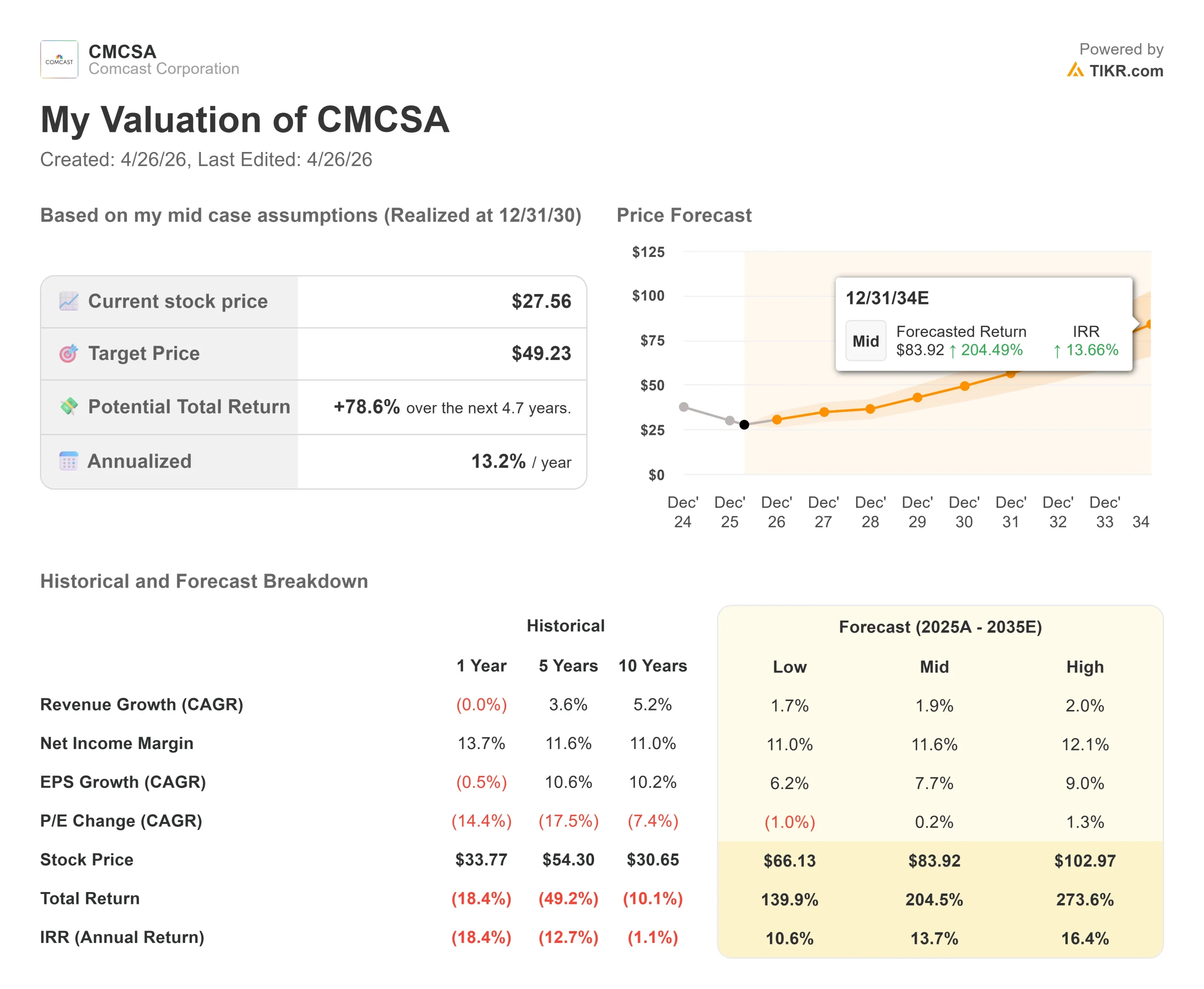

Key Stats for Comcast Stock

- Current Price: $27.56

- Street Mean Target: ~$33

- TIKR Mid-Case Target: ~$49

- Potential Total Return: ~79%

- Annualized IRR: ~13% / year

- Q1 2026 Earnings Reaction: (12.90%) on April 24, 2026

- Dividend Yield: 4.9%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Comcast (CMCSA) fell 12.90% on April 24, 2026, the session after reporting Q1 results, dropping from $31.64 to $27.56. That put the stock within reach of its 52-week low of $25.75. The unusual part: it was a beat on every major metric.

Revenue came in at $31.46 billion, up 10.9% year over year on a pro forma basis and 3.4% ahead of consensus. Adjusted EPS of $0.79 beat estimates by 8.3%. Adjusted EBITDA of $7.93 billion beat by 2.4%. Net income attributable to Comcast fell 35.6% to $2.17 billion, and adjusted EBITDA declined 16.8%. Free cash flow dropped 28% to $3.9 billion. Deutsche Bank downgraded the stock to Hold from Buy, citing a muted EBITDA and free cash flow outlook beyond 2026.

