Key Takeaways:

- LNG Export Boom: Feed gas demand expected to jump from 16.6 Bcf/day in 2025 to 19.8 Bcf/day in 2026

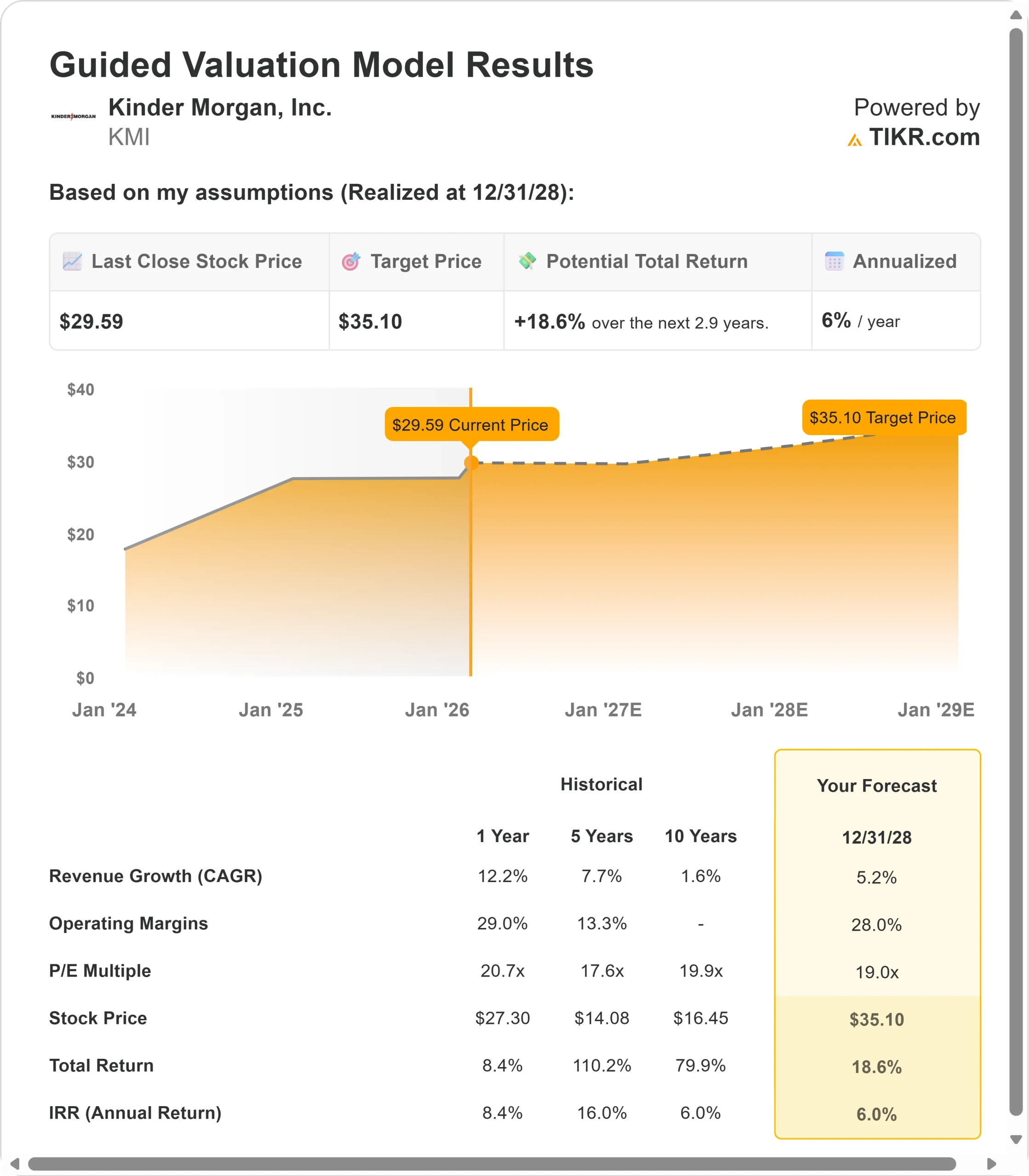

- Price Projection: Based on current execution, KMI stock could reach $35 by December 2028

- Potential Gains: This target implies a total return of 18.6% from the current price of $29.59

- Annual Return: Investors could see roughly 6% growth over the next 2.9 years

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Kinder Morgan (KMI) just posted its strongest quarter in company history. The midstream giant reported adjusted EBITDA up 10% and EPS jumping 22% in Q4 versus last year.

CEO Kim Dang credits one massive tailwind: surging natural gas demand driven by LNG exports and power generation.

