Key Takeaways:

- Q4 Miss and Storm Impact: Tractor Supply Company reported Q4 2025 net sales of $3.9 billion, missing $4.0 billion consensus as comparable store sales grew 0.3% versus 2.3% expected, with CEO Hal Lawton citing 100 basis points of headwind from lapping Hurricane Helene and Milton storm recovery that contributed more meaningfully to 2024 results than originally estimated.

- Fiscal 2026 Guidance Below Street: Tractor Supply Company issued fiscal 2026 net sales growth guidance of 4% to 6% below 6% consensus, and earnings per share of $2.13 to $2.23 below $2.31 Street estimate, while raising the quarterly dividend 4% to $0.96 per share and expanding the board to 10 members with Sonia Syngal’s appointment.

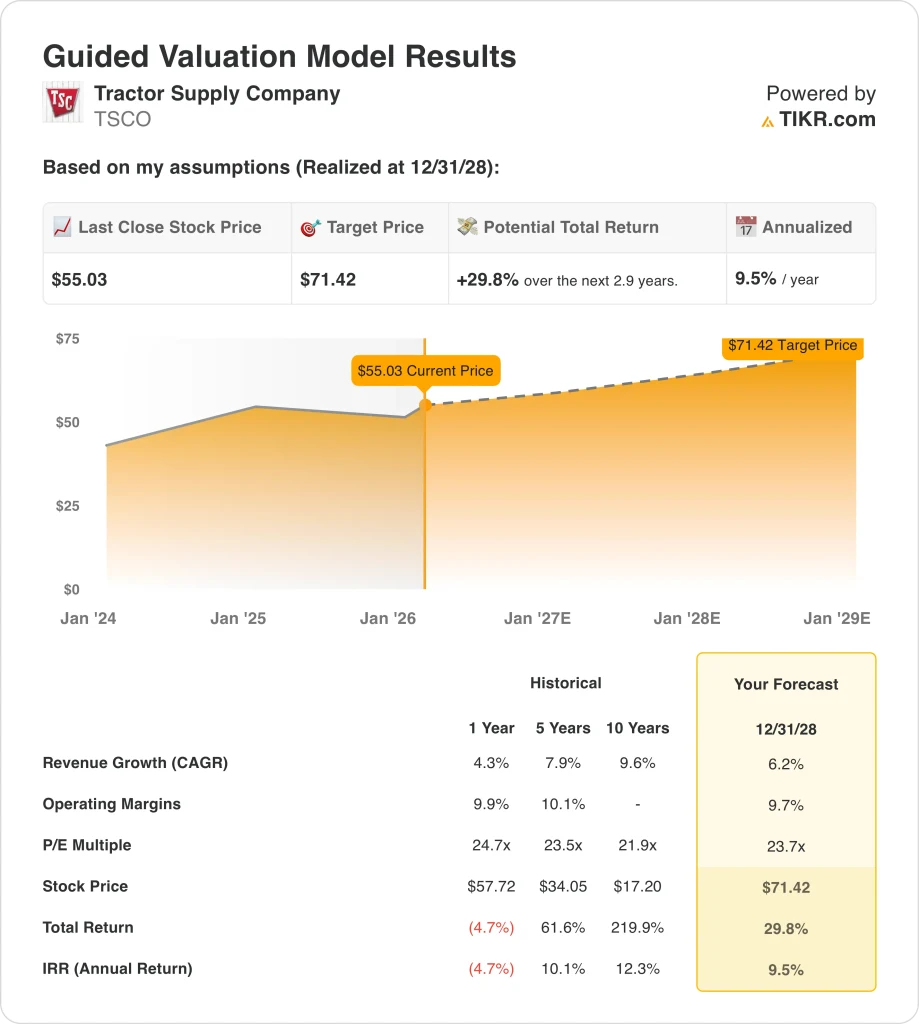

- Price Target Framework: Based on 6% revenue growth, 10% operating margins, and a 24x exit multiple, Tractor Supply Company stock could reach $71 by December 2028 from $55 today.

- Return Profile: Tractor Supply Company implies 30% total upside from $55 to $71 over 3 years, equating to a 10% annualized return under assumptions that discretionary spending stabilizes, 100 new store openings in fiscal 2026 deliver historical productivity, and Direct Sales initiative targeting $50 million in 2026 sales scales without further margin dilution.

Breaking Down the Case for Tractor Supply Company

Tractor Supply Company (TSCO) serves rural and suburban customers through over 2,200 retail locations offering equipment, livestock supplies, pet products, and home maintenance goods, positioning itself as the largest rural lifestyle retailer in a $29 billion market capitalization operating in a $225 billion total addressable market.

Financially, the company delivered $15.5 billion in fiscal 2025 revenue reflecting 4% growth, yet operating income of $1.5 billion compressed operating margins to 10% as selling, general, and administrative expenses climbed to 27% of net sales amid strategic initiative funding.

