Key Stats

- Current price: ~$22

- Q1 FY2026 revenue: $1.74B (+14% reported; +9% organic YoY)

- Q1 FY2026 adjusted EPS: $0.42 (+11% YoY)

- Full-year FY2026 reported revenue guidance: +5.5% to +6.5%

- Full-year FY2026 organic revenue guidance: +4.5% to +5.5%

- Full-year FY2026 adjusted diluted EPS guidance: $1.42–$1.48

- TIKR model price target: $38

- Implied upside after ~6 years: ~69%

Levi Strauss Q1 FY2026 Earnings Breakdown

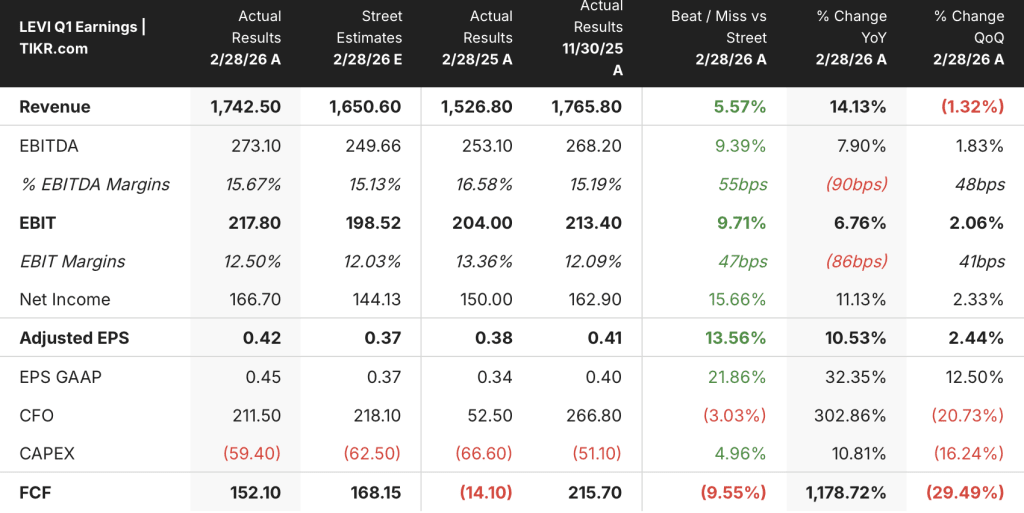

Levi Strauss stock (LEVI) posted Q1 FY2026 revenue of $1.74B, up 14% on a reported basis and up 9% organically, beating expectations across every region and channel.

Adjusted EPS came in at $0.42, up 11% year-over-year and ahead of the $0.38 delivered in the prior-year Q1.

DTC led the growth with a 10% increase and 7% comparable sales growth, marking the 16th consecutive quarter of positive comps, while wholesale outperformed expectations at +8%.

Women’s was the standout by category, up 13%, and tops delivered the same 13% growth, demonstrating traction in the brand’s expansion beyond core bottoms.

International markets contributed roughly 75% of total growth, with Europe up 10% and Asia up 12%, while the Americas grew 7%, including 4% in the U.S. and 14% in Latin America.

Adjusted EBIT margin was 12.5% for the quarter. According to CFO Harmit Singh on the Q1 2026 earnings call, normalizing for front-loaded advertising spend, the underlying margin would have been 14.1%, reflecting roughly 40% flow-through from higher revenue.

A $30M European wholesale shipment timing benefit pulled approximately 2 percentage points of growth into Q1 from Q2, a known headwind management flagged for next quarter.

Shareholder returns totaled $214M in Q1, up 163% year-over-year, supported by net proceeds from the Dockers divestiture completing in the quarter.

Levi Strauss stock now carries raised full-year FY2026 guidance: reported revenue growth of +5.5% to +6.5%, organic revenue growth of +4.5% to +5.5%, and adjusted diluted EPS of $1.42 to $1.48, up from the prior range of $1.40 to $1.46.

The company also announced the planned retirement of CFO Harmit Singh after 13 years, with a successor search underway and Singh confirmed to remain in role until a replacement is appointed.

