Key Stats for Intuit Stock

- Year-to-Date Performance: -33%

- 52-Week Range: $411 to $814

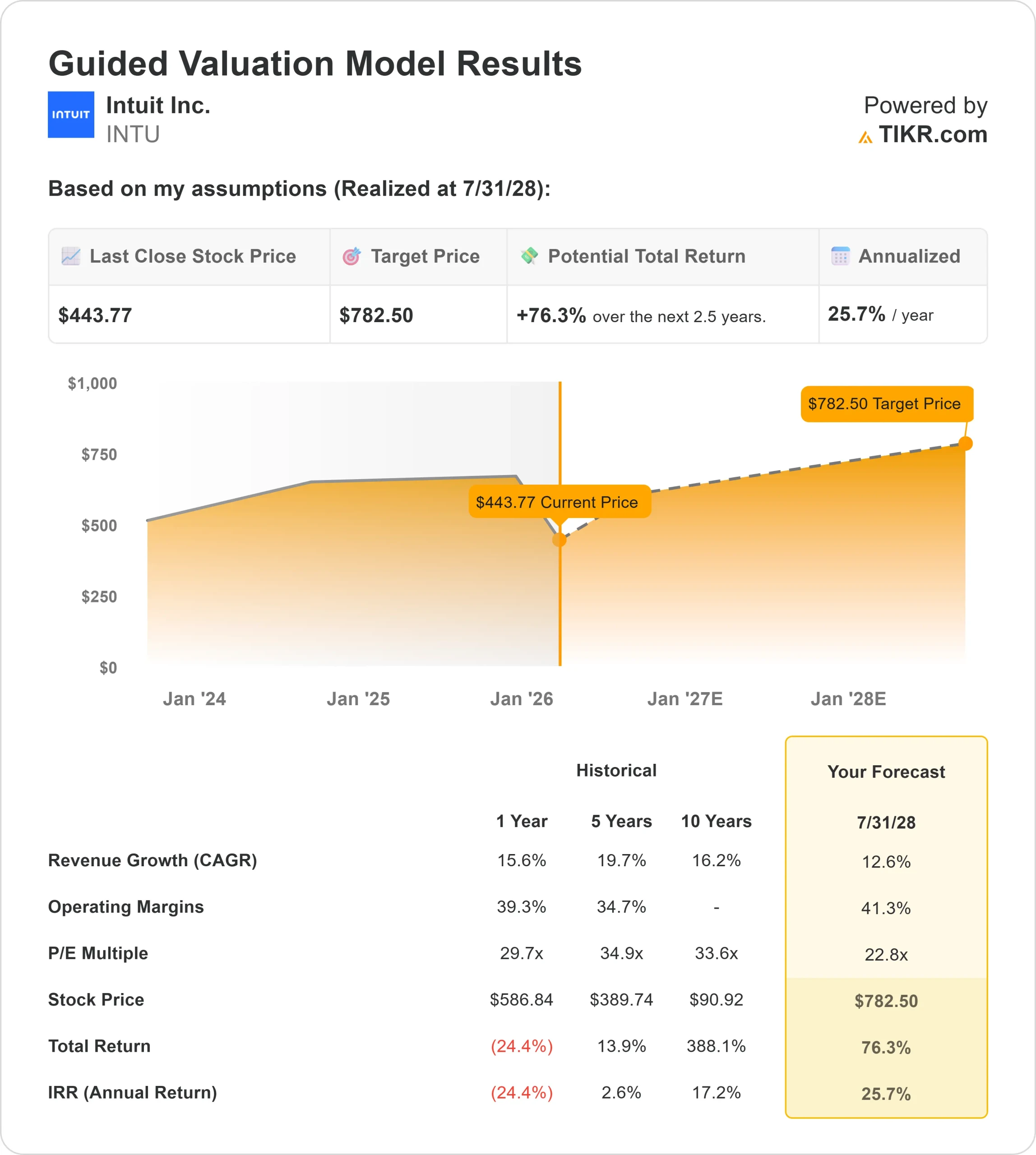

- Valuation Model Target Price: $783

- Implied Upside: 76%

Value your favorite stocks like Intuit with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Intuit Inc. stock shares are down about 33% year to date, trading near $444 per share, as the stock pulled back sharply from prior highs amid broad multiple compression across large-cap software. The decline reflects a reset in valuation expectations rather than a deterioration in Intuit’s underlying business performance.

The stock moved lower as investors rotated away from premium-valued software names while reassessing AI monetization timelines and near-term growth visibility.

Despite the selloff, Intuit’s core tax and small-business software platforms continue to generate recurring revenue with high retention, helping limit downside as expectations adjusted.

Institutional activity added context to the move. Several large holders trimmed exposure during the third quarter, signaling portfolio rebalancing rather than broad capitulation.

Canada Post Corp Registered Pension Plan reduced its stake by 8.5% to 25,432 shares worth about $17.7 million, while Renaissance Group cut its position by 15.6% to 38,282 shares valued at roughly $26.1 million.

Twin Capital Management and Thrivent Financial for Lutherans also trimmed holdings, selling 24.7% and 45.1% of their stakes, respectively.

Those reductions were partially offset by selective accumulation. Bessemer Group increased its stake by 28.4% to 13,253 shares worth about $9.1 million, while Guinness Asset Management trimmed only modestly, reducing its position by 4.6% and retaining 66,284 shares valued at about $46.1 million.

Overall, the activity points to positioning adjustments rather than a loss of confidence in Intuit’s long-term earnings profile, helping explain the year-to-date decline without signaling fundamental stress.

