Key Takeaways:

- Strategic Turnaround: Ally delivered 62% EPS growth in 2025 while reducing credit risk and strengthening capital.

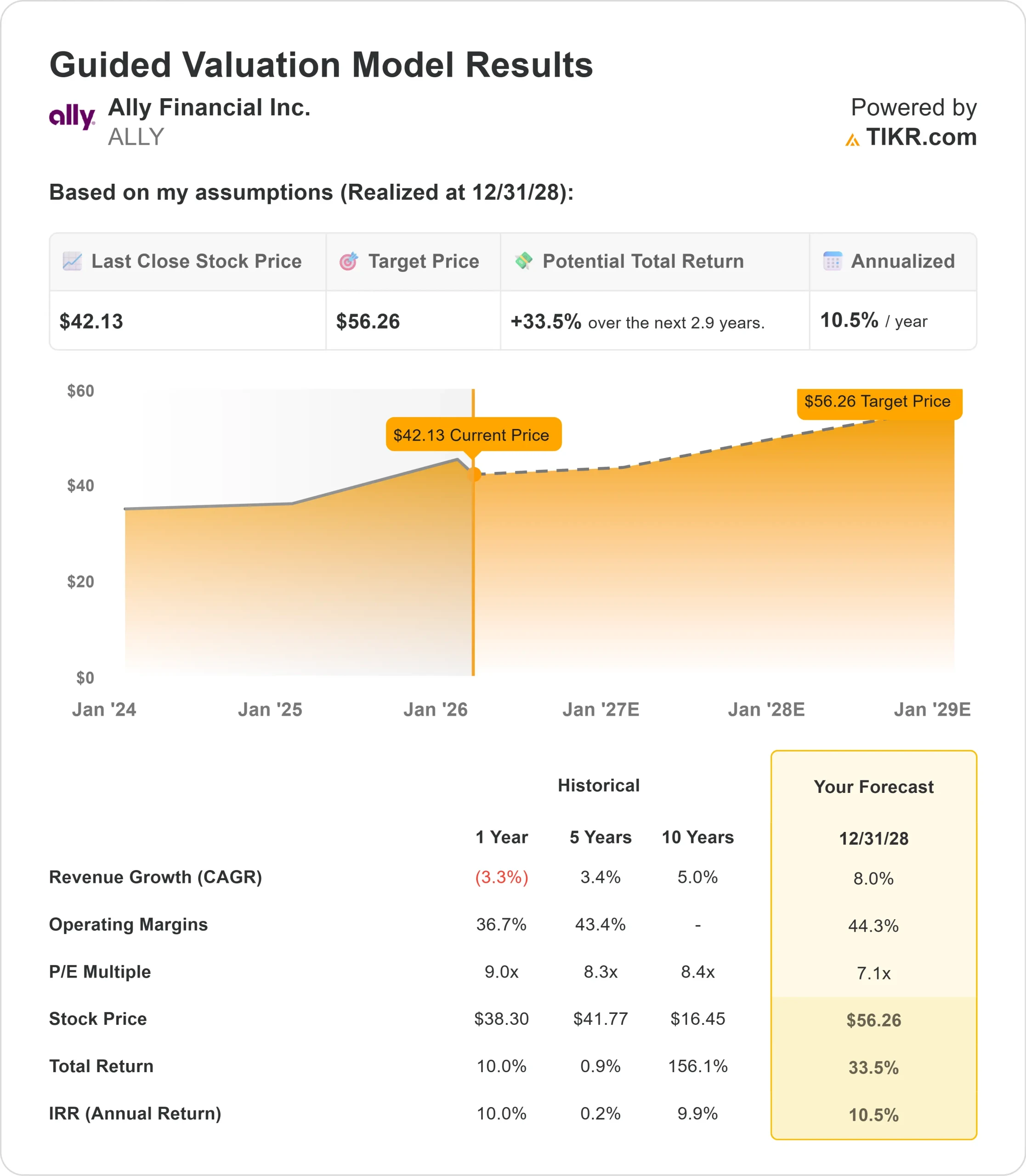

- Price Projection: Based on management guidance, ALLY stock could reach $56 by December 2028.

- Potential Gains: This target implies a total return of 33% from the current price of $42.

