Key Stats for Adobe Stock

- 52-Week Range: $224 to $423

- Current Price: $254

- Street Mean Target: $329

- Street High Target: $487

- Analyst Consensus: 13 Buys / 3 Outperforms / 18 Holds / 4 Sells

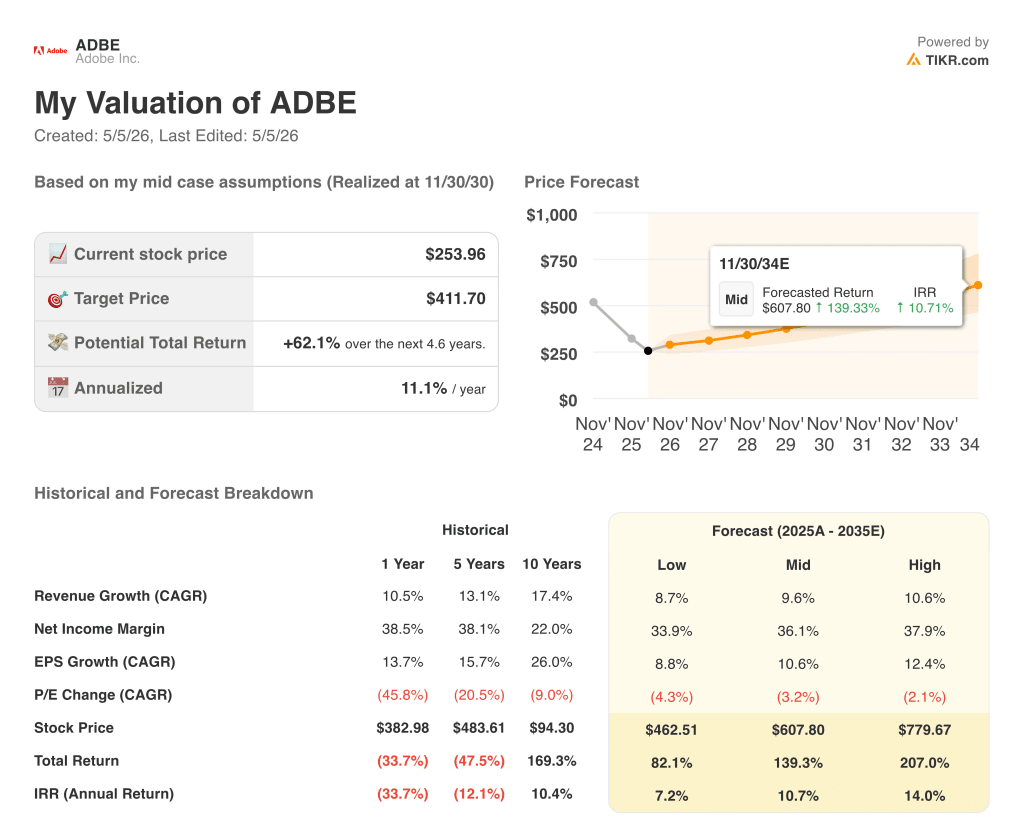

- TIKR Model Target (Dec. 2030): $412

What Happened?

Adobe (ADBE), the design and customer experience software company behind Photoshop, Acrobat, and a growing suite of AI tools, reported $6.40 billion in revenue for Q1 fiscal 2026, beating the consensus estimate of $6.28 billion by a meaningful margin.

The most important number was not the revenue beat itself but the 19% year-over-year growth in non-GAAP EPS to $6.06, which arrived alongside a reaffirmed full-year guidance target implying 10.2% total ARR growth for fiscal 2026.

Adobe’s monthly active users surpassed 850 million, growing 17% year-over-year, a figure that represents more than one in ten people on the planet engaging with Adobe products each month.

CEO Shantanu Narayen stated on the Q1 2026 earnings call that “our new AI-first offerings ending ARR more than tripled year-over-year, reflecting progress against this opportunity with individuals and enterprises alike,” tying the metric directly to Adobe’s freemium expansion and enterprise automation momentum.

Adobe then launched CX Enterprise at its April Summit, a full agentic AI platform integrating Firefly creative tools with GenStudio and the Adobe Experience Platform, while simultaneously announcing a $25 billion share buyback authorized through April 2030 and completing its acquisition of Semrush to add SEO and generative engine optimization capabilities to its brand visibility suite.

