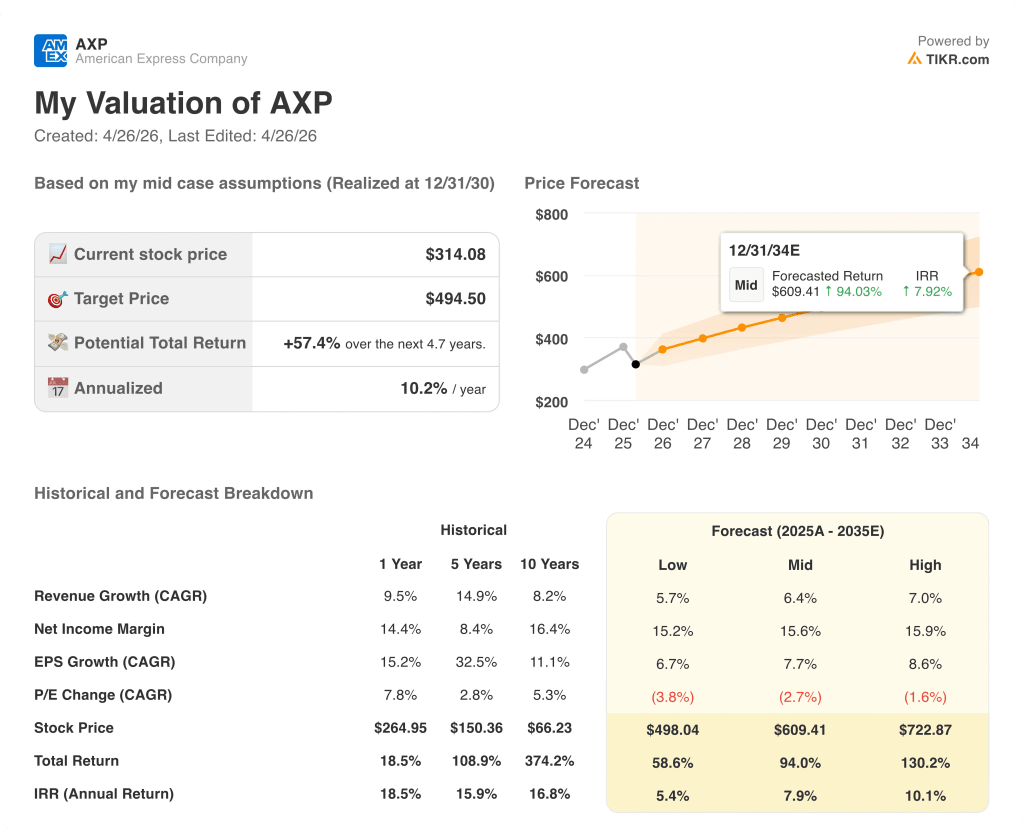

Key Stats

- Current price: ~$314

- Q1 2026 revenue: $18.9B, up ~11% YoY

- Q1 2026 EPS: $4.28, up ~18% YoY

- Full-year 2026 revenue guidance: 9% to 10% growth (reaffirmed)

- Full-year 2026 EPS guidance: $17.3 to $17.9 (reaffirmed)

- TIKR model price target: ~$495 (mid case)

- Implied upside: ~57% over approximately 5 years (~10% annualized)

American Express Stock Delivers Strongest Spending Quarter in Three Years

American Express stock (AXP) opened Q1 2026 with $18.9B in revenue, up 11% year-over-year, and EPS of $4.28, up 18% from the prior-year March quarter.

Card Member spending grew 10% on a reported basis, the highest quarterly growth rate in three years, with Travel and Entertainment up 9% on an FX-adjusted basis and Goods and Services up 8%.

The U.S. Platinum portfolio was the standout driver, with spend growth accelerating 6 percentage points year-over-year following last year’s product refresh and fee increase.

About 25% of the Platinum portfolio has been billed at the higher annual fee, and retention rates have not changed from pre-refresh levels, according to CFO Christophe Le Caillec on the Q1 earnings call.

International Card Services posted billings growth of 13% on an FX-adjusted basis, extending its streak of double-digit FX-adjusted billings growth to 20 consecutive quarters.

Net card fees were the fastest-growing revenue line, up 16% FX-adjusted, in line with Q4 2025, and management expects card fee growth to accelerate into the high teens as the year progresses and the Platinum refresh anniversary approaches.

Net interest income grew 12% FX-adjusted again this quarter, outpacing balance growth of 7%, while write-off dollars rose only 4% year-over-year, according to Le Caillec on the Q1 earnings call.

