Key Stats for GE Healthcare Stock

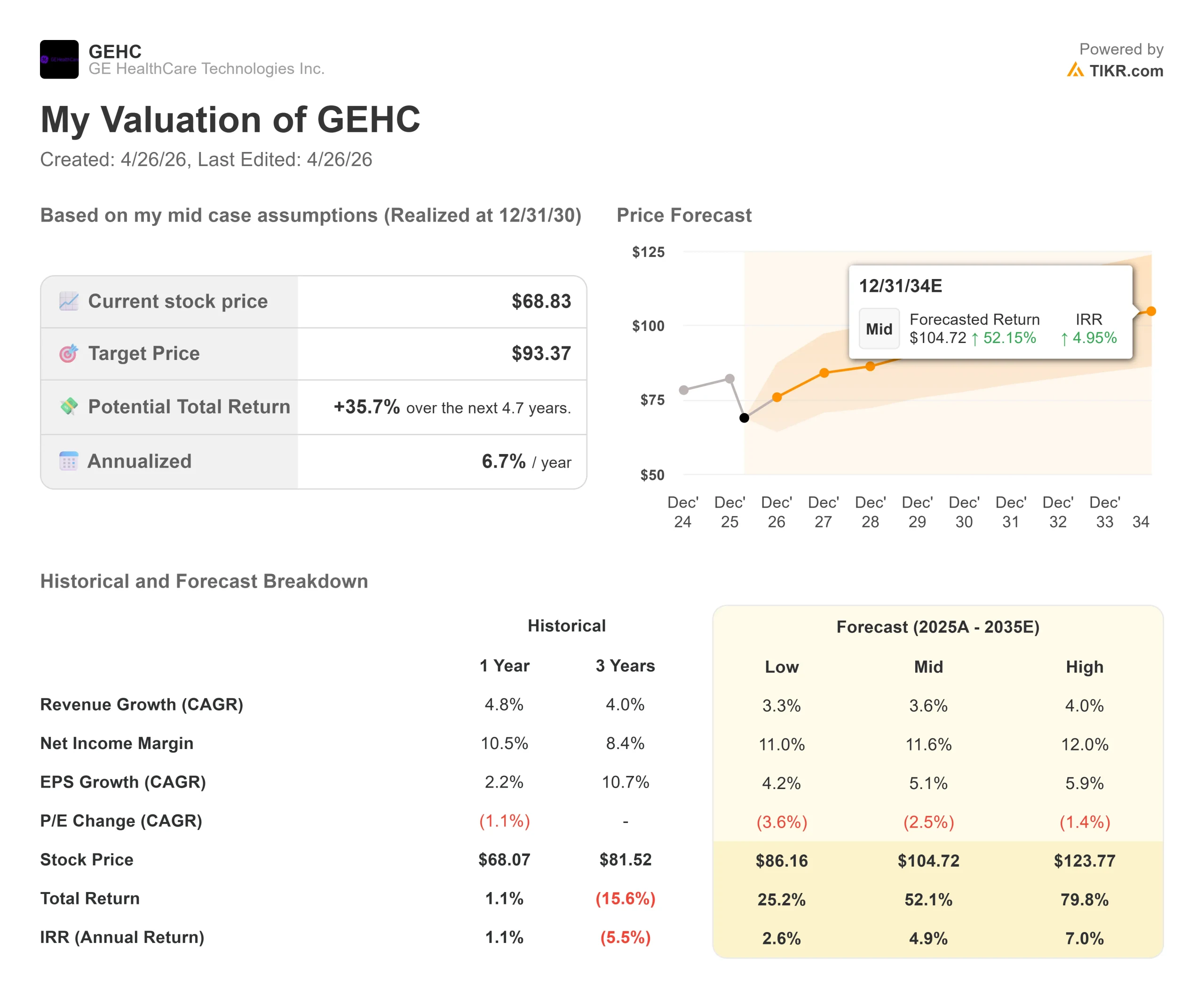

- Current Price: $68.83

- Target Price (Mid): ~$93

- Street Target: ~$91

- Potential Total Return: ~36%

- Annualized IRR: ~7% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

GE Healthcare (GEHC) stock sits 23% below its 52-week high of $89.77, near its lowest level since the company’s 2023 spinoff from General Electric. The gap between price and analyst consensus is as wide as it has ever been.

Bulls point to a $21.8 billion order backlog, a newly FDA-cleared next-generation CT scanner, and a closed $2.3 billion software acquisition as proof that the market has overshot. Bears argue that deliberate China budget cuts, tariff margin pressure, and a product cycle that won’t meaningfully show up in revenue until 2027 all justify the discount.

Q1 2026 results land before the market opens on April 29, and that report is about to force a verdict.

The biggest recent catalyst was the March 23 FDA 510(k) clearance of Photonova Spectra, GE HealthCare’s photon-counting computed tomography system powered by its proprietary Deep Silicon detector technology. The company, called Photonova, is the result of a $5.1 billion R&D investment since 2024 and said the platform is expected to add 1% to 2% in annual revenue growth over time. That clearance arrived five days after GE HealthCare completed its $2.3 billion acquisition of Intelerad, a cloud-based medical imaging workflow software provider.

Two major catalysts in one week, and the stock barely moved.

