Key Stats

- Current price: ~$92

- Q1 2026 revenue: $12.25B, up 16.2% YoY

- Q1 2026 operating income: $3.96B, up 18.2% YoY

- Q1 2026 operating margin: 32.3%, up from 31.7% in Q1 2025

- Q1 2026 free cash flow: $5.09B, up 91.4% YoY

- Member quality metric: all-time high in Q1 (second consecutive record)

- 2026 full-year revenue growth guidance: 12–14% (maintained)

- 2026 full-year operating margin guidance: 31.5% (maintained)

- 2026 advertising revenue target: ~$3B

- TIKR model price target: ~$189 (mid case, realized 12/31/30)

- Implied upside over ~5 years: ~+104%

Netflix Q1 2026 Earnings Breakdown

Netflix stock (NFLX) posted $12.25B in Q1 2026 revenue, a 16.2% YoY increase, while operating income grew 18.2% to $3.96B against guidance calling for a 31.5% full-year operating margin.

Management maintained its full-year 2026 guidance in full: 12% to 14% revenue growth and a 31.5% operating margin, absorbing roughly $275M in M&A-related costs from both the InterPositive acquisition and the terminated Warner Bros. deal with no material impact to the margin outlook, according to CFO Spence Neumann on the Q1 earnings call.

Netflix stock’s member quality metric hit an all-time high in Q1 2026, the second consecutive record after Q4 2025, with retention improving year over year across every region.

View hours grew at a rate consistent with the second half of 2025 despite 17 days of Winter Olympics streaming competition landing in the quarter.

The World Baseball Classic was the single biggest driver of regional outperformance: 31.4 million viewers made it the most-watched program in Netflix’s history in Japan, it produced the largest single sign-up day ever in Japan, and Japan delivered the company’s highest quarterly paid net adds in company history, according to Co-CEO Ted Sarandos on the Q1 earnings call.

APAC was the strongest FX-neutral revenue growth region in Q1, with contributions from Japan, India, Korea, and Southeast Asia extending well beyond the WBC.

On advertising, Netflix stock’s advertiser base grew over 70% year over year in 2025 to more than 4,000 advertisers, with programmatic on pace to represent more than 50% of non-live ad sales; management reiterated its target to roughly double advertising revenue to approximately $3B in 2026, according to Co-CEO Greg Peters on the Q1 earnings call.

Netflix walked away from the Warner Bros. acquisition after deal costs exceeded net value to shareholders, with Co-CEO Ted Sarandos describing the exit as a test of investment discipline and confirming no change to the company’s capital allocation philosophy.

Reed Hastings, Netflix’s founder and Board Chair, announced he will not stand for reelection at the upcoming shareholder meeting, with both Co-CEOs confirming the decision was unrelated to the Warner Bros. transaction.

Netflix Stock Financials

Netflix’s Q1 2026 income statement shows a business operating at the intersection of sustained revenue growth and margin expansion, with both gross profit and operating leverage reaching multi-quarter highs in the same period.

Gross margin reached 52% in Q1 2026, matching the Q1 2025 level of 50.1% on an upward basis and representing the highest gross margin in the eight quarters visible in the income statement, up from 45.9% in Q2 2024.

Gross profit grew to $6.36B in Q1 2026, up 20.5% YoY from $5.28B in Q1 2025, continuing a run of consistent double-digit gross profit growth across the trailing eight quarters.

Operating income reached $3.96B in Q1 2026, up 18.2% YoY from $3.35B in Q1 2025, with operating margin expanding from 31.7% to 32.3%.

