Key Takeaways:

- Q4 2025 Beat: General Electric Company delivered Q4 2025 revenue of $11 billion up 20% and EPS of $1.57 beating the $1.43 estimate, as commercial services revenue surged 31% and LEAP engine deliveries increased 49% while free cash flow grew 15% to $1.8 billion with conversion over 100%.

- Fiscal 2026 Guidance: General Electric Company issued fiscal 2026 guidance last January targeting $48 billion revenue up 14% at the midpoint, operating profit of $9.85 billion to $10.25 billion representing $1 billion growth, EPS of $7.10 to $7.40 up 15%, and free cash flow of $8 billion to $8.4 billion with conversion solidly above 100%.

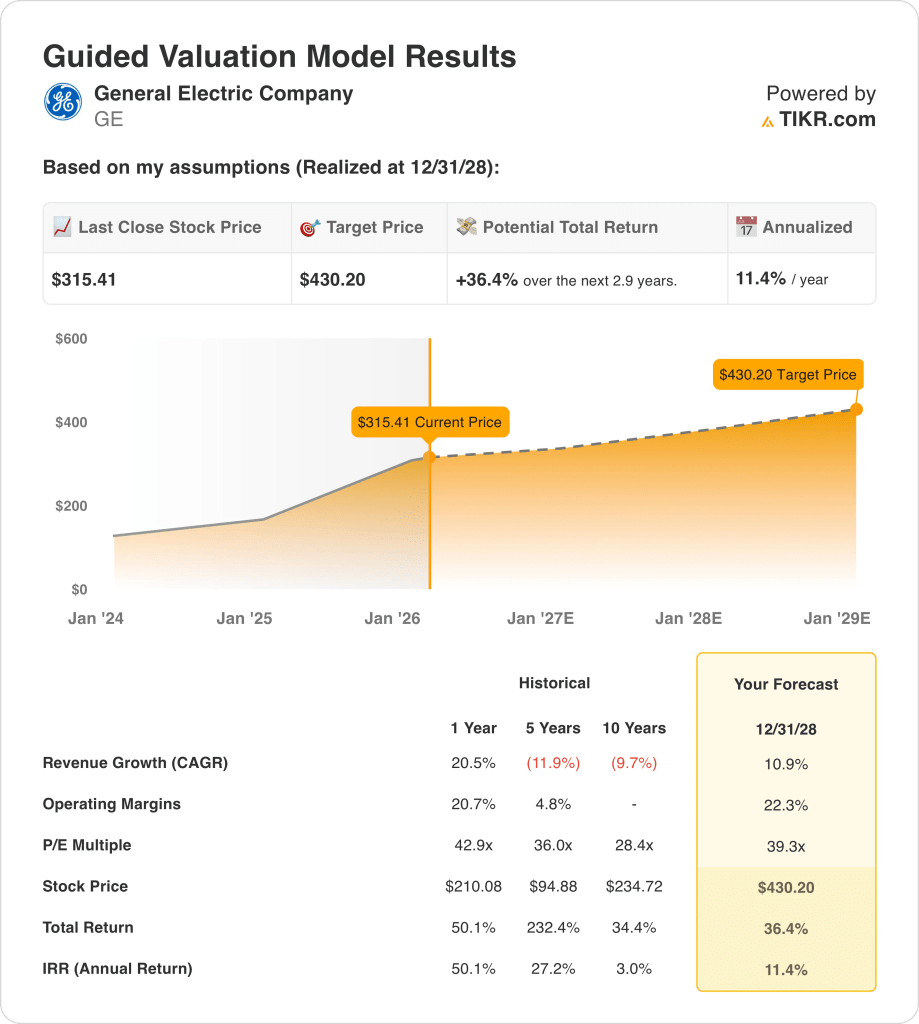

- Price Target Path: Based on 11% revenue growth, 22% operating margins, and a 39x exit multiple, General Electric Company stock could reach $430 by December 2028 from $315 today.

- Return Profile: General Electric Company implies 36% total upside from $315 to $430 over 3 years, equating to an 11% annualized return under assumptions that commercial services revenue grows mid-teens and LEAP internal shop visits increase 25% in fiscal 2026.

Breaking Down the Case for GE Electric Co.

General Electric Company (GE) powers commercial aviation through its installed base of 80,000 engines globally, split between the Commercial Engines and Services segment delivering $34 billion in fiscal 2025 revenue and the Defense Propulsion and Technologies segment generating $10 billion, positioning the company as the world’s largest aerospace engine manufacturer with a $190 billion backlog.