Citi Research noted that the typical six-to-nine-month capital equipment order cycle means Photonova revenue will not contribute meaningfully until 2027, a timeline CEO Peter Arduini confirmed on the Q4 earnings call. The flat stock reaction reflects a market waiting for execution, not news.

Peter Arduini, President and Chief Executive Officer, framed the year on the February 4 earnings call: “We delivered a strong quarter and year with growth in Pharmaceutical Diagnostics, Imaging, and Advanced Visualization Solutions.

This reflects healthy capital investment trends, commercial execution, and demand for new products.” GE HealthCare Full-year 2025 revenue came in at $20.6 billion, up 4.8%, with the Imaging segment growing 6.6% in Q4 to $2.55 billion and Pharmaceutical Diagnostics posting 22.3% organic growth in the quarter.

See historical and forward estimates for GE Healthcare stock (It’s free!) >>>

Is GE Healthcare Undervalued Today?

At $68.83, GEHC trades at 13.6x next twelve months earnings and 9.4x NTM EV/EBITDA, both near the lowest levels since the IPO. Nineteen analysts have published price targets averaging $90.74, implying roughly 32% upside.

The company runs at two very different speeds.

Pharmaceutical Diagnostics (PDx), the segment that sells contrast media and radiopharmaceuticals used to enhance diagnostic scans, grew 22.3% organically in Q4 2025, driven by Flyrcado, a cardiac positron emission tomography agent that measures blood flow to the heart.

Imaging, the company’s largest business at roughly $9.2 billion in 2025 revenue, is growing at low-to-mid single digits. The current multiple prices in Imaging’s pace ignore PDx’s acceleration entirely, which is where a large part of the re-rating case lives.

The bear argument rests on two measurable headwinds. CFO Jay Saccaro stated on the Q4 call that the company is “anticipating a decline in China in 2026,” with that caution baked into full-year organic revenue guidance of 3% to 4%. On top of that, roughly $100 million in tariff expense hit Q4 adjusted EBIT margin, pushing it down 200 basis points to 16.7%, and management flagged Q1 2026 as the heaviest tariff quarter of the year.

That means the April 29 print will carry the single worst margin quarter of 2026 before conditions improve.

What the bears may be underpricing is the demand picture.

On the Q4 call, Arduini noted that a recent U.S. customer survey showed an increase in the number of large customers planning to invest in capital equipment in 2026. The company exited 2025 with a record $21.8 billion backlog and a book-to-bill ratio of 1.06x in Q4 and 1.07x on a trailing twelve-month basis, meaning orders have consistently outpaced revenue. Piper Sandler cut its price target from $96 to $88 on April 17 while keeping its Overweight rating, a reset rather than a retreat.

The free cash flow picture adds context.

The company generated $1.5 billion in FCF in 2025 and guided for approximately $1.7 billion in 2026, representing 13% growth. At today’s market cap of around $31 billion, GEHC trades at around 19x forward free cash flow, a compressed level for a business with a record backlog and a software acquisition adding recurring, higher-margin revenue from day one. The company funded the $2.3 billion Intelerad deal from consistent free cash flow, keeping net leverage near 1.5x EBITDA.

See how GE Healthcare performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $68.83

- Target Price (Mid): ~$93

- Potential Total Return: ~36%

- Annualized IRR: ~7% / year

See analysts’ growth forecasts and price targets for GE Healthcare stock (It’s free!) >>>

The TIKR mid-case model targets approximately $93 for GEHC by December 31, 2030, implying around 36% total return and roughly 7% annualized. The two primary revenue drivers are PDx volume growth as Flyrcado doses scale toward management’s $500 million revenue target by end-2028, and Intelerad’s cloud software recurring revenue compounding at low double digits from its 2026 base. The model runs on a revenue CAGR of around 3.5% to 4% and assumes net income margins expand from 10.2% in 2025 to around 12% in the mid case, driven by Intelerad’s software mix and a declining tariff headwind.

The upside requires Photonova to capture U.S. hospital share from Siemens Healthineers’ competing platform and Flyrcado to hit its dose targets on schedule. The downside, if China remains a sustained drag and tariff mitigation stalls, still implies a positive total return from today’s price, which is not the profile of a stock that has fully priced in a recovery. The primary near-term risk is that Q1 prints below the full-year 2025 adjusted EBIT margin of 15.3% and management trims the 2026 EPS guidance range of $4.95 to $5.15, which would likely push GEHC toward its 52-week low of $66.95.

Conclusion

Watch the adjusted EBIT margin on April 29. Management guided the full year at 15.8% to 16.1% and called Q1 the toughest tariff quarter. If the margin holds near that range and the EPS guide stays intact, the 23% discount to the $90.74 Street mean is difficult to justify. If the margin disappoints and guidance is trimmed, the stock likely retests $67 before the 2027 product cycle takes over.

GEHC is a medical technology business trading at a trough valuation multiple, with a product cycle entering commercialization, a software acquisition adding day-one recurring cash flow, and five consecutive quarters of earnings beats already on record. One more difficult quarter stands between today’s price and the point where the investment case becomes very hard to ignore.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in GE Healthcare?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE Healthcare, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE Healthcare alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze GE Healthcare on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!