Key Takeaways:

- Leadership Shakeup: New executive leadership following internal investigation into sales practices.

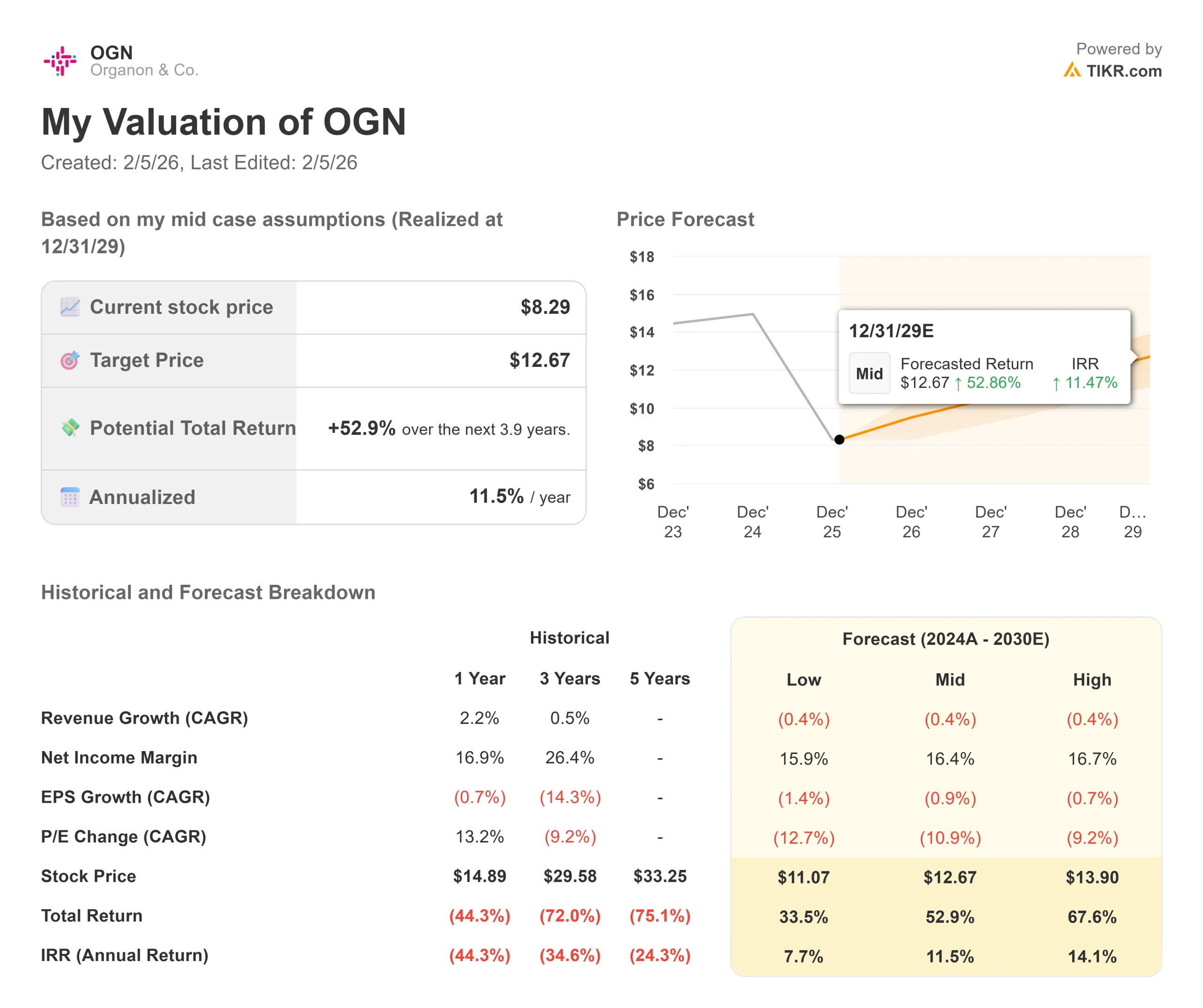

- Price Projection: Based on current fundamentals, OGN stock could reach $12.67 by December 2029.

- Potential Gains: This target implies a total return of 53% from the current price of $8.29.

- Annual Return: Investors could see roughly 11.5% growth over the next 3.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Organon & Co. (OGN) is navigating turbulent waters. The women’s health specialist recently announced leadership changes following an internal investigation into Nexplanon sales practices and simultaneously divested its Jada system for $465 million to accelerate debt reduction.

