Key Stats for Cummins Stock

- 52-Week Range: $284 to $663

- Current Price: $661

- Street Mean Target: $643

- Street High Target: $784

- Analyst Consensus: 9 Buys / 4 Outperforms / 9 Holds / 1 Underperform

- TIKR Model Target (Dec. 2030): $726

What Happened?

Cummins Inc. (CMI) is one of the world’s largest manufacturers of diesel and natural gas engines, power generation equipment, and drivetrain components, serving commercial truck, construction, mining, and data center markets across more than 100 countries.

The company closed 2025 with $33.67 billion in full-year revenue, down 1% from the prior year as weakness in North America’s heavy and medium-duty truck markets outweighed record performance in Power Systems and Distribution.

The headline number undersells the real story.

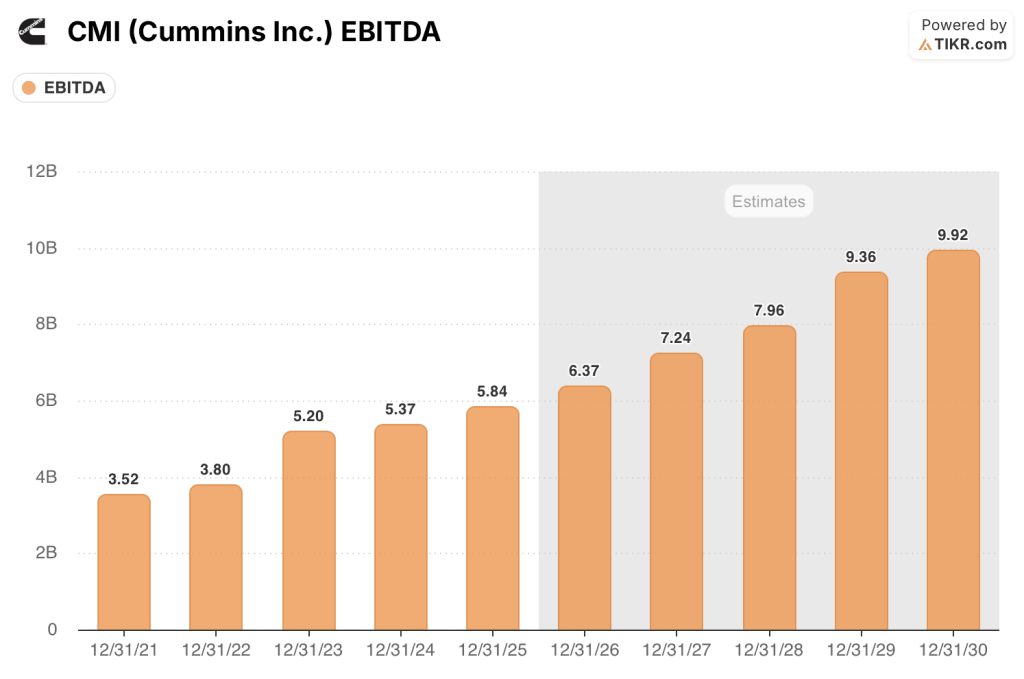

Excluding one-time Accelera electrolyzer charges of $458 million, Cummins posted record adjusted EBITDA of $5.84 billion, or 17.4% of sales, up from $5.4 billion and 15.7% in 2024 and ahead of the company’s own 2030 margin targets, achieved four years early.

Power Systems, the segment supplying backup diesel generators to data centers, delivered full-year revenue of $7.5 billion, up 16% year-over-year, with EBITDA margins of 22.7%, up 430 basis points from 2024.

Distribution, the global service and support network that routes Power Systems product to hyperscaler customers, hit record revenue of $12.4 billion, up 9%, with EBITDA of 14.6%, up 250 basis points.

The data center angle is not a passing trend for Cummins.

CEO Jennifer Rumsey said on the Q4 2025 earnings call: “We’re taking orders now well into 2028; the demand remains very strong for diesel backup power.”

Total data center-related revenue reached approximately $3.5 billion in 2025, up from $2.6 billion in 2024, and company strategy head Jeff Wiltrout confirmed at the February Citi conference that backlog now extends into 2028 with active conversations for 2029 and beyond.