Levi Strauss Stock: Financials

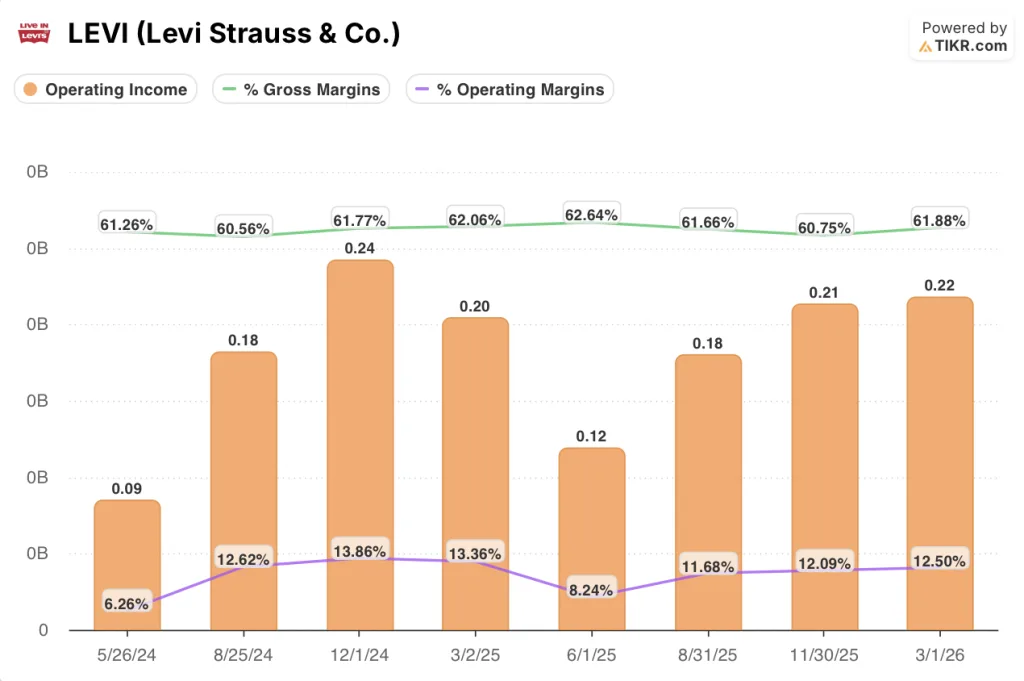

The Q1 income statement reflects a resilience story: gross margin held near recent highs despite tariff pressure, and operating income continued expanding.

Gross margin came in at 62% for the quarter ended March 1, 2026, contracting 20 basis points from the 62.1% posted in the prior-year Q1, with tariffs cited as the primary driver.

That contraction was partially offset by pricing actions and reduced promotional activity, according to Harmit Singh on the Q1 2026 earnings call.

The multi-quarter gross margin trend has been consistent: 62.1% in March 2025, 62.6% in June 2025, 61.7% in August 2025, 60.8% in November 2025, and ~62% in the current quarter.

Operating margin was 12.5% in Q1, compared to 13.4% in the March 2025 quarter, with the sequential decline reflecting front-loaded A&P investment.

Operating income reached $220M in Q1 FY2026, up 6.8% from $200M in the prior-year Q1 per the income statement.

Management guided full-year adjusted EBIT margin to approximately 12%, up from the prior range of 11.8% to 12%, with H2 margins expected to reach 13% to 14% as A&P normalizes and U.S. distribution costs fall as the DC transition completes mid-year, according to Harmit Singh on the Q1 2026 earnings call.

Levi Strauss Stock: Valuation Model Take

The TIKR model prices Levi Strauss stock at $38, implying roughly 69% total upside from the current ~$22 price over approximately 6 years, or about 12% annually.

The mid-case assumes revenue CAGR of 6% and net income margin of 10% from 2025 through 2035, with EPS growing at roughly 10% per year.

Q1’s 9% organic growth came in above the modeled revenue CAGR, and management raised guidance rather than pulling back despite an uncertain macro environment.

Levi Strauss stock appears undervalued relative to the TIKR model, and this quarter reinforces that view: a guidance raise, 16 consecutive positive comp quarters, and a 14% underlying EBIT margin all point to a business executing ahead of plan.

The central tension: Levi Strauss stock beat on every line in Q1, but the full-year guidance raise was modest, and the debate is whether that caution reflects discipline or a real deceleration ahead.

Bull Case

- Q1’s 9% organic growth came in well above the full-year guidance midpoint of 5%, and management cited a prudent macro outlook rather than weakening demand as the reason for limited guidance upside

- DTC hit its 16th consecutive quarter of positive comps at 7% growth, and e-commerce grew 17%, with 70% of new U.S. e-commerce orders coming from Gen Z and millennials

- The Blue Tab premium line grew 40% in Q1 with just 1% share of the $10B premium denim market, representing meaningful margin accretion potential beyond the core

- If the current 10% tariff rate holds through year-end, management quantified a potential incremental $35M COGS benefit and $0.07 EPS upside not reflected in current guidance

Bear Case

- The $30M European wholesale timing benefit added roughly 2 percentage points to Q1 revenue growth, creating a known headwind in Q2, where organic revenue is guided to only 3% to 4%

- CFO Harmit Singh’s retirement after 13 years introduces succession risk at a critical execution phase, with the company targeting its first sustained run above 12% EBIT margin

- Adjusted SG&A grew 16% in Q1 due to front-loaded A&P and FX headwinds; if H2 A&P normalization does not fully materialize, the path to 13% to 14% H2 margins narrows

- Q2 adjusted EBIT margin is guided to 8% to 9%, a sharp step-down from Q1’s 12.5%, and any volume miss would reduce the fixed-cost leverage underpinning the projected H2 recovery

Should You Invest in Levi Strauss & Co.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LEVI stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Levi Strauss & Co. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LEVI stock on TIKR for Free →