The company posted Q3 revenue of $1.6 billion with a 32.3% adjusted EBITDA margin.

Despite challenges, including U.S. policy headwinds affecting contraceptive sales and weakness in its respiratory portfolio, Organon maintains diverse exposure across Women’s Health, biosimilars, and established brands serving patients in many countries.

Management expects 2025 revenue between $6.2 billion and $6.25 billion, representing a 2-3% decline year-over-year.

The company is prioritizing debt reduction, with net leverage at 4.2x, while investing behind growth drivers like Vtama, Hadlima, and international Nexplanon expansion.

Despite recent setbacks, Organon stock trades at $8.29, potentially offering upside for investors willing to look past near-term headwinds.

See analysts’ full growth forecasts and estimates for OGN stock (It’s free) >>>

What the Model Says for Organon Stock

We analyzed Organon through its position as a diversified women’s health and biosimilars company facing both operational challenges and strategic opportunities.

- The company’s Nexplanon franchise, while facing U.S. policy headwinds, remains a global contraceptive leader.

- Management expects international Nexplanon growth to offset domestic weakness, with global revenues projected to be flat in 2026.

- Meanwhile, the biosimilars business continues gaining momentum, with Hadlima up 63% year-to-date and new launches, including a denosumab biosimilar, adding growth vectors.

- The Jada divestiture will reduce debt by over $400 million, improving financial flexibility while allowing management to focus resources on core franchises.