The EBITDA and cash flow pressure were not a surprise to anyone on the call. CFO Jason Armstrong framed it clearly: “This is an investment period for us.”

Two temporary, deliberate costs drove the decline: the first-year peak of the new NBA rights contract, with roughly half of all NBA games played in Q1 representing the heaviest quarterly cost, and the upfront investment behind Comcast’s broadband go-to-market pivot. Armstrong stated both pressures would begin easing from Q2 onward.

Co-CEO Michael Cavanagh addressed the stock reaction directly during Q&A. On Comcast’s positioning and the negativity around cable, he said: “I think we’re undervalued, frankly, and the negativity on the business is something we need to work on changing people’s sentiment towards, period, full stop.”

That is an on-record conviction statement from the executive running day-to-day operations, made while the stock was falling by double digits.

See historical and forward estimates for Comcast stock (It’s free!) >>>

Is Comcast Undervalued Today?

At $27.56, CMCSA trades at 7.68x forward earnings and 5.47x forward EV/EBITDA, per TIKR. The Street’s mean target is $32.73, implying roughly 19% upside.

Peers trade at a notable premium.

Verizon sits at 9.44x forward earnings and 6.81x forward EV/EBITDA. AT&T trades at 11.11x forward earnings and 7.12x forward EV/EBITDA. Comcast trades below both on both metrics, despite owning Universal Parks, NBCUniversal, Peacock, and a growing wireless business that neither peer has. The valuation discount is real. The debate is whether it is deserved.

The bear case is straightforward. Comcast lost 65,000 domestic residential broadband customers in Q1, an improvement from 183,000 losses a year ago, but still a net loss. Broadband ARPU fell 3.1%, and Armstrong guided for more pressure in Q2.

The free cash flow trajectory tells the same story: TIKR consensus estimates show FCF declining from $19.2 billion in 2025 to $13.3 billion in 2026 as NBA costs and broadband investments peak simultaneously.

The bull case sits in the parts of the business the market is discounting. Universal theme parks revenue rose 24% to $2.33 billion in Q1, while film studio revenue rose 21% to $3.43 billion. Theme Parks EBITDA increased 33% to $551 million, fueled by Epic Universe. Peacock crossed $2 billion in quarterly revenue for the first time and reached 46 million paid subscribers. Armstrong said Peacock is “on track to approach profitability for the first time next quarter,” with durable profitability the stated goal as NBA amortization normalizes.

On wireless, Comcast added a record 435,000 net lines in Q1, bringing total Xfinity Mobile lines to 9.7 million at 16% penetration of its domestic residential broadband base. Steve Croney, President of Connectivity and Platforms, disclosed on the call that the company is running hundreds of AI-driven models with thousands of attributes to optimize acquisition, upsell, and retention decisions. Connect volumes are positive for the first time in more than four years.

The number that got the least attention post-earnings was Armstrong’s convergence ARPA disclosure: Comcast’s combined broadband and wireless service revenue per account currently sits at roughly $85, while telecom competitors are at roughly double that figure on the same metric. Every free wireless line that converts to a paying relationship in the second half of 2026 moves that number higher. Management said early cohort retention has been strong, with a “significant majority” of rolled-off free lines converting to paid.

See how Comcast performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $27.56

- TIKR Mid-Case Target: ~$49

- Potential Total Return: ~79%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Comcast stock (It’s free!) >>>

The TIKR mid-case model targets around $49 per share over the next approximately 4.7 years, implying roughly 79% total return and around 13% annualized IRR. The model assumes around 2% annual revenue CAGR and a net income profit margin of around 12%. Both are conservative relative to Comcast’s 10-year historical revenue CAGR of 5.2% and its current LTM net income margin of 13.7%.

The two revenue drivers are wireless monetization as free-line conversions compound through 2026 and beyond, and broadband ARPU recovery as the go-to-market transition laps its initial investment period. The margin driver is operating leverage in wireless: paid lines grow on a capital-efficient MVNO model without proportional cost increases.

The primary risk is the sustainability of the broadband trend. Armstrong confirmed on the call that over half of Q1’s broadband improvement came specifically from Legendary February promotions, a one-time marketing moment tied to the Olympics and Super Bowl, rather than purely organic improvement. If that demand was pulled forward, Q2 losses could disappoint. A secondary risk is international parks, where Cavanagh noted it remains too soon to know whether higher oil prices and airline costs could create pressure on Parks in Q2 and Q3.

At 7.68x forward earnings with a 4.9% dividend yield, the stock is priced for continued failure. The TIKR model suggests the market has overcorrected.

Conclusion

Watch broadband net losses at Q2 2026 earnings, expected in late July. A second consecutive quarter of year-over-year improvement, even a modest one, would confirm that the organic recovery is real and not a Legendary February artifact. One quarter of improvement is a data point. Two is a trend.

Comcast is trading at distressed cable multiples while running a record wireless quarter, a profitable Q2 streaming service, and the best-performing theme park resort it has ever had. The market is pricing the risk. The TIKR model suggests it is not pricing the recovery.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Comcast?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Comcast, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Comcast alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Comcast on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!