“We saw record billings” against a backdrop of geopolitical uncertainty, said Chairman and CEO Stephen Squeri on the Q1 earnings call, noting luxury retail spending up 18% and front-of-cabin airline spending up 12%.

Capital returned to shareholders in Q1 totaled $2.3B, including $700M in dividends and $1.7B in share repurchases, with the quarterly dividend increased 16%.

Management flagged softness in airline spending in late March and early April tied to Middle East travel disruptions, but characterized the impact as immaterial to overall billing trends.

American Express also announced plans to launch 8 new or enhanced commercial products in 2026, including a corporate cash back card and expense management software, described by Squeri as the most significant single-year commercial product expansion in company history.

Full-year 2026 guidance was reaffirmed at 9% to 10% revenue growth and EPS of $17.30 to $17.90, with management electing to reinvest Q1’s earnings upside into incremental marketing and technology rather than raise the bottom-line guide.

American Express Stock: What the Income Statement Shows

The Q1 2026 income statement for American Express stock shows operating leverage building steadily across a sustained revenue acceleration.

Total revenues reached $17.66B in Q1 2026, up 11.6% year-over-year from $15.82B in Q1 2025.

Revenue growth had been running at 8.7% in Q2 2024 and 8.0% in Q3 2024 before accelerating to 10.6% in Q4 2024, 8.8% in Q1 2025, and then picking up sequentially through Q2 and Q3 2025 at 9.2% and 12.2%, respectively.

Operating income reached $3.78B in Q1 2026, up 13.5% year-over-year from $3.33B in the prior-year March quarter.

Operating margin expanded to 21.4% in Q1 2026, up from 21.1% in Q1 2025, recovering from the trough of 17.5% in Q4 2025.

The Q4 2025 margin compression to 17.5% reflected elevated Total Operating Expenses of $14.50B in that quarter, the highest in the period shown on the income statement screenshot.

Q1 2026 operating expenses pulled back to $13.88B, which Le Caillec attributed on the Q1 earnings call to VCE-to-revenue running at 44.7% in Q1, in line with expectations, with the company targeting approximately 44% for the full year.

What Does the Valuation Model Say?

The TIKR valuation model places a mid-case price target of approximately $495 on American Express stock, representing roughly 57% potential total return from the current price of ~$314 over approximately 4.7 years, at an annualized rate of about 10%.

The mid-case model assumes a revenue CAGR of 6.4% and a net income margin of 15.6% through 2035, against a historical 1-year net income margin of 14.4%.

The Q1 result strengthens the investment case on both dimensions: 11% revenue growth in a geopolitically uncertain environment sits well above the 6.4% modeled CAGR, and the combination of operating margin expansion and best-in-class credit metrics supports the assumption that margins can widen from here.

The risk/reward on American Express stock looks stronger after this report than before it.

The central tension: American Express stock is executing ahead of its model assumptions today, but the question is whether 11% revenue growth is repeatable as co-brand exits create a headwind and the platinum refresh annualizes.

Bull Case

- Q1 billed business growth of 10% was the highest in three years and accelerated by approximately 1 percentage point versus Q4 2025, with luxury retail spending up 18% and front-of-cabin travel up 12%.

- Net card fees grew 16% FX-adjusted in Q1 and management guided that growth will accelerate into the high teens as the year progresses, driven by approximately 75% of the Platinum portfolio still yet to be billed at the higher annual fee.

- International Card Services has now delivered double-digit FX-adjusted billings growth for 20 consecutive quarters, providing a durable non-U.S. growth engine.

- The commercial product expansion, including 8 new or enhanced products in 2026, is expected to contribute tailwinds in 2027, extending the growth runway beyond the current platinum refresh cycle.

Bear Case

- Management explicitly flagged that the Amazon and Lowe’s co-brand exits will create a low-single-digit drag on SME spend growth starting in Q2, with zero impact on pretax income but a visible revenue headwind.

- Airline spending softened in late March and into early April due to Middle East travel disruptions, and while management called the impact immaterial, T&E remains a meaningful portion of the billed business mix.

- The platinum refresh tailwind is expected to annualize sometime in 2027, and Le Caillec cautioned on the Q1 earnings call against expecting another step-up acceleration in billed business growth beyond the current 6-percentage-point lift.

- At ~$314 per share, the stock is already pricing in continued execution, and the TIKR model’s low-case scenario implies a total return of only 58.6% to ~$498 by year-end 2030, leaving limited room for guidance disappointment.

Should You Invest in American Express Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AXP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track American Express Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AXP stock on TIKR for Free →