Financially, the company delivered $42.3 billion in fiscal 2025 revenue reflecting 21% growth, yet operating income of $9.5 billion compressed operating margins to 21% from 20% the prior year as commercial services volume and price gains of $1.8 billion were partially offset by original equipment growth, GE9X ramp losses of $200 million, and $3 billion in annual R&D investments while LEAP engine deliveries exceeded 1,800 units up 28%.

Last January, the company reported Q4 2025 results with orders up 74%, revenue up 20% to $11 billion, operating profit up 14% to $2.3 billion, and EPS of $1.57 beating the $1.43 estimate as commercial services revenue surged 31%, internal shop visit revenue grew 30%, spare parts sales increased 25%, and free cash flow reached $1.8 billion up 15% with conversion over 100%.

Management issued fiscal 2026 guidance targeting low double-digit revenue growth with commercial services up mid-teens, operating profit of $9.85 billion to $10.25 billion up $1 billion at the midpoint, EPS of $7.10 to $7.40 up 15%, and free cash flow of $8 billion to $8.4 billion as LEAP internal shop visits grow 25% and deliveries increase 15%.

CEO Larry Culp stated on the January 22, 2026, earnings call that “we expect to deliver mid-teens revenue growth between ’24 and ’26 compounded and $10 billion of profit in ’26 2 years earlier than our outlook at spin,” framing acceleration momentum through Flight Deck continuous improvement initiatives and supply chain partnerships delivering 40% year-over-year material input growth.

The company announced last February that United Airlines selected 300 GEnx engines to power new Boeing 787 Dreamliners making United the largest GEnx operator globally, while Delta selected GE Electric last January to power 30 Boeing 787-10s with deliveries starting in 2031, and Pegasus Airlines committed last December to up to 300 LEAP-1B engines for future Boeing 737-10 fleets.

Meanwhile. last February, GE Electric unveiled a $300 million Singapore automation lab investment targeting 33% repair volume growth without expanding site footprint as the company deploys robotics to automate compressor blade blending and reduce CFM56 turbine nozzle turnaround times from 40 days in 2021 to a 21-day 2028 target through Flight Deck lean manufacturing principles.

The investment tension centers on whether fiscal 2026 guidance adequately accounts for GE9X losses doubling year-over-year as shipments increase, spare engine ratio declining as planned creating equipment mix headwinds, and supply chain capacity constraints limiting commercial services growth despite mid-teens revenue targets and $190 billion backlog support.

This unfolds against a backdrop of $315 current stock price, 43x forward P/E above the 36x 5-year historical average, and 11% projected annualized returns through December 2028 that depend on LEAP shop visit output growing 25% in fiscal 2026, CFM56 retirements moderating to 2% versus prior 2% to 3% expectations, and operating margins expanding to 22% as commercial services volume scales without further GE9X or original equipment dilution.

What the Model Says for GE Stock

GE Electric enters 2026 with strong engine demand, rising service volumes, and expanding repair capacity, supporting elevated expectations despite ongoing 9X investment pressure.

The model uses a 10.9% revenue growth market assumption, 22.3% margin market assumption, and 39.3x exit multiple market assumption to reach a $430.20 target price.

This produces 36.4% total upside and an 11.4% annualized return, modestly above a typical 10% equity hurdle rate.

The model signals a Buy because the 11.4% annualized return exceeds required returns while supported by improving profitability and durable service demand.

The 11.4% annualized return exceeds a 10% equity hurdle rate, indicating the projected 36.4% upside supports capital appreciation rather than mere capital preservation, and justifies a Buy based strictly on valuation math.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for GE Electric stock:

1. Revenue Growth: 10.9%

The 10.9% revenue growth model assumption sits below the recent 20.5% one-year growth, while management guides low double-digit expansion supported by a $190 billion backlog and rising LEAP shop visits.

Last January, orders rose 32% and revenue increased 21%, supported by 80,000 engines in service and mid-teens services guidance for 2026, which anchors recurring revenue more than original equipment deliveries.

However, revenue depends on supply chain stability, spare parts availability, and execution on 15% LEAP delivery growth, while 9X ramp losses and slower aircraft production could pressure near-term growth rates.

If revenue slows toward mid-single digits while margins target 22.3%, fixed-cost leverage weakens and the 39.3x multiple becomes sensitive, as growth and profitability assumptions compound valuation risk.

This is below the 1-year revenue growth of 20.5%, as backlog conversion normalizes after post-pandemic demand, and valuation relies on sustained services expansion rather than peak recovery growth.

2. Operating Margins: 22.3%

GE electric stock’s 22.3% operating margins exceeds the 1-year margin of 20.7%, while management guides operating profit of roughly $10 billion with services growth carrying higher profitability than equipment.

Last January, margins reached 21.4% for the year, supported by 26% services revenue growth and improved shop turnaround times, while 9X losses of roughly $200 million weighed on equipment profitability.

