15% net sales growth on a refranchising-adjusted basis and system-wide same-store sales expansion of 5.8%, with management reaffirming fiscal 2026 revenue guidance of $2.0 billion to $2.1 billion that requires sustained ticket growth through pricing power and service premiumization.

Forward progress requires Breeze store integration to proceed without customer attrition or operational disruption, while the base network must maintain positive transaction growth despite tougher year-over-year comparisons and potential consumer spending softness in discretionary automotive services.

Sustaining 13.4% growth also depends on the company’s ability to open 330 to 360 net new stores in fiscal 2026 as guided, with franchise partners contributing their projected share and construction timelines remaining on schedule despite labor market constraints and permitting delays.

This sits above the 1-year revenue growth of 5.6%, as the Breeze acquisition provides a one-time step-change in network scale, and valuation capitalizes this elevated growth rate across multiple years without adjusting for the nonrecurring nature of the acquisition contribution.

2. Operating Margins: 19.2%

Valvoline stock reported 20.8% operating margins in fiscal 2025 on a 1-year basis and 18.9% across five years, yet these figures reflect adjusted EBITDA margins rather than pure operating margins, as the company’s retail service model carries lower fixed-cost intensity than product manufacturing but still faces labor and real estate expense pressures.

The 19.2% margin assumption sits below the 1-year level of 20.8%, as the integration of 162 immature Breeze stores creates near-term dilution estimated at 100 basis points on EBITDA margins, while Q1 2026 adjusted EBITDA margins of 25.4% demonstrated 60 basis points of year-over-year expansion through labor and product leverage.

Margin durability depends on sustained pricing discipline and service mix optimization, as ticket growth driven by premiumization of services like battery replacements and differential fluid changes carries higher incremental profitability than base oil changes, yet competitive pressure from other quick-lube operators limits pricing flexibility.

The Breeze stores currently operate at lower productivity levels than mature Valvoline locations, and management expects margin recovery as these units ramp traffic and adopt standardized operating procedures, yet this trajectory assumes successful integration execution without material customer disruption or elevated turnover in acquired store teams.

Any deviation in labor cost inflation, used oil pricing volatility, or weakness in non-oil-change revenue attachment rates would compress margins faster than the model assumes, as the company’s SG&A expenses of $328 million in fiscal 2025 still require disciplined control while supporting technology investments in CRM systems, SAP implementation, and store platform modernization.

This sits below the 1-year operating margin of 20.8%, as Breeze integration temporarily dilutes profitability and technology spending absorbs efficiency gains, and valuation assumes margins stabilize near historical averages without structural expansion despite scale benefits.

3. Exit P/E Multiple: 20.1x

Valvoline stock’s valuation history centers on multiples tied to its asset-light franchise model and recurring maintenance demand, with the 1-year NTM P/E at 20.1x as of the most recent market assumption and a 5-year average of 21.0x reflecting investor willingness to pay for predictable cash generation and network expansion optionality.

The 20.1x exit multiple capitalizes normalized earnings under the assumption that Breeze integration completes successfully, leverage reduces from 3.3x to the targeted 2.5x EBITDA, and same-store sales growth sustains at mid-single-digit levels through fiscal 2028 without recession-driven transaction declines.

This multiple assumes the market continues to value Valvoline at parity with its historical range despite elevated interest expense of $33 million annually from the new Term Loan B and the operational complexity of integrating 162 stores while simultaneously pursuing organic unit growth of 250 new stores by fiscal 2027.

The exit multiple sits in line with the Market assumption NTM P/E of 20.1x for fiscal 2026, yet this valuation does not embed further multiple expansion and therefore depends entirely on earnings growth rather than re-rating to deliver shareholder returns.

Terminal valuation depends on earnings stability and cash flow visibility, as the company suspended share repurchases to prioritize deleveraging and any disappointment in store maturation timelines, margin recovery, or competitive positioning would compress the multiple faster than earnings can recover.

This sits in line with the 1-year P/E of 20.1x and slightly below the 5-year P/E of 21.0x, as margin expansion and growth normalization already sit within projected fundamentals, and valuation assumes the market maintains its current view without re-rating risk.

What Happens If Things Go Better or Worse?

Valvoline Inc. stock results are shaped by store maturation velocity, same-store sales momentum, and margin recovery from Breeze integration through September 2030.

- Low Case: If competitive pressure limits pricing power and Breeze stores mature slower than expected, revenue grows 10% and net margins hold 11% → 5% annualized return.

- Mid Case: With sustained ticket growth and successful integration execution, revenue grows 11% and net margins reach 12% → 11% annualized return.

- High Case: If premiumization accelerates and operating leverage drives profitability gains, revenue grows 12% and net margins approach 12% → 15% annualized return.

How Much Upside Does Valvoline Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!