Key Takeaways:

- Category Headwinds: Traditional loaf bread segment facing structural shifts as consumers pivot to value and better-for-you options.

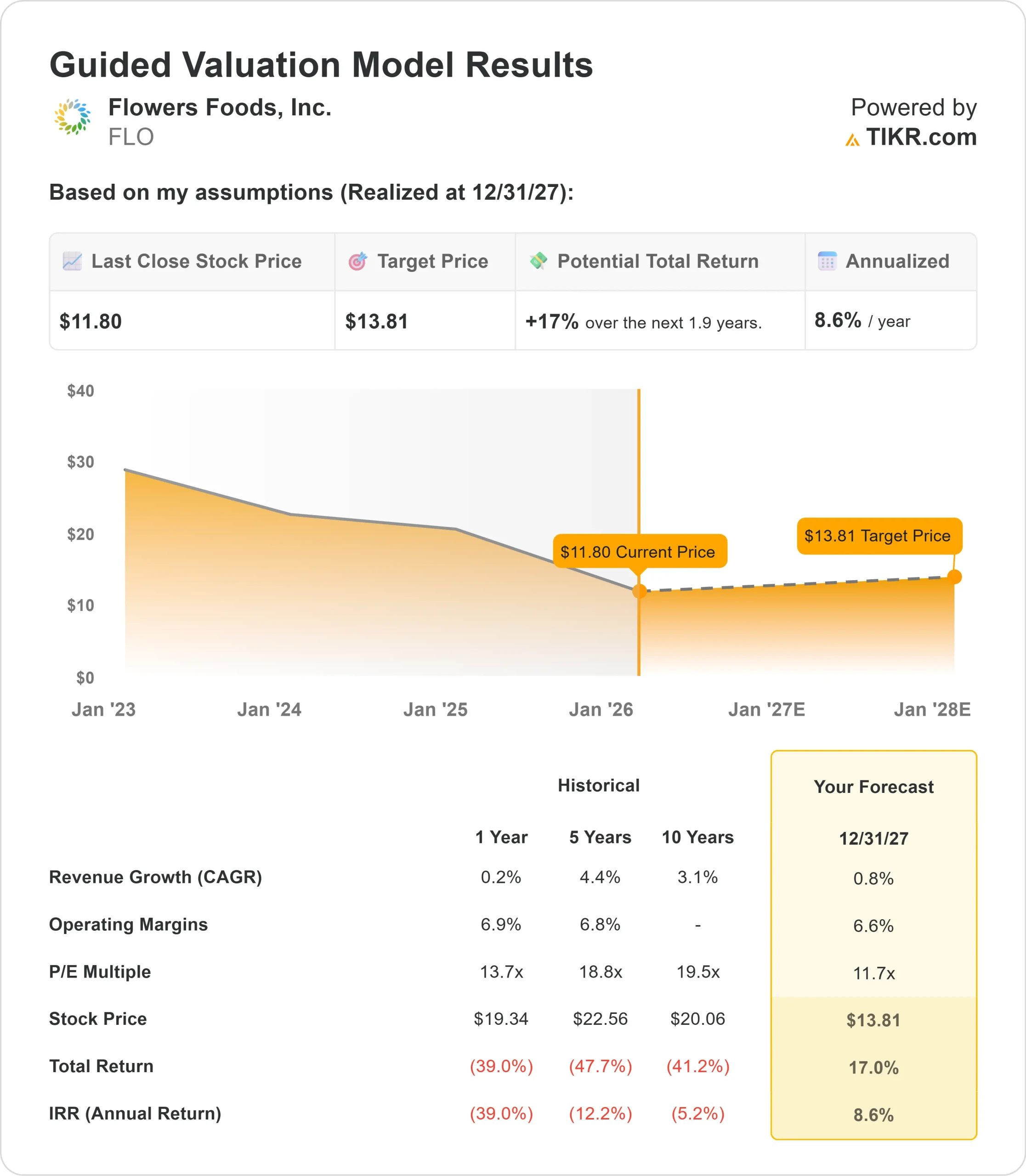

- Price Projection: Based on current execution, FLO stock could reach $13.81 by December 2027.

- Potential Gains: This target implies a total return of 17% from the current price of $11.80.

- Annual Return: Investors could see roughly 8.6% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Flowers Foods (FLO) is navigating one of the most challenging periods in its history as the bread category undergoes a significant transformation.