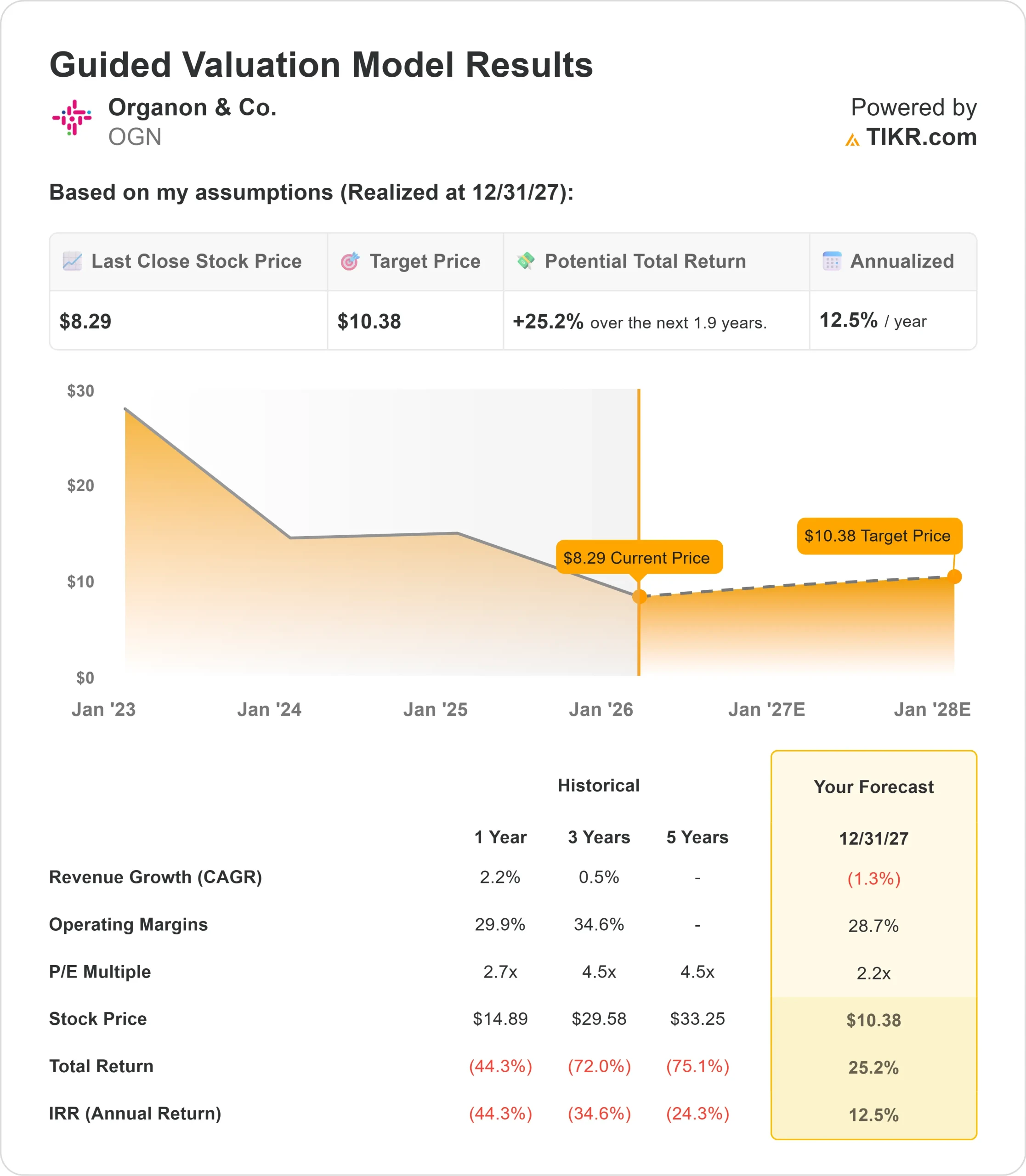

Using a forecast of 1.3% annual revenue contraction and 28.7% operating margins, our model projects the stock will rise to $10.38 within 1.9 years. This assumes a 2.2x price-to-earnings multiple at exit.

That represents significant compression from Organon’s historical P/E averages of 2.6x (one year) and 4.5x (three years).

The conservative multiple reflects integration risks from recent turmoil, persistent respiratory weakness, and an uncertain contraceptive policy landscape.

The real value lies in stabilizing the revenue trajectory while maintaining industry-leading EBITDA margins and successfully deleveraging the balance sheet.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for OGN stock:

1. Revenue Growth: -0.4%

Organon faces modest revenue headwinds going forward. The company expects 2026 revenue to be approximately flat on a pro forma basis after the Jada divestiture, with growth products such as Vtama, Emgality, and biosimilars offsetting continued respiratory softness.

The respiratory portfolio faces structural challenges as older products such as Singulair lose market share to newer molecules, particularly in pediatrics, while mandatory price reductions in China and Japan compound pressure. Management acknowledges this erosion will persist in the near-term

For Nexplanon, U.S. policy headwinds affecting Title X funding and Planned Parenthood access have disproportionately impacted the product’s core market. While international growth continues at mid-to-high single-digit rates, domestic weakness is weighing on results.

The upcoming five-year indication may boost the addressable population but reduce reimplantation frequency.

2. Operating margins: 28.7%

Organon has demonstrated margin resilience despite revenue challenges. The company delivered 32.3% adjusted EBITDA margin in Q3, though full-year guidance points to approximately 31% as increased SG&A investments support Vtama and Tofidence launches.

Management continues to execute on $200 million in operating expense savings and plans a supply chain separation from Merck, which should drive gross margin expansion beginning in 2027.

However, near-term mix headwinds from respiratory weakness and continued commercial investments moderate the margin trajectory.

The company’s diverse geographic footprint and established brands infrastructure provide operating leverage, though we model modest margin compression as growth investments offset efficiency gains.

3. Exit P/E Multiple: 2.2x

The market currently values Organon at 2.2x earnings. We assume the P/E remains stable at 2.2x through our forecast period.

Recent governance issues and leadership transition create near-term uncertainty. The Board has initiated a CEO search while installing interim leadership to oversee remediation efforts, including enhanced controls and personnel changes.

As the company demonstrates operational stability, reduces leverage to below 4x, and makes progress on Women’s Health business development, investor confidence should improve.

The entrepreneurial model with decentralized commercial operations provides agility, though execution remains paramount given recent challenges.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Pharmaceutical companies with diversified portfolios face varying market dynamics across franchises. Here’s how Organon stock might perform under different scenarios through December 2029:

- Low Case: If revenue contracts 0.4% annually and net income margins compress to 15.9%, investors could see a 33.5% total return (7.7% annually).

- Mid Case: With 0.4% revenue decline and 16.4% margins, we expect a total return of 52.9% (11.5% annually).

- High Case: If revenue stabilizes at-0.4% while the company achieves 16.7% margins, total returns could reach 67.6% (14.1% annually).

See what analysts think about OGN stock right now (Free with TIKR) >>>

The range reflects execution on biosimilars growth, successful debt reduction, and stabilization of Women’s Health revenues despite policy headwinds.

In the low case, respiratory erosion accelerates, or Nexplanon faces worsening U.S. access barriers.

In the high case, Vtama adoption has a meaningful impact; biosimilars gain market share faster than expected, and management successfully navigates the leadership transition while delivering margin expansion ahead of schedule.

How Much Upside Does Organon Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!