Q4 2025 results released on January of 2026, showed net sales of $3.9 billion missing $4.0 billion Street estimates, while comparable store sales rose 0.3% versus 2.3% consensus as big-ticket categories stepped down and lapping Hurricane Helene storm recovery created 100 basis point headwind.

CEO Hal Lawton stated last month on an earnings call that “fourth-quarter results came in below our expectations and reflected a shift in consumer spending with essential categories remaining resilient while discretionary demand moderated and emergency response was absent versus last year.”

Management issued fiscal 2026 guidance projecting net sales growth of 4% to 6% below 6% Street estimate and earnings per share of $2.13 to $2.23 below $2.31 consensus, while committing to open 100 new stores and increase the quarterly dividend 4% to $0.96 per share.

The company announced on February 11, 2026, a dividend increase and appointed Sonia Syngal as independent board director, while advancing Direct Sales targeting $50 million in fiscal 2026 sales with 100 specialists and Final Mile Delivery expanding to 375 hubs covering 50% of stores.

Lawton emphasized that “we remain confident in the long-term opportunity as we operate a differentiated needs-based model that has proven resilient across cycles,” while CFO Kurt Barton outlined the company’s low 2% comparable sales inflection point for operating margin expansion.

The investment tension centers on whether fiscal 2026 guidance adequately accounts for discretionary spending pressure, tariff cost limitations creating 20 to 30 basis points of ongoing pressure, and execution risk in scaling Direct Sales to $50 million while opening 100 stores without margin dilution.

What the Model Says for Tractor Supply Company Stock

Tractor Supply Company stock reflects Q4 discretionary spending pressure and 100 basis point storm recovery headwind, yet 100 new store openings in fiscal 2026 and Direct Sales scaling to $50 million support normalized growth assumptions.

The market assumption underwrites 6.2% revenue growth, 9.7% operating margins, and a 23.7x exit multiple, producing a $71.42 target price by December 2028, with growth sitting above 4.3% fiscal 2025 actual yet below 8% 5-year historical average.

This valuation delivers 29.8% total upside and a 9.5% annualized return from $55.03, representing returns that fall below a typical 10% equity hurdle rate while embedding execution risk tied to discretionary category recovery and strategic initiative scaling.

Given modeled returns of 9.5% annualized that marginally undershoot equity hurdles amid promotional environment uncertainty and tariff pressure, the model signals a Hold, favoring selective capital preservation over aggressive appreciation as normalization unfolds through fiscal 2026.

With a 9.5% annualized return falling short of the 10% equity hurdle, the model supports capital preservation as discretionary spending normalization and Direct Sales scaling remain unproven, justifying a Hold until execution de-risks the thesis.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Tractor Supply Company stock:

1. Revenue Growth: 6.2%

Tractor Supply Company stock’s revenue history shows deceleration from a 10-year CAGR of 10% to 4.3% one-year growth in fiscal 2025, as comparable store sales of 1.2% and 99 new stores provided modest expansion.

The 6.2% growth assumption sits above the 1-year growth of 4.3% yet below the 5-year CAGR of 8%, as management’s fiscal 2026 guidance of 4% to 6% net sales growth with 100 new store openings provides foundational support.

Still,current execution supports 6.2% growth as Direct Sales initiative targets $50 million in fiscal 2026 sales after achieving $2 million in December 2025 run-rate, while Final Mile Delivery expands to 375 hubs covering 50% of stores by year-end.

Meanwhile, forward progress requires discretionary spending in big-ticket categories to normalize from Q4’s high single-digit decline, spring selling season to deliver after 2 consecutive tough springs, and 100 new stores to achieve historical productivity levels.

Sustaining 6.2% growth depends on comparable store sales reaching the low 2% inflection point management cited, as transactions must remain positive despite declining consumer sentiment while average ticket growth from 2% retail inflation offsets promotional activity.

This sits above the 1-year revenue growth of 4.3%, as new store openings and Direct Sales scaling provide structural expansion, and valuation assumes fiscal 2026 guidance midpoint of 5% materializes without further discretionary category deterioration.

2. Operating Margins: 9.7%

Tractor Supply Company stock reported 9.9% operating margins in fiscal 2025 and 10.1% across five years, yet Q4 2025 operating income declined 6.5% year-over-year as SG&A expenses increased 70 basis points to 27.5% of sales.

The 9.7% margin assumption sits below the 1-year level of 9.9%, as management’s fiscal 2026 guidance of 9.3% to 9.6% maintains flat profitability despite gross margin expansion being offset by Idaho distribution center costs.

Margin durability depends on gross margin expanding through cost management and exclusive brands offsetting delivery costs and tariffs creating 20 to 30 basis points of ongoing pressure, while Direct Sales and Final Mile initiatives become self-funding.

Furthermore, CFO Kurt Barton stated on the January 29, 2026, earnings call that “our model shows an inflection point in the low 2% comp range, and as comps move above that inflection point, we would expect operating margin to improve by roughly 5 to 20 basis points per year.”

Any deviation in comparable store sales below the 2% inflection point compresses margins faster, as Q4 demonstrated with elevated promotional activity creating 10 basis points of gross margin pressure management described as transitory.

