Key Takeaways:

- Local Commerce Expansion: New verticals growing with improving unit economics across grocery, retail, and autonomous delivery.

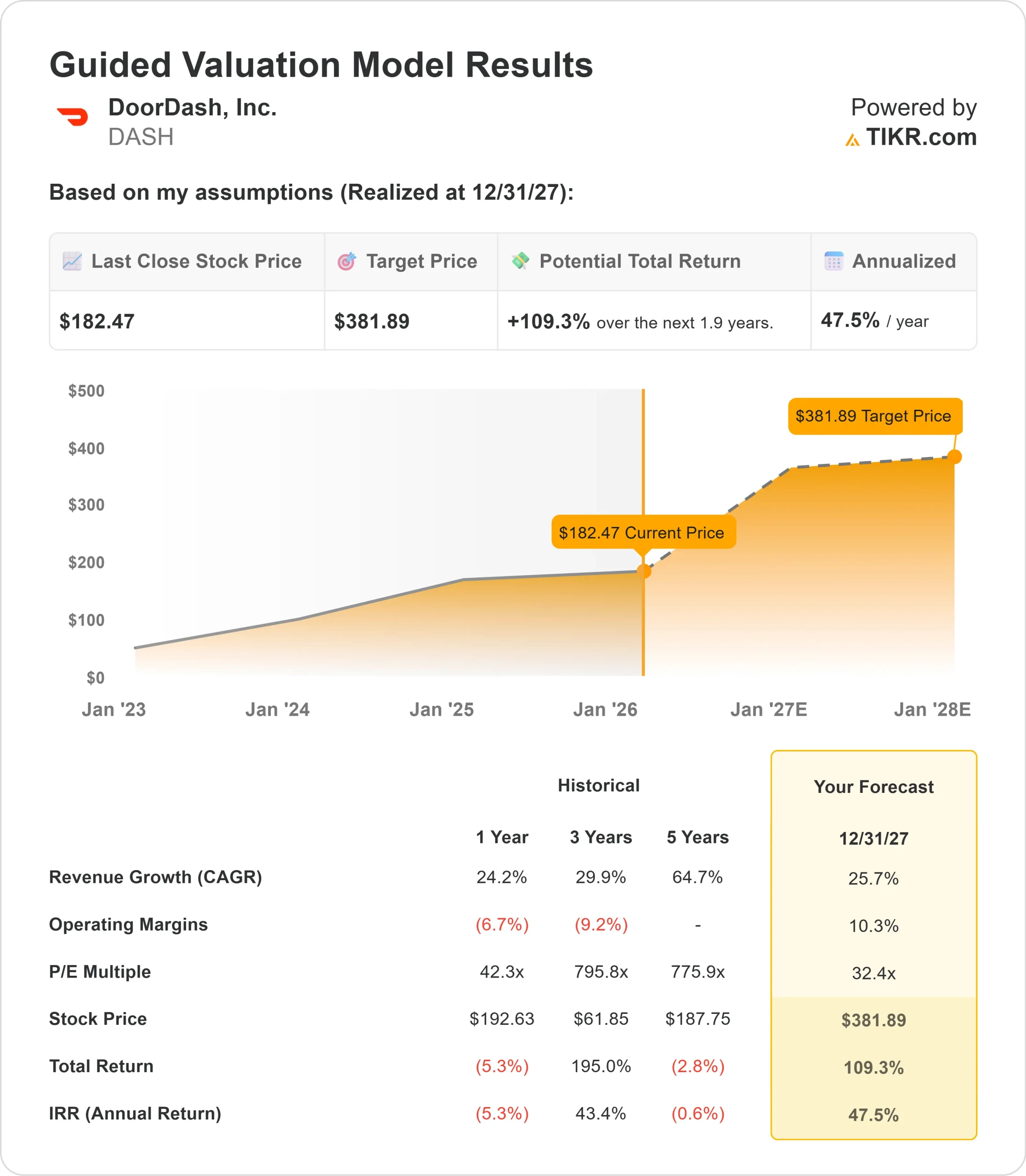

- Price Projection: Based on current execution, DASH stock could reach $382 by December 2027.

- Potential Gains: This target implies a total return of 109% from the current price of $182.

- Annual Return: Investors could see roughly 47.5% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

DoorDash (DASH) recently closed its £2.9 billion acquisition of Deliveroo while posting strong Q3 2025 results.

- The company grew gross order value across all segments, reaching record profitability levels.

- Growth accelerated for the fourth straight quarter as CEO Tony Xu executes an aggressive expansion strategy centered on building a comprehensive local commerce platform.

- The company is investing heavily in 2026 across three major areas: a new global tech platform, autonomous delivery infrastructure, including the DoorDash Dot, and new products like DashMart Fulfillment Services and SevenRooms reservations.