- The company reported Q3 2025 results showing continued pressure on traditional loaf bread, with CEO Ryals McMullian acknowledging that consumer sentiment reached a low point during the quarter.

- The core issue centers on traditional loaf bread—the 20-ounce soft variety white breads that have long been staples.

- This segment has bifurcated sharply into premium differentiated products or value offerings, leaving traditional loaf “taking it on the chin,” as McMullian described.

- The shift has accelerated over the past 12 to 18 months, creating immediate headwinds for Flowers Foods, given its concentration in this category with the #1 brand and #1 SKU.

- Consumer weakness compounds these structural challenges. Economic uncertainty, tariff concerns, and government disruptions have kept shoppers cautious.

- The foodservice business, which includes QSR and broad-line distribution, has experienced notable pressure reflecting weak traffic trends across the restaurant industry.

- Despite near-term struggles, Flowers Foods is executing a strategic pivot to redefine traditional loaf by incorporating value and better-for-you attributes aligned with evolving preferences.

The company’s portfolio demonstrates that this shift is gaining traction. Canyon Bakehouse posted 6% unit growth in Q3, while Dave’s Killer Bread surged 10%. The company’s entry into small loaf bread captured 15 full points of unit share, placing Nature’s Own at #2 in a category growing 85%.

The Simple Mills acquisition continues performing in line with expectations, with strong collaboration between teams yielding opportunities in customer engagement and procurement.

Management expressed enthusiasm about the upcoming 2026 innovation, though the acquisition currently pressures margins due to its 100% co-manufacturing model.

Flowers Foods faces margin challenges in the near term. Gross margin declined 190 basis points in Q3, driven by negative price mix, lower volumes, and Simple Mills’ higher-cost structure.

The company also converted independent distributors to company employees in California, increasing SG&A expenses.

New product innovation naturally pressures margins initially before scale and targeted capital investments improve efficiency.

Management is focused on returning to normalized leverage ratios, reducing CapEx based on project cadence, and reassessing investments to ensure optimal returns.

The company maintains 44 bakeries following years of consolidation, with further supply chain optimization opportunities under evaluation.

See analysts’ full growth forecasts and estimates for FLO stock (It’s free) >>>

What the Model Says for Flowers Foods Stock

We analyzed Flowers Foods as it navigates a category transformation and repositions its portfolio for long-term growth. The company’s strong brand equity with Nature’s Own, Wonder, and Dave’s Killer Bread provides a foundation, but execution against structural headwinds remains critical.

Using a forecast of 0.8% annual revenue growth and 6.6% operating margins, our model projects the stock will rise to $13.81 within 1.9 years. This assumes an 11.7x price-to-earnings multiple.

That represents compression from Flowers Foods’ historical P/E averages of 13.7x (one year) and 18.8x (five years).

The lower multiple reflects ongoing category weakness, margin pressure from innovation and Simple Mills integration, and uncertainty around when traditional loaf stabilizes.

The real value lies in successfully repositioning the portfolio toward faster-growing segments while maintaining operational efficiency during the transition.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for FLO stock:

1. Revenue Growth: 0.8%

Growth expectations remain muted, reflecting category dynamics.

Management expects weakness to continue for part of 2026 as economic uncertainty persists. The company is focusing on innovation-driven growth in premium segments such as Canyon Bakehouse, Dave’s Killer Bread, and small-loaf formats, which command higher prices but represent smaller absolute volumes than traditional-loaf declines.

2. Operating margins: 6.6%

Margins face near-term pressure from multiple factors. New product launches create complexity in bakeries accustomed to long runs of established items.

Simple Mills operates on a co-manufacturing model, which inherently yields lower margins. The company expects input cost inflation to continue, particularly for wheat.

However, management has a track record of bringing acquired businesses up to the company’s average margins over time.

3. Exit P/E Multiple: 11.7x

The market currently values Flowers Foods at 12.1x earnings.

We assume modest compression to 11.7x over our forecast period, given integration complexity, category transformation risks, and margin pressures.

