Key Takeaways:

- Comp Growth Acceleration: Q3 comparable store sales surged 7%, up 3% year-on-year

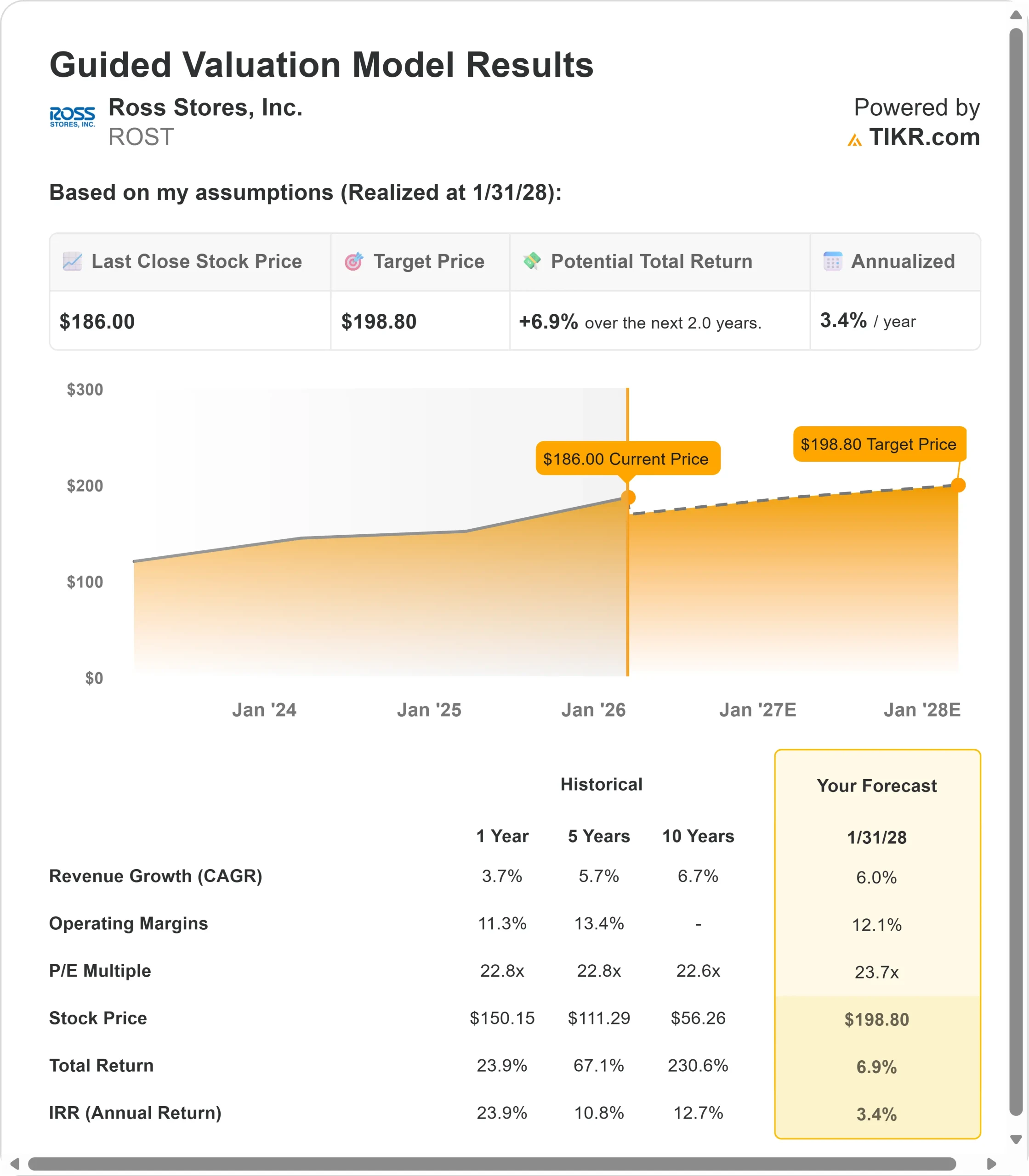

- Price Projection: Based on our assumptions, ROST stock could reach $199 by January 2028

- Potential Gains: This target implies a total return of 7% from the current price of $186

- Annual Return: Investors could see roughly 3.4% growth over the next 2 years

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Ross Stores (ROST) just delivered a strong quarterly performance. The off-price retailer posted a 7% comparable store sales increase in Q3, significantly outpacing the growth seen in the first nine months of the year.