Despite these investments, unit economics continue to improve as the business scales.

DoorDash now operates in over 20 European countries through the Deliveroo acquisition, complementing its existing Wolt business.

The company maintains leadership in U.S. restaurant delivery while rapidly expanding into grocery, retail, and other verticals.

With advertising revenue surpassing $1 billion annually and DashPass membership at record levels, DoorDash is building multiple revenue streams beyond its core delivery business.

See analysts’ full growth forecasts and estimates for DASH stock (It’s free) >>>

What the Model Says for DoorDash Stock

We analyzed DoorDash’s evolution from a restaurant delivery company into a dominant local commerce platform serving multiple categories and geographies.

The company is expanding well beyond restaurant delivery.

- The new verticals business is growing rapidly, with unit economics improving both sequentially and year-over-year.

- DoorDash now leads in order volume share across grocery, convenience, and retail categories.

- This diversification provides resilience while creating opportunities for cross-shopping behavior that increases customer lifetime value.

The autonomous delivery platform represents a major long-term investment. DoorDash is taking a pragmatic, multimodal approach that includes partnerships and proprietary vehicles like the DoorDash Dot.

The company is also building DashMart Fulfillment Services to solve the inventory accuracy problem that has limited grocery delivery penetration.

Using a forecast of 25.7% annual revenue growth and 10.3% operating margins, our model projects the stock will rise to $382 within 1.9 years. This assumes a 32.4x price-to-earnings multiple.

That represents compression from DoorDash’s historical P/E averages of 42.3x (one year) and 795.8x (three years). The lower multiple reflects the company’s transition from hypergrowth to more sustainable expansion while managing significant platform investments.

The real value lies in executing the local commerce vision while maintaining category leadership and improving profitability across all business segments.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DASH stock:

1. Revenue Growth: 25.7%

DoorDash’s growth centers on category expansion and geographic reach.

The U.S. restaurant business is accelerating at larger scale, with growth strengthening for four consecutive quarters.

Monthly active users continue to increase as new customer cohorts are acquired and existing cohorts maintain engagement.

New verticals represent a major growth driver. The business is scaling rapidly with improved unit economics.

Miles driven are up, order frequency is increasing, and basket sizes are growing. Over 25% of DoorDash users now order from new verticals.

The Deliveroo acquisition adds substantial revenue while providing access to large European markets. Management expects the business to grow at double-digit rates while generating $200 million in EBITDA contribution.

International operations through Wolt and Deliveroo now give DoorDash a presence in over 20 countries.

2. Operating margins: 10.3%

DoorDash is investing heavily while improving underlying profitability. The company expects margins for the existing business, excluding Deliveroo, to be up slightly in 2026 despite several hundred million in incremental investments.

These investments span three areas: building a single global tech platform to deliver features simultaneously across all markets, scaling autonomous delivery capabilities, and expanding new products such as in-store dining and fulfillment services.

Management maintains strict discipline around IRR targets and milestone-based funding.

The advertising business provides high-margin revenue that helps fund expansion. Unit economics across all segments continue improving, with the U.S. restaurant business maintaining incremental margins above 7% over the last eight quarters.

3. Exit P/E Multiple: 32.4x

The market values DoorDash at 32.4x current earnings, matching our exit multiple assumption. We expect this valuation to hold as the company demonstrates execution across multiple initiatives.

Near-term integration complexity from Deliveroo and heavy platform investments creates some uncertainty.

The company must successfully combine European operations while maintaining growth momentum. The autonomous delivery program requires substantial upfront spending before generating returns.

However, DoorDash has proven it can manage multiple priorities simultaneously. The track record of improving unit economics while growing faster at scale supports a premium multiple.

The entrepreneurial operating model provides agility to capture emerging opportunities across local commerce.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Local commerce platforms face competitive pressure and execution risks on multiple fronts. Here’s how DoorDash stock might perform under different scenarios through December 2027:

- Low Case: If revenue growth slows to 19.1% and net income margins compress to 31.0%, investors still see a 230.0% total return (35.8% annually).

- Mid Case: With 21.2% growth and 35.1% margins, we expect a total return of 363.6% (48.2% annually).

- High Case: If local commerce adoption accelerates and DoorDash maintains 39.0% margins while growing at 23.3%, total returns could reach 531.9% (60.4% annually).

See what analysts think about DASH stock right now (Free with TIKR) >>>

The range reflects execution on platform investments, category expansion success, and margin improvement as scale benefits emerge.

In the low case, new vertical growth disappoints, or autonomous delivery faces setbacks.

In the high case, DashMart Fulfillment Services unlocks rapid retail expansion and tech platform investments drive faster feature velocity than expected.

How Much Upside Does DoorDash Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!