The company now serves LNG feed gas flowing to Gulf Coast export terminals. That demand averaged 16.6 billion cubic feet per day in 2025 and is expected to hit 19.8 Bcf/day this year—a 19% increase. By 2030, management expects that figure to exceed 34 Bcf/day.

- Kinder Morgan’s $10 billion project backlog trades at a multiple below 6x EBITDA, suggesting attractive returns.

- The company recently upgraded its annual growth capital guidance from $2.5 billion to $3 billion, reflecting strong market fundamentals. S&P upgraded KMI to BBB+ last week, and the company reduced its net debt-to-EBITDA ratio to 3.8x.

- Natural gas transport volumes jumped 9% in Q4, while gathering volumes surged 19%. The Haynesville system alone hit a record 1.97 Bcf/day on December 24.

Despite near-term commodity price volatility, Kinder Morgan stock trades at $29.59, offering upside for investors who recognize the structural shift in U.S. energy infrastructure.

See analysts’ full growth forecasts and estimates for KMI stock (It’s free) >>>

What the Model Says for Kinder Morgan Stock

We analyzed Kinder Morgan through its dominance in U.S. natural gas infrastructure during an unprecedented demand surge.

The company operates extensive pipeline networks along the Texas-Louisiana Gulf Coast, exactly where LNG export terminals are concentrated. Management added $3.7 billion in new projects during 2025 while placing $1.8 billion into service, growing the backlog from $8.1 billion to $10 billion.

Three major projects—Mississippi Crossing, South System 4, and Trident—are advancing on or ahead of schedule. FERC issued a scheduling order anticipating final certificates by July 31, earlier than expected. Construction on Trident started last week.

Using a forecast of 5.2% annual revenue growth and 28% operating margins, our model projects the stock will rise to $35 within 2.9 years. This assumes a 19x price-to-earnings multiple.

That represents compression from Kinder Morgan’s historical P/E averages of 20.7x (one year) and 17.6x (five years). The lower multiple acknowledges risks around commodity exposure and long project development timelines.

The real value lies in converting the $10 billion backlog into operating assets while capturing additional opportunities in power generation markets.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for KMI stock:

1. Revenue Growth: 5.2%

Kinder Morgan’s growth centers on expanding its natural gas infrastructure. The company’s natural gas business drove the Q4 outperformance, with strength across interstate pipelines, intrastate systems, and gathering assets.

Management expects LNG feed gas demand to grow from 16.6 Bcf/day in 2025 to over 34 Bcf/day by 2030. These volumes flow under long-term, take-or-pay contracts with investment-grade counterparties—providing reliable cash flows for decades.

Beyond LNG, power generation represents a massive opportunity. Management is developing projects to potentially serve more than 10 Bcf/day of natural gas demand from the power sector.

In Georgia alone, utilities project 53 gigawatts of new power demand by the early 2030s, potentially requiring 10 Bcf/day of natural gas supply.

Kinder Morgan serves current natural gas markets with proximity to data center development. Out of the total backlog of $10 Billion, 60% is associated with power projects.

Wood Mackenzie forecasts incremental demand growth of 20 Bcf/day between 2030 and 2035, extending the runway well beyond this decade.

2. Operating margins: 28%

Kinder Morgan maintains industry-leading margins through its fee-based business model. EPS grew at 22% over the past year in Q4, supported by take-or-pay contracts that generate cash flow regardless of commodity prices.

The company generated $5.92 billion in operating cash flow during 2025 while investing $3.15 billion in total capital expenditures. The company spent about $2.6 billion in dividends. This disciplined approach maintains strong margins while funding organic growth.

Management’s $10 billion backlog trades at a multiple below 6x, suggesting these projects will deliver attractive returns as they enter service. About 60% of the backlog supports power generation projects backed by creditworthy utilities.

3. Exit P/E Multiple: 19x

The market values Kinder Morgan at 21.8x earnings today. We assume the P/E will compress modestly to 19x over our forecast period.

Near-term headwinds include exposure to commodity prices and long construction timelines for major infrastructure projects. Q4 saw some softness in the CO2 segment, and product pipelines face demand challenges.

