Key Takeaways:

- Talent Solutions Recovery: First positive sequential growth in over 3 years, with weekly trends showing momentum.

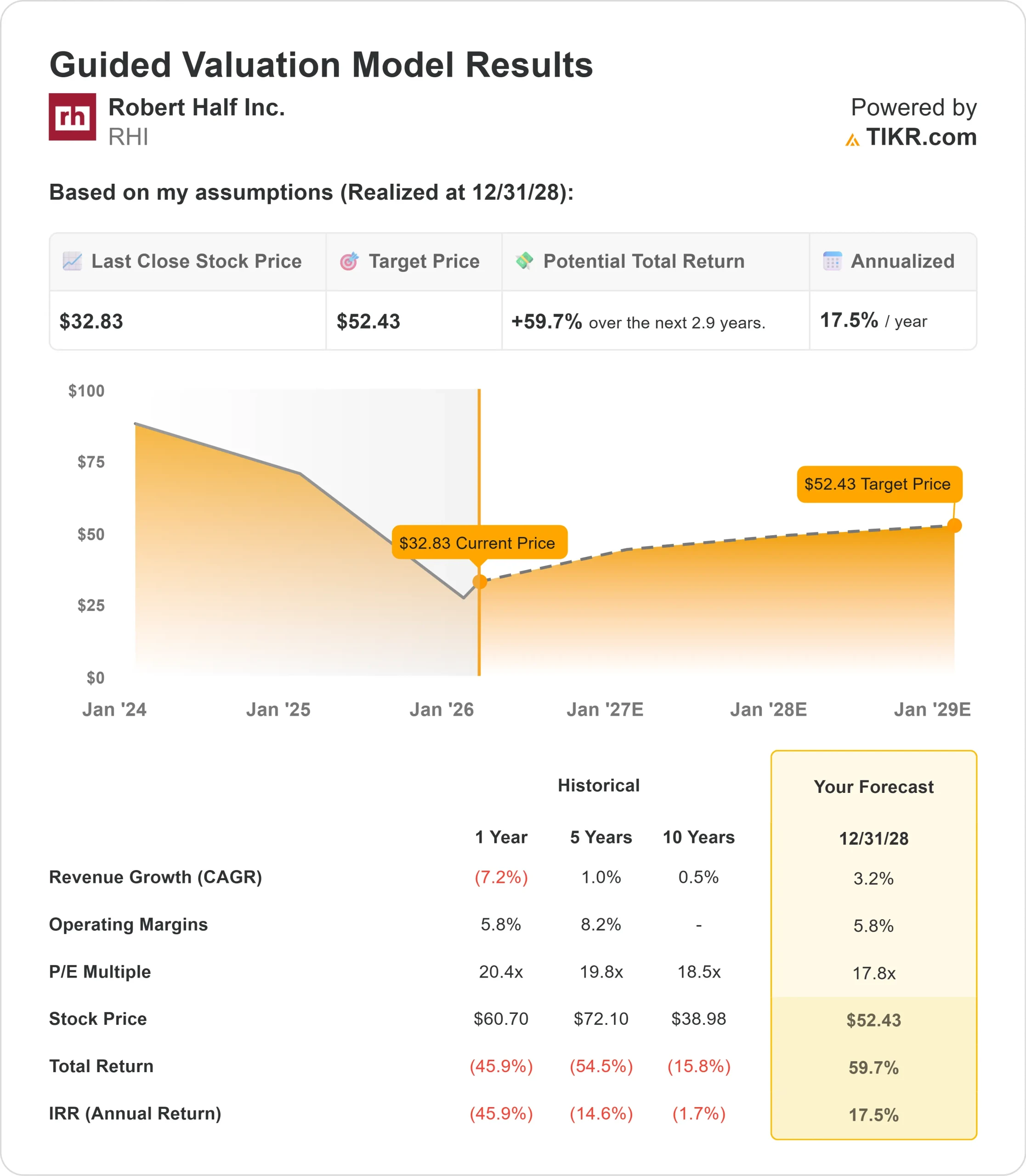

- Price Projection: Based on current execution, RHI stock could reach $52 by December 2028.

- Potential Gains: This target implies a total return of 60% from the current price of $33.