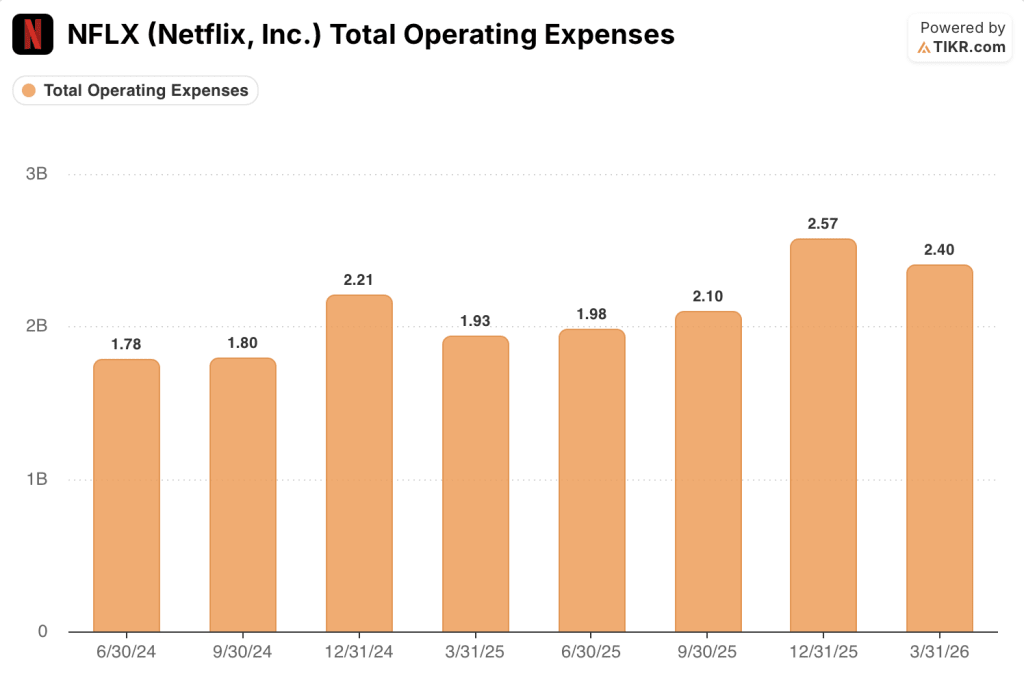

Total operating expenses fell to $2.40B in Q1 2026 from $2.57B in Q4 2025, reflecting the absence of elevated M&A-related costs that pressured the prior quarter and providing the primary mechanism for the sequential margin recovery.

The operating margin trajectory across the trailing eight quarters shows meaningful variability: operating margin troughed at 22.2% in Q4 2024 before recovering to 31.7% in Q1 2025, dipping again to 24.5% in Q4 2025, and rebounding sharply to 32.3% in Q1 2026, a pattern consistent with first-quarter seasonality in content spend.

What Does the Valuation Model Say?

The TIKR valuation model prices Netflix stock at a mid-case target of approximately $189, implying roughly 104% upside from the April 24 close of ~$92, at an annualized return of about 16% over 4.7 years.

The mid-case assumptions call for a 9.6% revenue CAGR and a 33.2% net income margin, both grounded in the trajectory Netflix has already demonstrated: Q1 2026 operating margin of 32.3% is within reach of the 33.2% net income margin the model requires.

Q1’s combination of maintained full-year guidance, all-time member quality, broad-based regional growth, and free cash flow of $5.09B (up 91.4% YoY) collectively tighten the range of outcomes and strengthen the investment case for Netflix stock at current levels.

The central argument is not whether Netflix can sustain growth, it is whether the current price gives investors sufficient compensation for a business growing revenue at 16% with expanding margins and record engagement.

The central tension for Netflix stock is whether a maturing paid member base forces the company to rely on advertising and live content to sustain the 12% to 14% revenue growth rate that justifies the current valuation.

What Has to Go Right

- Advertising revenue doubles to approximately $3B in 2026 on schedule, with programmatic exceeding 50% of non-live ad sales and the advertiser base continuing to expand beyond the 4,000-plus advertisers reached in 2025

- Live content strategy delivers outsized business impact at scale: the World Baseball Classic drove 31.4 million viewers, Japan’s largest sign-up day ever, and record quarterly net adds in one country; replication across CONCACAF, Women’s World Cup, and NFL expansion events drives similar regional growth flywheel effects

- Member quality metric sustains consecutive all-time highs into Q2, supporting the pricing power that allows management to raise U.S. subscription prices while retention improves across every region

- InterPositive acquisition accelerates GenAI production capabilities, reducing per-title content costs and improving the return on Netflix’s content investment at scale

What Could Still Go Wrong

Reed Hastings’ departure from the Board removes the founder’s institutional oversight at a moment when the company is navigating its most significant strategic pivots, including live sports, gaming, podcasting, and GenAI production tools simultaneously

Paid member growth is not disclosed on a quarterly basis; the business is approaching 45% penetration of the addressable smart TV household universe, and the next leg of growth depends on advertising and gaming audience expansion that remains early-stage

The operating margin trajectory shows significant quarterly volatility: operating margin swung from 34.1% in Q2 2025 to 24.5% in Q4 2025 before recovering to 32.3% in Q1 2026, and sustained elevated content spend on live rights could reproduce that compression in H2 2026

The mid-case TIKR model requires net income margins of 33.2%, above the 22.3% net income margin Netflix delivered in the trailing twelve months; the gap depends heavily on advertising scaling at the pace management has guided

Should You Invest in Netflix, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NFLX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Netflix, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NFLX stock on TIKR for Free →