- Annual Return: Investors could see roughly 10.5% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Ally Financial (ALLY) is executing a major strategic refresh after weathering a challenging credit cycle.

The digital banking and auto finance company posted adjusted earnings of $3.81 per share for 2025, up 62% year-over-year, while return on core tangible common equity (ROTCE) jumped over 300 basis points to 10.4%.

CEO Michael Rhodes completed his first full year leading the company with deliberate choices that reduced risk and strengthened the balance sheet.

- Ally executed two credit risk transfer transactions totaling $10 billion in retail auto loans, repositioned its investment portfolio to reduce interest rate exposure, and maintained strict expense discipline.

- The company serves 3.5 million digital banking customers with $144 billion in retail deposits, making it the largest all-digital direct bank in the U.S.

- On the lending side, Ally originated $43.7 billion in consumer auto loans while Corporate Finance delivered 28% return on equity with zero charge-offs for the second consecutive year.

Despite this progress and a recent bounce from lows, Ally stock trades at $42, presenting an opportunity for investors who believe in the company’s path to sustained mid-teens returns.

See analysts’ full growth forecasts and estimates for ALLY stock (It’s free) >>>

What the Model Says for Ally Financial Stock

We analyzed Ally’s transformation from a credit-challenged lender into a more disciplined financial services company with improving fundamentals.

- The company is benefiting from vintage rollover dynamics as problematic loans from 2022-2023 age out of the portfolio.

- Management has tightened underwriting standards, with 43% of new auto originations now in the highest credit tier.

- Enhanced servicing strategies are keeping delinquencies in check despite macro uncertainty.

- Ally’s digital bank provides stable, low-cost funding with retail deposits representing nearly 90% of total funding.

- The company serves customers directly without branch overhead, allowing competitive rates while maintaining attractive margins.

Using a forecast of 8% annual revenue growth and 44.3% operating margins, our model projects the stock will rise to $56 within 2.9 years. This assumes a 7.1x price-to-earnings multiple.

That represents compression from Ally’s historical P/E averages of 9x (one year) and 8.3x (five years). The lower multiple acknowledges continued macroeconomic uncertainty around employment and used-vehicle values, as well as execution risk as the company approaches its mid-teens return targets.

The real value lies in expanding net interest margins toward the upper 3% range while keeping retail auto charge-offs below 2%.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ALLY stock:

1. Revenue Growth: 8%

Ally’s growth centers on expanding its core franchises with discipline.

The company saw record application volume of 15.5 million in 2025, a record in itself, allowing selective origination at attractive spreads.

Management expects mid-single-digit growth in both retail auto and Corporate Finance portfolios for 2026.

Net interest margin increased over 30 basis points in 2025 (adjusting for the credit card sale), and management guides toward 3.6-3.7% for 2026, approaching their upper 3% target.

Deposit pricing beta started low following Fed cuts but is expected to catch up through the year, driving margin expansion.

2. Operating margins: 44.3%

Ally is maintaining profitability through cycle management.

The company held controllable expenses flat in 2025 while investing in technology, cybersecurity, and customer experience.

For 2026, management expects expenses to increase by just 1%, demonstrating continued discipline even as it supports growth initiatives.

Operating leverage from revenue growth should drive margin expansion over time as the fixed cost base absorbs higher volumes.

3. Exit P/E Multiple: 7.1x

The market values Ally at roughly 8x earnings currently. We assume modest compression to 7.1x over our forecast period.

Financial stocks face uncertainty from potential changes in the regulatory environment and economic conditions. Ally must specifically navigate labor market weakness and used-vehicle price volatility, which could impact auto credit performance.

However, as management demonstrates consistent execution toward mid-teens returns – requiring upper 3% margins, sub-2% charge-offs, and capital discipline – the company should maintain a reasonable valuation multiple reflecting its improved risk profile.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