See analysts’ growth forecasts and price targets for Intuit (It’s free) >>>

Is Intuit Undervalued?

Under valuation assumptions, the stock is modeled using:

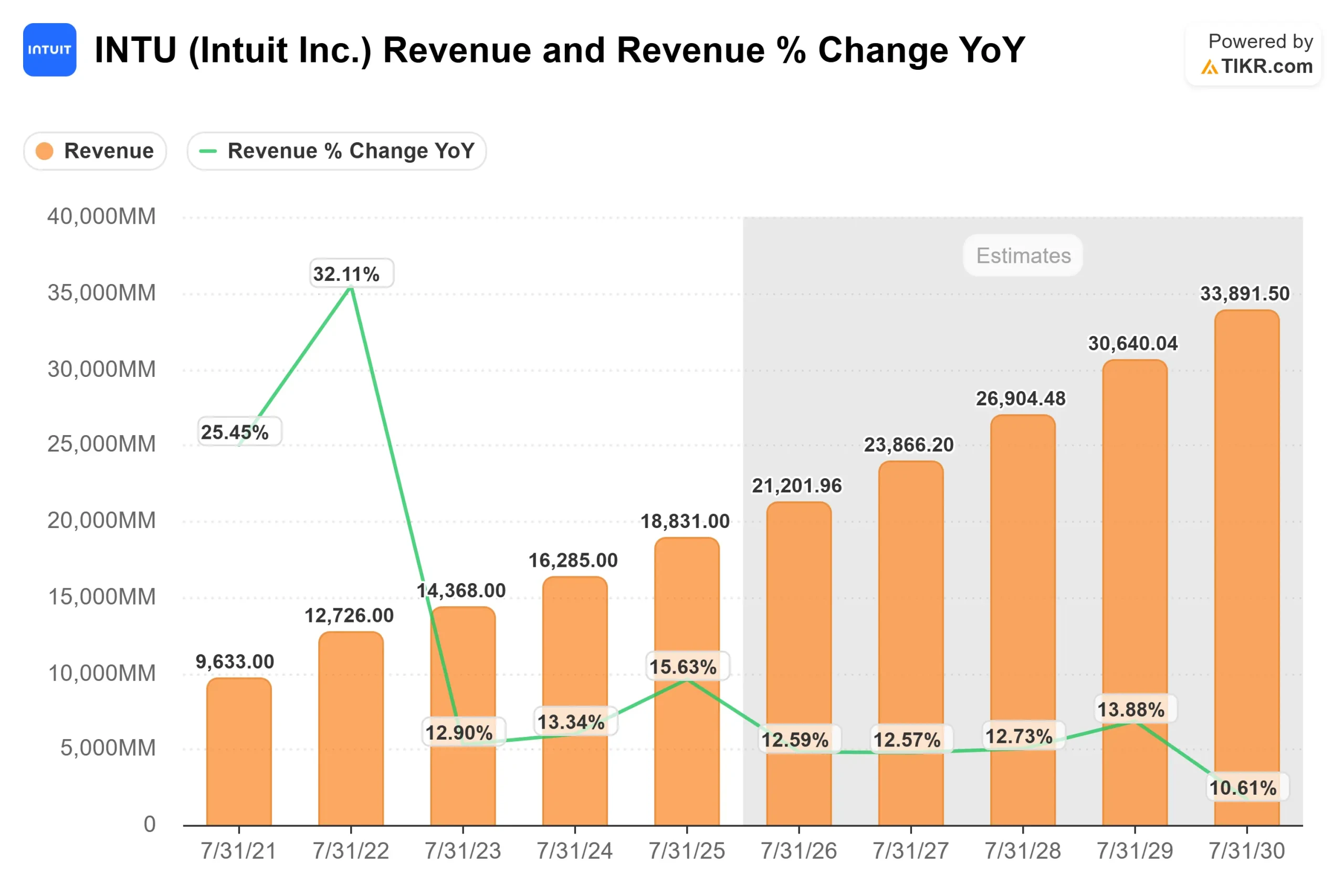

- Revenue Growth (CAGR): 12.6%

- Operating Margins: 41.3%

- Exit P/E Multiple: 22.8x

Revenue growth reflects continued expansion across TurboTax, QuickBooks, and Credit Karma, supported by rising adoption of assisted tax services and deeper monetization across Intuit’s consumer and small-business platforms.

Growth is driven less by new user additions and more by higher-value services, improved conversion, and AI-enabled personalization that increases engagement across the ecosystem.

Margin assumptions remain elevated as Intuit benefits from software-led operating leverage. Management highlighted that AI has shortened tax preparation time by 12%, improved developer productivity by 40%, and unlocked roughly $135 million in efficiency opportunities, supporting margin durability even as the company continues investing in new products and distribution.

Based on these inputs, the valuation model estimates a target price of $783, implying about 76% total upside over roughly 2.5 years, indicating the stock appears undervalued at current prices. That implied return comfortably clears the internal threshold used to flag undervalued opportunities.

Results over the next year hinge on several business drivers. Expansion in the assisted tax market, which includes 88 million potential filers, remains a key growth engine as Intuit moves further upmarket with AI-supported expert services.

Credit Karma’s 43 million monthly active users provide another lever through increased engagement and monetization of loans, financial products, and AI-powered financial assistants.

At the same time, local service expansion, including the rollout of 600 service centers and about 20 retail stores after early pilots produced a fivefold increase in expert engagement, could lift conversion during tax season and deepen customer relationships.

At current levels, Intuit appears undervalued, with future performance driven by platform monetization, AI-driven efficiency gains, and durable demand across its financial software ecosystem rather than multiple expansion alone.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>