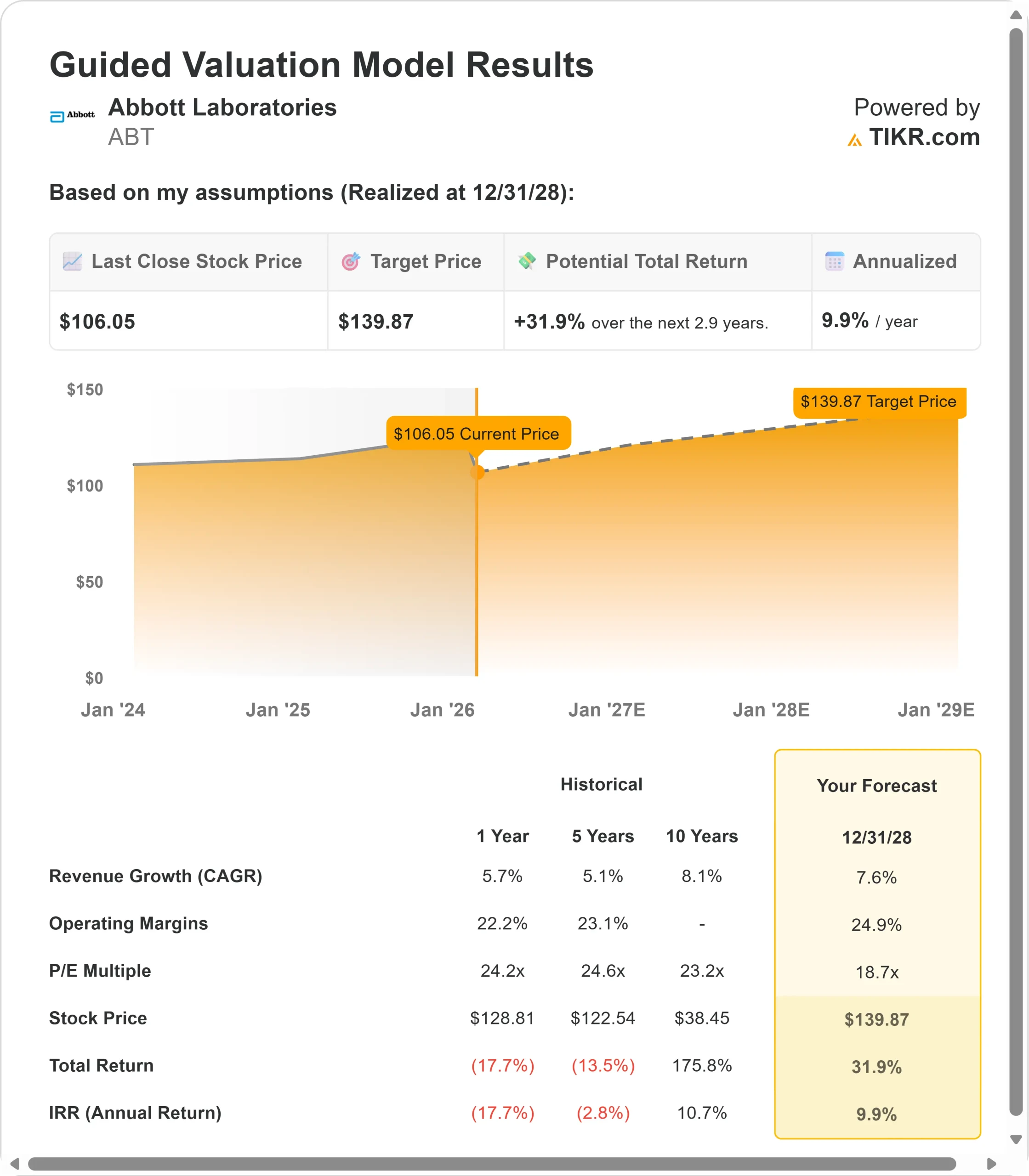

Key Takeaways:

- Revenue Growth: 7.6% annually through 2028, driven by Medical Devices and Diagnostics recovery

- Price Projection: Based on current execution, ABT stock could reach $140 by December 2028

- Potential Gains: This target implies a total return of 32% from the current price of $106

- Annual Return: Investors could see roughly 9.9% growth over the next 2.9 years

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Abbott Laboratories (ABT) just wrapped up a strong 2025 despite navigating challenges in its Nutrition business. The healthcare giant delivered double-digit earnings growth while advancing its product pipeline across multiple franchises.

CEO Robert Ford is executing a dual strategy: sustaining high-single-digit growth in diabetes and cardiovascular products while positioning foundational businesses, such as Rhythm Management, for acceleration.

With regulatory approval in Electrophysiology and the pending Exact Sciences acquisition adding a cancer diagnostics vertical, Abbott is capturing market share through innovations and acquisitions.