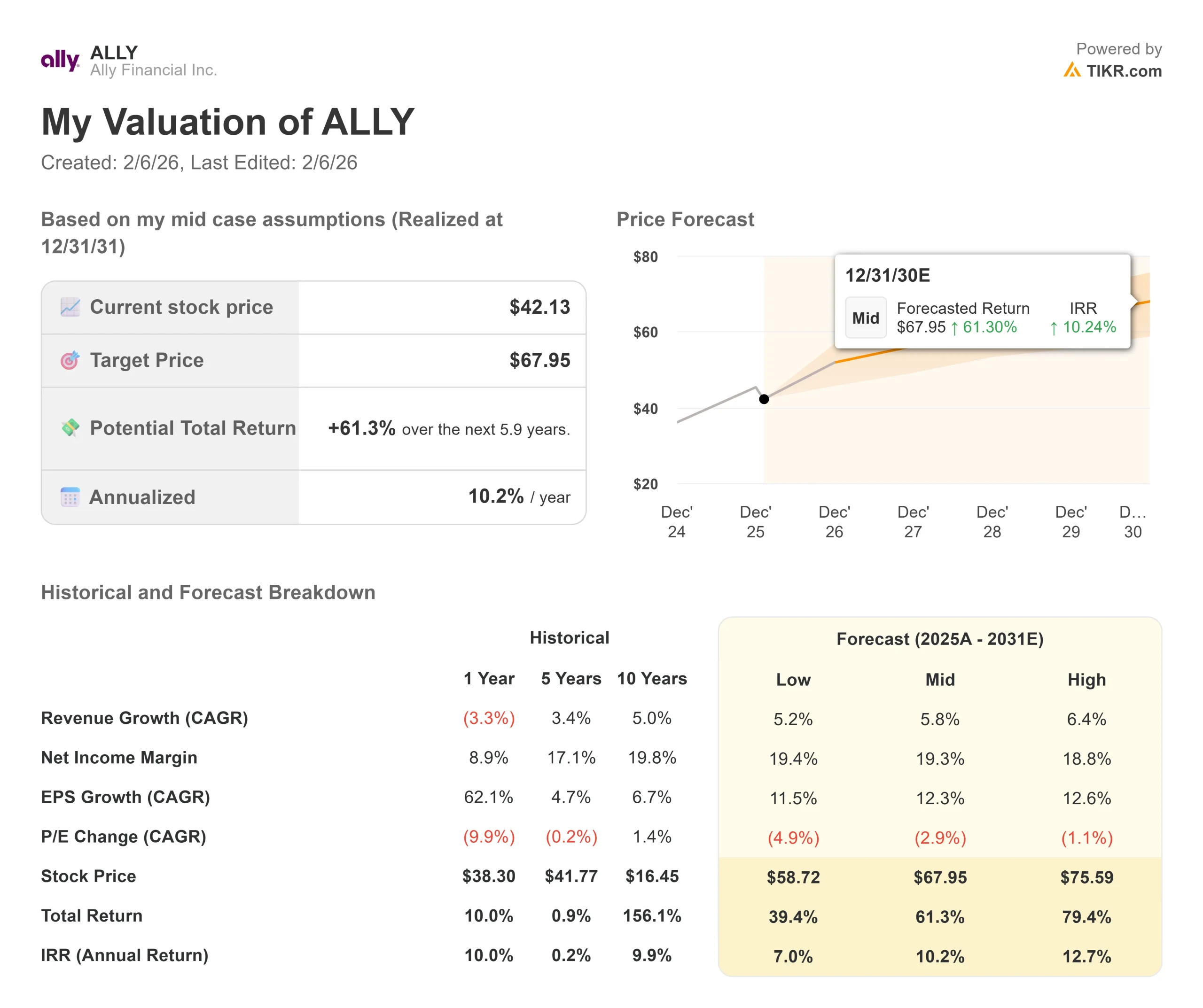

Auto lenders face credit cycles and interest rate sensitivity. Here’s how Ally stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 5.2% and net income margins compress to 19.4%, investors still see a 39% total return (7.0% annually).

- Mid Case: With 5.8% growth and 19.3% margins, we expect a total return of 61% (10.2% annually).

- High Case: If margins expand to 18.8% while growing at 6.4%, returns could hit 79% total (12.7% annually).

See what analysts think about ALLY stock right now (Free with TIKR) >>>

The range reflects execution on credit improvement, margin expansion, and capital deployment, including the recently announced $2 billion share repurchase authorization.

In the worst case, unemployment rises more than expected or used-vehicle values deteriorate, pressuring credit losses.

In the best case, the labor market remains resilient, vintage rollover benefits exceed expectations, and margin expansion accelerates as deposit betas catch up faster than anticipated.

How Much Upside Does Ally Financial Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!