As the project backlog converts to operating assets and natural gas demand growth materializes, Kinder Morgan should command a stable valuation premium. The combination of investment-grade contracts, strategic positioning in high-growth markets, and an improving balance sheet supports this multiple.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Midstream companies face regulatory risks and commodity price volatility. Here’s how Kinder Morgan stock might perform under different scenarios through December 2028:

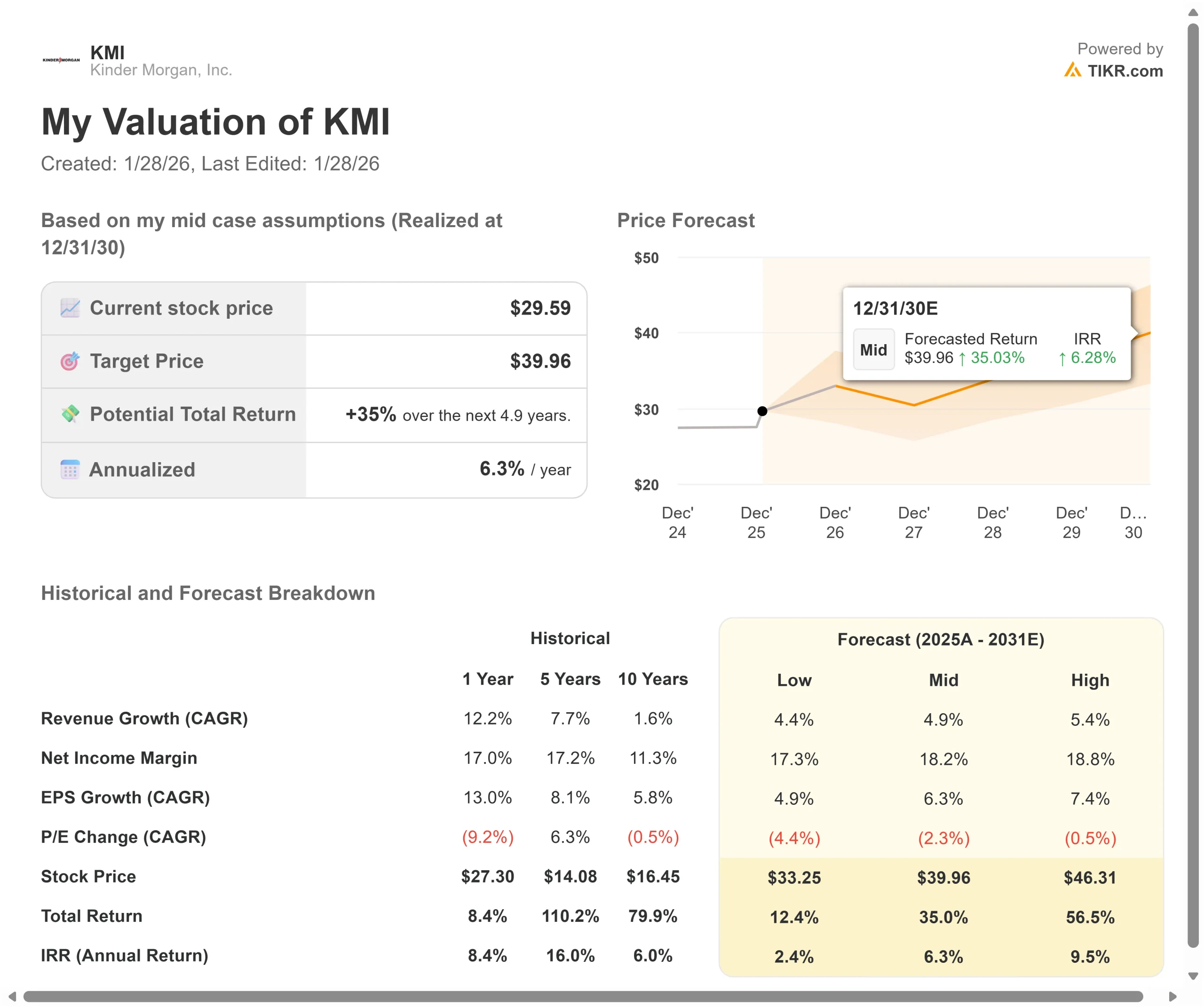

- Low Case: If revenue growth slows to 4.4% and net margins compress to 17.3%, investors still see a 12.4% total return (2.4% annually).

- Mid Case: With 4.9% growth and 18.2% margins, we expect a total return of 35% (6.3% annually).

- High Case: If natural gas demand accelerates and Kinder Morgan maintains 18.8% margins while growing at 5.4%, returns could hit 56.5% total (9.5% annually).

See what analysts think about KMI stock right now (Free with TIKR) >>>

The range reflects execution on major pipeline projects, timing of LNG export growth, and success in capturing power generation opportunities.

In the low case, regulatory delays extend project schedules, or natural gas prices remain depressed, limiting ancillary revenue from storage and transport optimization.

In the high case, LNG exports ramp faster as new facilities come online, power demand from data centers and AI materializes quickly, and projects like Mississippi Crossing enter service ahead of schedule.

Additional upside could come from the Western Gateway Pipeline with Phillips 66 and further expansions on Florida Gas Transmission.

How Much Upside Does Kinder Morgan Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!