The $25 billion buyback authorization, running through April 2030, arrived after a 24% year-to-date decline in Adobe stock, a direct statement from the board that the current price is wrong.

Wall Street’s Take on ADBE Stock

The Q1 revenue beat and the CX Enterprise launch shift the question from whether Adobe can adapt to AI to how fast that adaptation translates into ARR acceleration, and the answer arrives in the next two quarters.

Adobe’s normalized EPS grew 19% year-over-year to $6.06 in Q1, and consensus estimates project around $6 per share for Q2 and approximately $24 for the full fiscal year, supported by the freemium MAU engine converting at scale and Firefly Enterprise new customer acquisition growing 50% year-over-year.

Thirteen analysts rate Adobe stock a buy or better, three rate it outperform, eighteen hold, and four sell, with a mean price target of around $329 representing roughly 30% upside from the current price of $253.96, as Wall Street waits for AI-first ARR to move from a tripling base off near-zero to a measurable portion of the $26 billion total ARR book.

The target spread runs from $220 at the low end, anchored by competition fears in the prosumer and SMB segments where Canva and Figma are both growing ARR at 30% and 40% respectively, to $487 at the high end, a figure that requires CX Enterprise and Semrush to accelerate the enterprise platform transition meaningfully faster than the current timeline.

The $25 billion repurchase program is the clearest signal management has sent: at $254, the board believes the stock is mispriced, and the buyback reduces float by roughly 20% over four years at current prices.

The risk is CEO transition timing: Narayen leaving without a named successor creates a decision-making lag at the exact moment the CX Enterprise agentic platform requires aggressive enterprise sales execution.

The Q2 earnings report, expected in early June, is the catalyst to watch, specifically the net new ARR figure and whether AI-first ARR is tracking toward the next $1 billion threshold Narayen outlined on the Q1 call.

What Does the Valuation Model Say?

The TIKR model assigns a mid-case price target of around $412 for Adobe, a 62% premium to the current price, built on a revenue CAGR of around 10% through 2030, a net income margin of approximately 36%, and an EPS CAGR of around 11% per year, inputs that are already visible in the Q1 actuals and that management reaffirmed at April’s Summit investor session.

With the mid-case IRR running at around 11% annually and the low case still projecting a price of approximately $463 on a longer five-year horizon, Adobe stock appears undervalued: the market is pricing in meaningful multiple compression when the actual model requires only that Adobe sustain the revenue and EPS growth rates it has already demonstrated.

Adobe’s valuation hinges entirely on whether the AI platform transition bends the ARR growth curve before Canva, Figma, and Anthropic’s Claude Design close the gap in the segments Adobe has historically owned.

Firefly Enterprise new customer acquisition grew 50% year-over-year in Q1, and if that rate holds through Q3, AI-first ARR crosses $500 million within fiscal 2026, validating the path to the $1 billion threshold Narayen outlined before stepping down.

The 650 active customer trials for LLM Optimizer, Sites Optimizer, and Brand Concierge are the conversion pipeline that determines whether CX Enterprise becomes the next GenStudio or stalls at proof-of-concept.

LLM-driven retail traffic grew nearly 7x year-over-year in the 2025 holiday season, a data point that makes brand visibility spend non-discretionary and positions the Semrush acquisition as better-timed than the market currently credits.

The $25 billion buyback compresses share count by roughly 20% at current prices over four years, adding around 3% annual EPS accretion even if organic growth never re-accelerates.

The bear case is simpler: AI-first ARR below 2% of a $26 billion total book cannot bend the growth curve before Canva and Figma, both growing ARR at 30% and 40% respectively, take enough prosumer share to structurally cap Adobe’s Digital Media renewal pricing.

A CEO transition without a named successor creates a go-to-market execution gap at the precise moment CX Enterprise requires aggressive enterprise deployment, and Mizuho’s cut to neutral with a $270 target was specifically anchored to that timing risk.

The traditional stock library, a $450 million book already declining faster than planned in Q1, is the quiet drain: if generative substitution does not fully offset the erosion by fiscal 2027, net new ARR turns negative before the AI platform is large enough to compensate.

Should You Invest in Adobe Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Adobe Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Adobe Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ADBE stock on TIKR for Free →