CEO Jim Conroy’s branded merchandise strategy is paying off. The company opened 90 new stores in 2025 while maintaining disciplined expense control.

With tariff headwinds now in the rearview mirror and a refreshed marketing approach driving traffic, Ross is capturing market share during a challenging retail environment.

Despite near-term economic uncertainties, ROST stock trades at $186, offering modest upside for investors who recognize the company’s execution momentum and value proposition.

See analysts’ full growth forecasts and estimates for ROST stock (It’s free) >>>

What the Model Says for Ross Stores Stock

We analyzed Ross through its transformation into a more brand-focused off-price powerhouse with strengthened customer engagement.

- The company is executing a multifaceted strategy that combines merchandising improvements, a marketing refresh, and store experience upgrades.

- The branded merchandise initiative, which particularly boosted the ladies’ business, has now been embedded for over a year and is driving sequential improvement across categories.

- New marketing campaigns are resonating with younger customers while store refreshes are halfway complete across the chain.

- Management successfully navigated tariff challenges through vendor negotiations and opportunistic buying, with Q4 tariff impact now expected to be negligible.

Using a forecast of 6% annual revenue growth and 12.1% operating margins, our model projects the stock will rise to $199 within 2 years. This assumes a 23.7x price-to-earnings multiple.

That represents a slight compression from Ross’s historical P/E averages of 22.8x (one year and five years). The modest multiple reflects ongoing macro uncertainty and consumer caution, though the company’s value positioning should provide resilience.

The real opportunity lies in the sustainability of comp acceleration and margin expansion as branded strategies mature and store experience improvements compound.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ROST stock:

1. Revenue Growth: 6.0%

Ross’s growth centers on comparable-store sales momentum and new-store productivity. The company delivered 7% comps in Q3 with broad-based strength across all major merchandise categories and geographies.

Management guided Q4 comps to 3-4%, marking a notable departure from their traditional 2-3% guidance range.

The branded merchandise strategy is driving results. Ladies’ business, which had lagged, now comps above the chain average.

The company opened 90 stores in 2025, including successful entries into the Northeast and New York metro area. New stores are outperforming plans, particularly the Brooklyn location, which has generated significant buzz.

Ross plans a gradual expansion into new markets while maintaining roughly 70% of its openings in existing markets. With 1,903 Ross stores and 360 dd’s DISCOUNTS locations, the runway remains substantial.

2. Operating margins: 12.1%

Ross is managing margins carefully while investing in growth. Q3 operating margin decreased to 11.6% mainly on account of tariffs and related distribution costs. The company successfully offset tariff impacts through vendor cost concessions and opportunistic closeout buying.

Merchandise margins remained relatively stable with only 10 basis points of deleverage. Management expects continued opportunity to gain leverage as branded vendor relationships deepen and provide more closeout access.

The company is investing in store refreshes, the rollout of self-checkout in high-volume locations, and marketing, all within its existing expense structure.

3. Exit P/E Multiple: 23.7x

The market currently values Ross at 26.6x earnings. We assume the P/E will compress modestly to 23.7x over our forecast period, roughly in line with historical averages.

Near-term macro uncertainties and consumer caution warrant a conservative multiple. However, Ross’s value proposition strengthens during economic uncertainty. As the branded strategy matures and traffic-driving initiatives compound, Ross should maintain a premium multiple within the off-price sector.

The company generated strong free cash flow and returned $262 million to shareholders through buybacks in Q3 alone, remaining on track to repurchase $1.05 billion for the year.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