Cummins doubled its 95-liter engine manufacturing capacity ahead of schedule in 2025, completed the Centum generator set product line with the S17 targeting space-constrained mission-critical sites, and positioned itself as a vertically integrated supplier across engines, alternators, and radiators for data center gensets.

The truck cycle, which weighed on 2025 results, is beginning to turn.

North American Class 8 truck production is guided to 220,000 to 240,000 units in 2026, flat to up 10% from 2025’s trough, with a pronounced second-half recovery expected as a prebuy cycle ahead of EPA’s January 2027 low-NOx standard begins to build.

Cummins is launching three new engine platforms under the HELM architecture for the 2027 emissions cycle, with the X10 replacing both the L9 and X12 platforms alongside an updated B Series and a next-generation X15, and content-per-truck increases of roughly $10,000 are expected to drive average selling price uplift across the Engine and Components segments.

In April 2026, Alstom acquired Cummins’ hydrogen fuel cell activities dedicated to rail, a signal of continued portfolio rationalization in Accelera as management refocuses investment away from green hydrogen and toward battery electric applications.

For 2026, Cummins guided full-year revenue growth of 3% to 8% and EBITDA margins of 17% to 18%, absorbing an estimated 50 basis points of dilution from tariff surcharges the company expects to largely recover at the dollar level through pricing adjustments.

Wall Street’s Take on CMI Stock

The record Power Systems and Distribution margins Cummins posted in 2025 are not a one-cycle event but the first evidence that the company’s structural earnings power has permanently shifted upward.

CMI’s adjusted EBITDA reached $5.84 billion in 2025, up around 9% year-over-year, with consensus projecting around $6.37 billion in 2026 (+9%) and around $7.24 billion in 2027 (+14%), as Power Systems capacity expansion and truck cycle recovery compound through the earnings base simultaneously.

Of 23 analysts covering Cummins stock, 13 carry buy or outperform ratings against 9 holds and 1 underperform, with a mean price target of $643.36 — roughly 3% below the current price of $660.75 — signaling the Street views CMI as fairly priced after its near-doubling over the prior year.

The spread between the $490 low target and the $784 high target reflects a genuine debate: bulls at the upper end are pricing in an accelerated data center capacity expansion and a stronger-than-guided EPA27 prebuy, while bears near the floor see the valuation as having already discounted both tailwinds.

Trading at approximately 18x 2026 consensus EBITDA against a 5-year historical average closer to 13x to 14x, Cummins stock appears fairly valued relative to its own history, as earnings growth of around 9% annually through 2028 is already embedded in the current price.

The Analyst Day on May 21 in New York is the next significant repricing event, with management expected to update 2030 financial targets that the company has already cleared four years ahead of schedule, alongside capital allocation guidance that may include share repurchase commitments.

Tariff-driven margin dilution of 50 basis points in 2026, combined with first-year launch costs on three HELM engine platforms in early 2027, presents a near-term compression window that could temporarily interrupt the margin expansion narrative for 12 to 18 months.

The Analyst Day EBITDA target revision and the magnitude of EPA27 content-add realized in Engine and Components pricing will confirm or deflate the current multiple.

What Does the Valuation Model Say?