Margin expansion requires stable pricing, spare parts availability, and higher LEAP aftermarket contribution, as doubling 9X losses in 2026 and increased R&D spending pressure equipment mix.

If revenue underperforms while margins aim for 22.3%, operating leverage fades and earnings compress quickly, as fixed manufacturing costs remain high and capital intensity limits flexibility.

This is above the 1-year operating margin of 20.7%, as services mix expansion lifts profitability, and sustaining higher margins requires disciplined cost execution and steady aftermarket demand.

3. Exit P/E Multiple: 39.3x

Using the model’s 39.3x exit multiple values expected earnings after scale gains and margin expansion, treating 2028 profits as durable rather than a temporary cyclical high.

The market assumption NTM P/E for 2026 stands at 42.9x, so the 39.3x exit multiple assumes modest contraction while preserving premium valuation tied to recurring services cash flow.

This multiple embeds confidence that LEAP profitability improves, 9X losses normalize, and free cash flow remains above 100% conversion, while backlog visibility supports earnings durability.

If margins stall below 22.3% or revenue growth slips under 10.9%, earnings estimates fall and the multiple contracts sharply, as industrial stocks historically compress when execution disappoints.

This is in line with the 1-year historical P/E of 42.9x, as elevated demand and services visibility sustain premium valuation, and downside risk rises if earnings momentum slows.

What Happens If Things Go Better or Worse?

GE Electric stock results are shaped by engine demand, aftermarket execution, and supply chain stability through 2030.

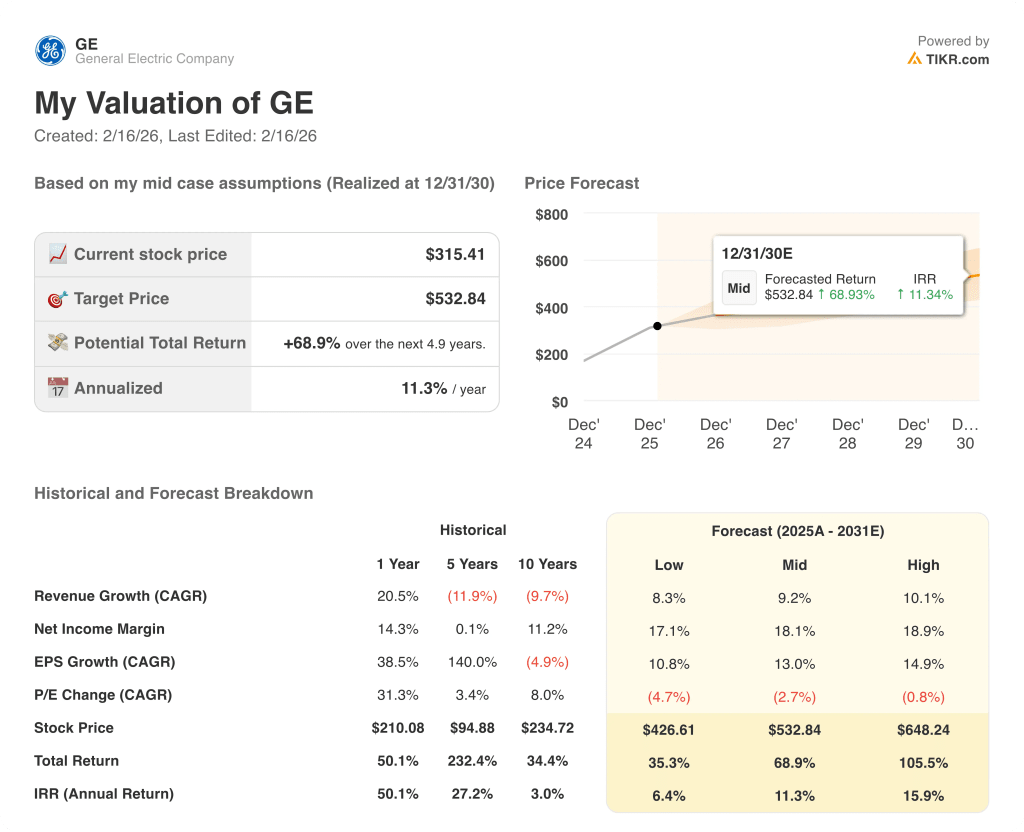

- Low Case: If supply tightness and equipment mix pressure persist, revenue grows 8.3% with 17.1% net margins, easing valuation → 6.4% annualized return.

- Mid Case: With backlog converting steadily and services expanding as planned, revenue grows 9.2% and margins reach 18.1% → 11.3% annualized return.

- High Case: If LEAP profitability improves and repair throughput rises, revenue grows 10.1% with 18.9% margins → 15.9% annualized return.

How Much Upside Does GE Electric Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!