This sits below the 1-year operating margin of 9.9%, as fiscal 2026 investments in Idaho distribution center and normalized incentive compensation absorb efficiency gains without margin expansion if comparable store sales fall below the low 2% threshold.

3. Exit P/E Multiple: 23.7x

Tractor Supply Company stock’s valuation history centers on multiples tied to its needs-based retail model, with the 1-year P/E at 24.7x and a 5-year average of 23.5x.

The 23.7x exit multiple capitalizes normalized earnings under the assumption that fiscal 2026 guidance of 5% revenue growth and 9.5% operating margins materialize without further discretionary category pressure or promotional environment persistence.

This multiple assumes the market values Tractor Supply near its 5-year average of 23.5x despite operating margins remaining flat at 9.5% rather than expanding toward the 10.1% 5-year historical average.

The exit multiple sits slightly below the Market assumption NTM P/E of 24.7x for fiscal 2026, yet this valuation depends entirely on earnings growth from revenue scaling and margin inflection above the low 2% comparable store sales threshold.

Terminal valuation depends on earnings stability, as any disappointment in new store productivity, Direct Sales customer acquisition economics, or spring selling season execution would compress the multiple faster than earnings can recover.

This sits in line with the 5-year P/E of 23.5x and below the 1-year P/E of 24.7x, as margin expansion and comparable store sales normalization already sit within projected fundamentals without re-rating upside.

What Happens If Things Go Better or Worse?

Tractor Supply Company stock results are shaped by comparable store sales momentum, discretionary category recovery, and new store productivity as Direct Sales and Final Mile initiatives scale through December 2030.

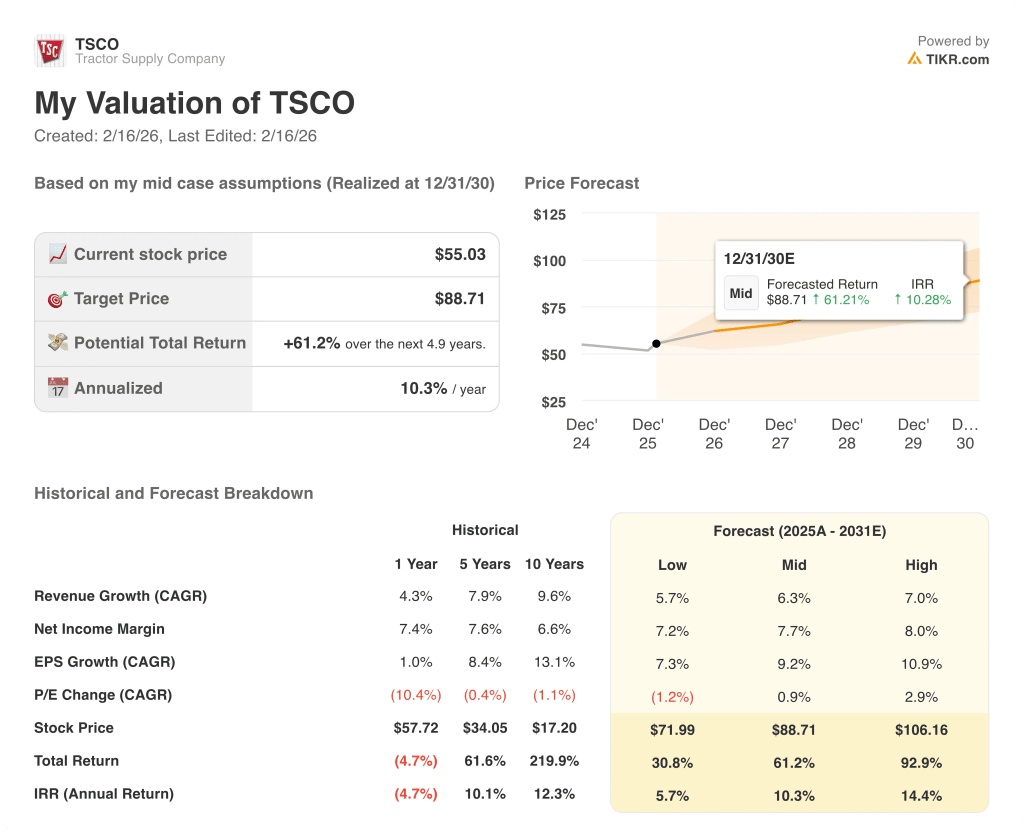

- Low Case: If promotional pressure persists and big-ticket categories remain soft, revenue grows 6% and net margins hold 7% → 6% annualized return.

- Mid Case: With discretionary spending normalizing and Direct Sales reaching $50 million in fiscal 2026, revenue grows 6% and net margins reach 8% → 10% annualized return.

- High Case: If spring selling season delivers after 2 tough years and new stores achieve historical productivity, revenue grows 7% and net margins approach 8% → 14% annualized return.

How Much Upside Does Tractor Supply Company Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!