Adjusted operating margin expanded 150 basis points year-over-year to 25.8%, driven by disciplined cost control and manufacturing efficiency. The company expects to maintain margin expansion of 50-70 basis points annually.

Despite near-term headwinds in Nutrition, Abbott stock trades at $106, offering upside for investors who recognize the company’s innovation momentum and strategic positioning.

See analysts’ full growth forecasts and estimates for ABT stock (It’s free) >>>

What the Model Says for Abbott Stock

We analyzed Abbott through its transformation into a diversified healthcare leader with sustained innovation across devices, diagnostics, and nutrition.

The company is expanding into high-growth segments such as continuous glucose monitors and structural heart, while recovering from diagnostics headwinds in China.

CGM sales exceeded $7.5 billion in 2025, marking the third consecutive year of adding more than $1 billion in sales. Management targets 6.5-7% organic growth in 2026 as the Nutrition business transitions back to volume-driven growth in the second half.

Using a forecast of 7.6% annual revenue growth and 24.9% operating margins, our model projects the stock will rise to $140 within 2.9 years. This assumes an 18.7x price-to-earnings multiple.

That represents compression from Abbott’s historical P/E averages of 24.2x (one year) and 24.6x (five years). The lower multiple acknowledges near-term Nutrition challenges and the integration of Exact Sciences.

The real value lies in executing the Medical Devices pipeline and leveraging the diagnostics recovery as China VBP headwinds dissipate.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ABT stock:

1. Revenue Growth: 7.6%

Abbott’s growth centers on the momentum of its Medical Devices business.

- CGM grew 17% in 2025, driven by strong adoption across all user segments.

- The team expects to add another $1 billion in sales in 2026, putting growth in the low-teens range.

- Intensive Insulin market penetration remains below 50% internationally, with additional upside from potential expansion of non-insulin Type 2 diabetes coverage in the U.S.

Structural Heart delivered double-digit growth across Navitor TAVR, TriClip, and MitraClip. Japan’s approval for TriClip opens a significant new market.

Electrophysiology launched Volt PFA in the U.S. and TactiFlex Duo internationally, positioning Abbott to grow in line with the mid-to-high teens EP market.

Diagnostics faces a transitional year but should accelerate to mid-single-digit growth as China VBP headwinds fade. The business took $1 billion in combined COVID and China VBP impact in 2025.

With Core Lab gaining share in the U.S., Europe, and Latin America, and COVID sales stabilizing around $200 million, the diagnostic franchise is positioned for recovery.

Nutrition remains challenged in the first half as the company implements pricing and promotional strategies to reignite volume growth.

Management expects a return to growth in the second half with eight new product launches over the next 12 months.

2. Operating margins: 24.9%

Abbott is expanding margins while investing in growth. The company delivered 150 basis points of operating margin expansion in Q4 to 25.8%, and management targets 50-70 basis points of annual improvement.

Gross margin expanded 20 basis points despite tariff impacts, demonstrating pricing power and manufacturing efficiency.

The team is reallocating resources in Nutrition to balance near-term promotional spending with long-term innovation while maintaining the division’s profitability profile.

3. Exit P/E Multiple: 18.7x

The market values Abbott at 24.2x earnings. We assume the P/E will compress to 18.7x over our forecast period.

Near-term Nutrition headwinds and Exact Sciences integration ($0.20 dilution initially) weigh on the multiple. The company will carry 2.7x gross debt-to-EBITDA post-acquisition.

As the product pipeline delivers and diagnostics accelerate, Abbott should maintain a premium multiple.

The company generates strong free cash flow conversion and maintains market-leading positions across multiple device categories. The Exact Sciences deal adds a fast-growing cancer diagnostics platform with 15% growth potential and significant upside from multi-cancer early detection tests.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Healthcare companies face economic cycles and execution risks. Here’s how Abbott stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 6.5% and the Margin level reaches 20.4%, investors still see a 31.5% total return (5.7% annually).

- Mid Case: With 7.2% growth and a margin growth of 21.7%, we expect a total return of 62.4% (10.3% annually).

- High Case: If Medical Devices accelerates and Abbott maintains a 22.9% margin while growing at 7.9%, returns could reach 95.0% total (14.5% annually).

See what analysts think about ABT stock right now (Free with TIKR) >>>

The range reflects execution on CGM penetration, EP market share capture, Nutrition recovery timing, and Exact Sciences integration success.

In the low case, non-insulin Type 2 coverage delays or competitive pressure in CGM persists.

In the high case, faster regulatory approvals for the dual glucose-ketone sensor and balloon TAVR, combined with successful Exact integration and multi-cancer test adoption, drive upside.

How Much Upside Does Abbott Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!