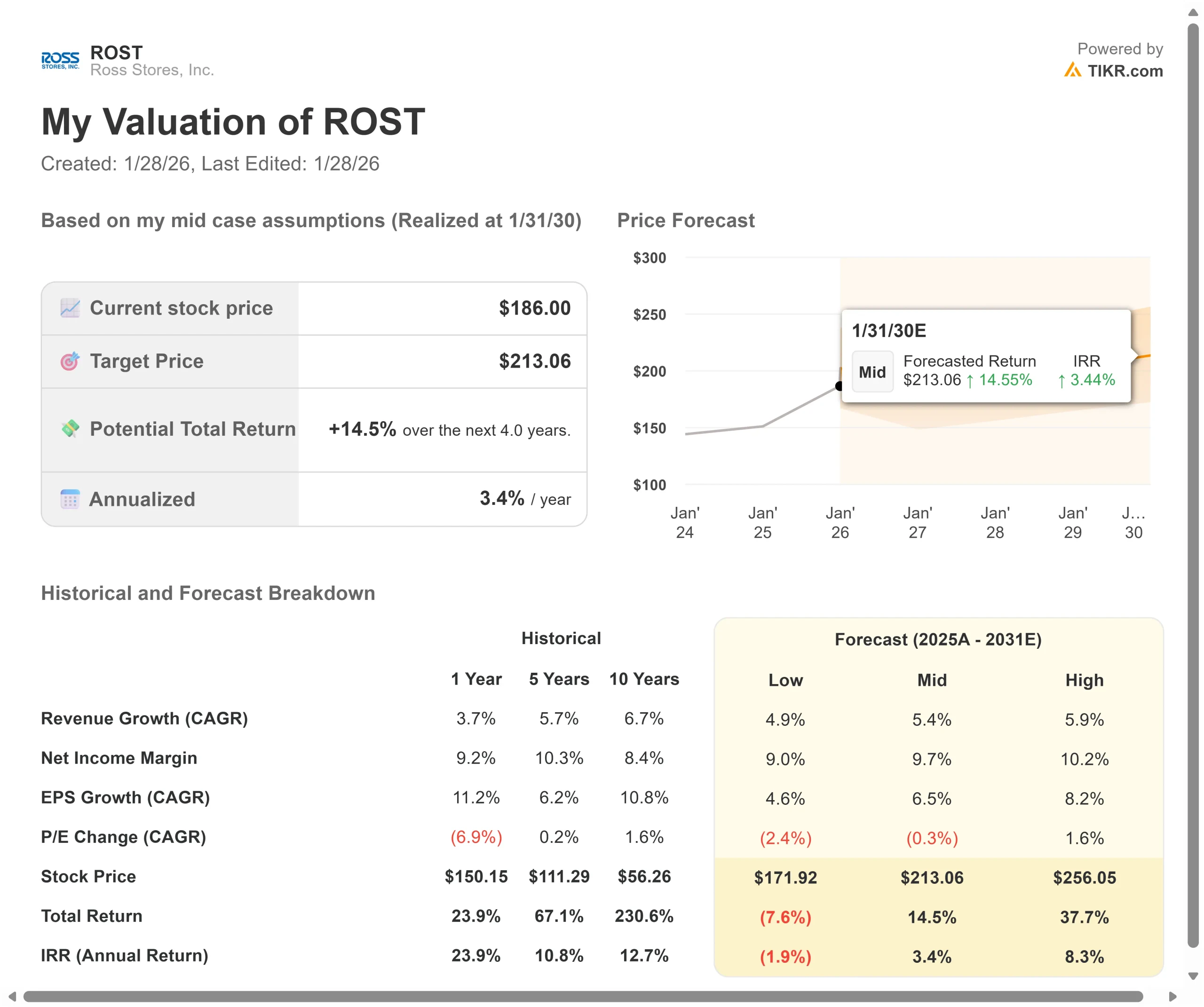

Off-price retailers face economic cycles and competitive pressures. Here’s how Ross stock might perform under different scenarios through January 2030:

- Low Case: If revenue growth slows to 4.9% and margins compress to 9%, investors could see a decline of 8% total return (-1.9% annually).

- Mid Case: With 5.4% growth and 9.7% margins, we expect a total return of 14.5% (3.4% annually).

- High Case: If comp momentum continues and Ross maintains 10.2% margins while growing at 5.9%, returns could hit 37.7% total (8.3% annually).

See what analysts think about ROST stock right now (Free with TIKR) >>>

The range reflects execution on brand strategy sustainability, success in new markets, and macroeconomic conditions impacting consumer spending.

In the low case, consumer spending deteriorates, or competitive pressures intensify, forcing promotional activity.

In the high case, the value proposition drives continued market share gains, new store productivity exceeds expectations, and branded relationships generate increasing closeout opportunities that support both sales and margins.

How Much Upside Does Ross Stores Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!