As traditional loaf stabilizes and innovation gains scale, the company should command a premium to this level, but timing remains uncertain.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

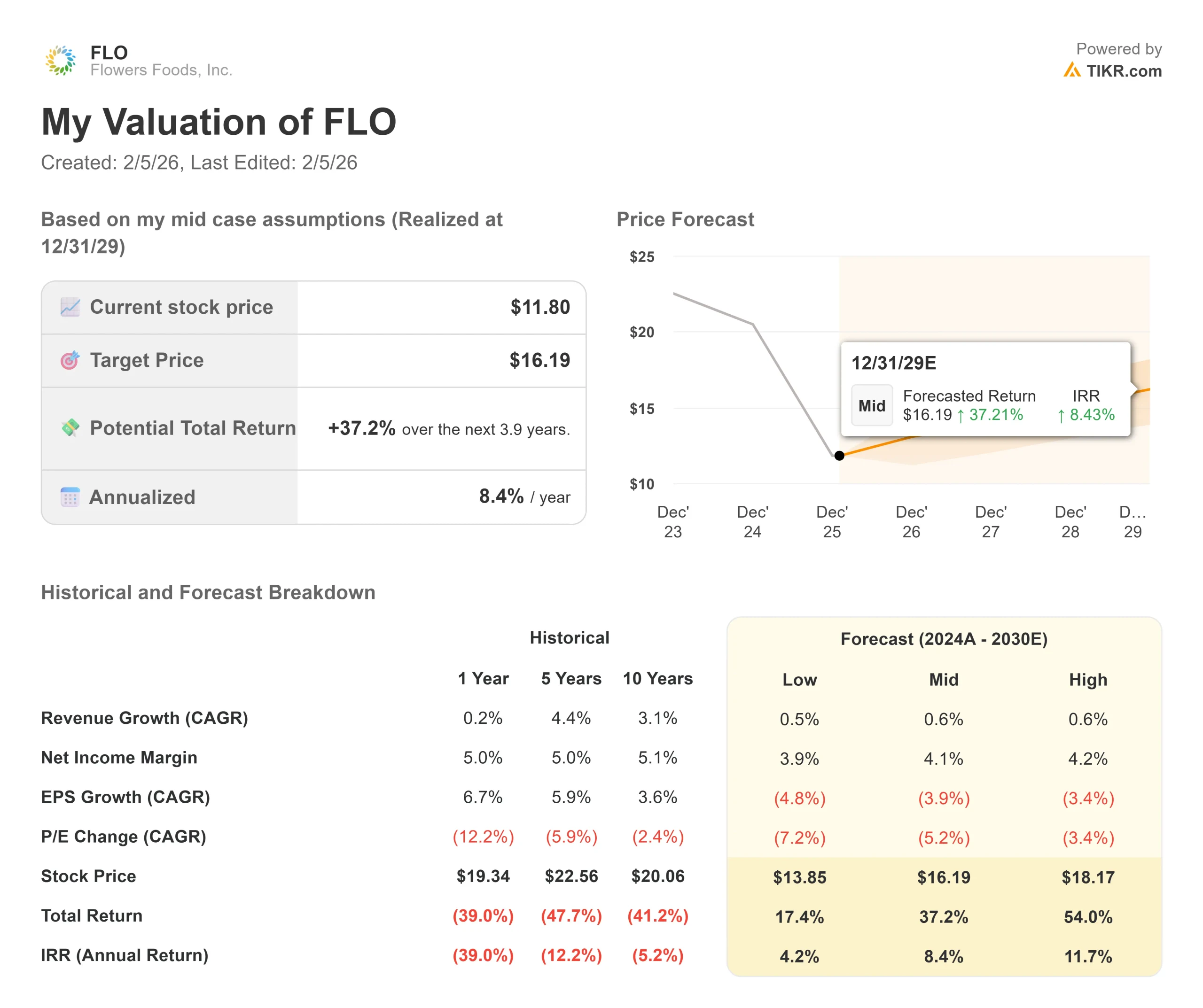

Food companies face shifts in consumer preferences and economic cycles. Here’s how Flowers Foods stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth stays at 0.5% and net income margins compress to 3.9%, investors still see a 17.4% total return (4.2% annually).

- Mid Case: With 0.6% growth and 4.1% margins, we expect a total return of 37.2% (8.4% annually).

- High Case: If innovation accelerates and Flowers Foods maintains 4.2% margins while growing at 0.6%, total returns could reach 54.0% (11.7% annually).

See what analysts think about FLO stock right now (Free with TIKR) >>>

The range reflects successful portfolio repositioning, category stabilization timing, and margin expansion as innovation scales and Simple Mills integration progress.

How Much Upside Does Flowers Foods Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!