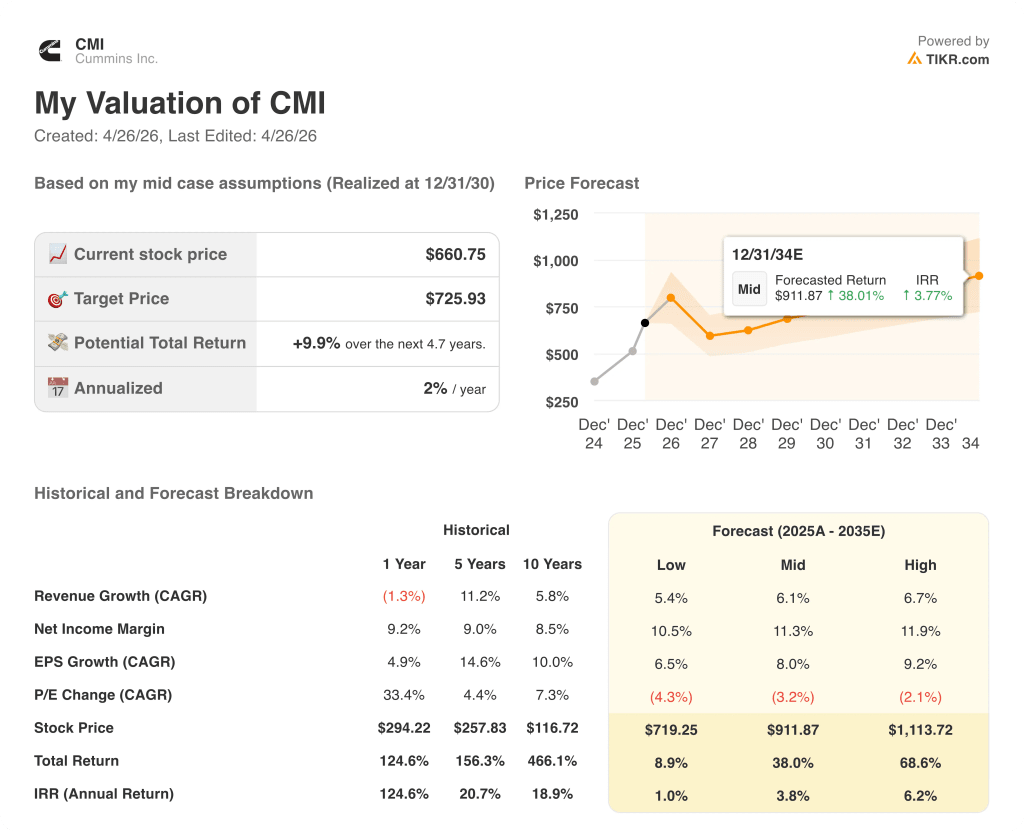

TIKR’s model assigns Cummins stock a mid-case target of approximately $726, implying a 10% total return over 5 years at an annualized rate of around 2%, built on revenue CAGR assumptions of around 6% through 2030 and net income margins expanding from 10% in 2025 to around 11% by 2030, consistent with the Power Systems margin expansion already underway.

At roughly $661, with the mid-case target implying only single-digit total upside and the current forward multiple already pricing in a strong EBITDA recovery, Cummins stock appears fairly valued — the structural data center story is real, but the market has already paid for it.

Cummins is a business with two distinct multi-year growth drivers arriving simultaneously, but the stock’s near-doubling over the prior twelve months means investors are now paying for the story before it fully delivers.

The central tension: can the EPA27 content uplift and data center capacity expansion drive EBITDA growth above the around 9% consensus pace that current prices already reflect?

What Has to Go Right

- Power Systems revenue grows 12% to 17% in 2026 as guided, with margins holding in the 23% to 24% range as additional capacity investments prove efficient

- EPA27 average selling price uplift of roughly $10,000 per truck lands by early 2027, with Engine and Components capturing around two-thirds of that content increase at neutral-to-accretive margins over the product life cycle

- North America heavy-duty truck production returns to 250,000-plus units by 2027 as the cyclical recovery and prebuy combine, restoring Engine segment EBITDA to the 12% to 13% guided range and layering additional earnings on top of Power Systems growth

- The May 21 Analyst Day produces materially higher 2030 financial targets, triggering upward estimate revisions and a re-rating toward the $784 high target

What Could Go Wrong

- The current mean analyst target of $643 is already 3% below the stock price; any guidance miss at the Analyst Day — particularly on data center capacity commitments or 2030 EBITDA targets — could trigger meaningful multiple compression

- Tariff surcharges diluting 50 basis points of EBITDA margin in 2026 compound with HELM platform launch costs in early 2027, creating a compression period that interrupts the margin expansion story for up to 18 months

- Accelera losses of $325 million to $355 million projected for 2026 remain a persistent drag, and any policy reversal forcing incremental zero-emissions investment could widen losses beyond the guided range

- The data center backlog extends into 2028 without capital commitments from hyperscalers; a deceleration in AI infrastructure spending would reduce Power Systems order intake with no near-term offset from the still-recovering truck market

Should You Invest in Cummins Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CMI stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cummins Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CMI stock on TIKR for Free →