- Annual Return: Investors could see roughly 17.5% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Robert Half Inc. (RHI) just posted its first sequential revenue growth in over three years while navigating one of the staffing industry’s most challenging periods.

The company generated $1.302 billion in Q4 revenue, down 7% year over year, but CEO Keith Waddell sees clear signs of recovery ahead.

Weekly revenue trends during the quarter showed positive momentum that extended into January. The company earned $0.32 per share compared to $0.53 a year ago, while generating $183 million in operating cash flow—the highest quarter of 2025 and an 18% increase over Q4 2024.

Despite headwinds from a cautious hiring environment, Robert Half trades at $33, offering meaningful upside for investors who recognize the company’s positioning as economic uncertainty begins to ease.

See analysts’ full growth forecasts and estimates for RHI stock (It’s free) >>>

What the Model Says for Robert Half Stock

We analyzed Robert Half’s transformation during an extended staffing downturn while maintaining its industry-leading talent and consulting capabilities.

The company weathered nearly four years of declining revenues by retaining its top producers and maintaining capacity for the recovery.

With 7,400 internal employees in talent solutions (down just 3.2% from the prior year) and 11,200 at Protiviti (up 1.5% from the prior year), Robert Half has 15-30% unused capacity based on various metrics.

Management expects to return to positive year-over-year revenue growth by Q3 2026 if current weekly trends continue.

Small and mid-sized businesses—Robert Half’s core market—remain particularly lean after years of cost containment, creating pent-up demand for both permanent placements and contract talent.

Using a forecast of 3.2% annual revenue growth and 5.8% operating margins, our model projects the stock will rise to $52 within 2.9 years. This assumes a 17.8x price-to-earnings multiple.

That represents compression from Robert Half’s historical P/E averages of 20.4x (one year) and 19.8x (five years). The lower multiple acknowledges near-term margin pressure as the company navigates the recovery and adjusts to a more competitive environment.

The real value lies in Robert Half’s ability to leverage its retained talent base as demand accelerates while Protiviti expands its technology consulting practice.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for RHI stock:

1. Revenue Growth: 3.2%

Robert Half’s growth centers on capturing pent-up SMB hiring demand as uncertainty declines.

- The company achieved its first positive sequential growth (same-day, constant-currency basis) in over three years in Q4.

- Contract talent solutions revenues were down 6.6% in early January, compared to 8.9% in December, indicating improving trends.

- Permanent placement revenues declined 9.4% in January versus 11% in December.

- Decision timelines are shortening, and client engagement is increasing as companies revisit postponed hiring initiatives.

The NFIB Small Business Optimism Index has trended higher while the Uncertainty Index fell to its lowest level since June 2024. SMB clients added just 1.1% annually to headcount between January 2022 and December 2025, well below the 2.8% rate at larger companies.

Protiviti reported 3% lower year-over-year revenue but is seeing strong demand for technology consulting, particularly for platform modernization projects.

Management expects Protiviti to add 100-200 basis points to gross and operating margins during 2026.

2. Operating margins: 5.8%

Robert Half expects to retrace on the upside the margin compression experienced during the downturn.

The company delivered an adjusted operating margin of 3.3% in Q4, down from more normalized levels as revenue declined. Talent solutions posted just 1.1% adjusted operating margins while Protiviti maintained 7.1% despite revenue headwinds.

Management has maintained capacity throughout the downturn, particularly in field management and corporate services.

This creates operating leverage as revenues return to growth. With minimal need to add headcount initially, incremental margins should improve meaningfully as utilization increases.

The company’s use of AI for candidate matching and prospect prioritization provides additional efficiency gains.

3. Exit P/E Multiple: 17.8x

The market values Robert Half at 21.9x trailing earnings. We assume the P/E will compress to 17.8x over our forecast period.

Near-term uncertainty around the pace of recovery and competitive dynamics weighs on the multiple. The company must demonstrate sustained sequential growth while expanding margins from cyclically depressed levels.

As hiring activity normalizes and Robert Half captures market-share gains through its technology investments and consultative approach, the company should command a premium over its long-term average.

The combination of staffing and Protiviti consulting creates a unique value proposition as AI makes candidate vetting more critical.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

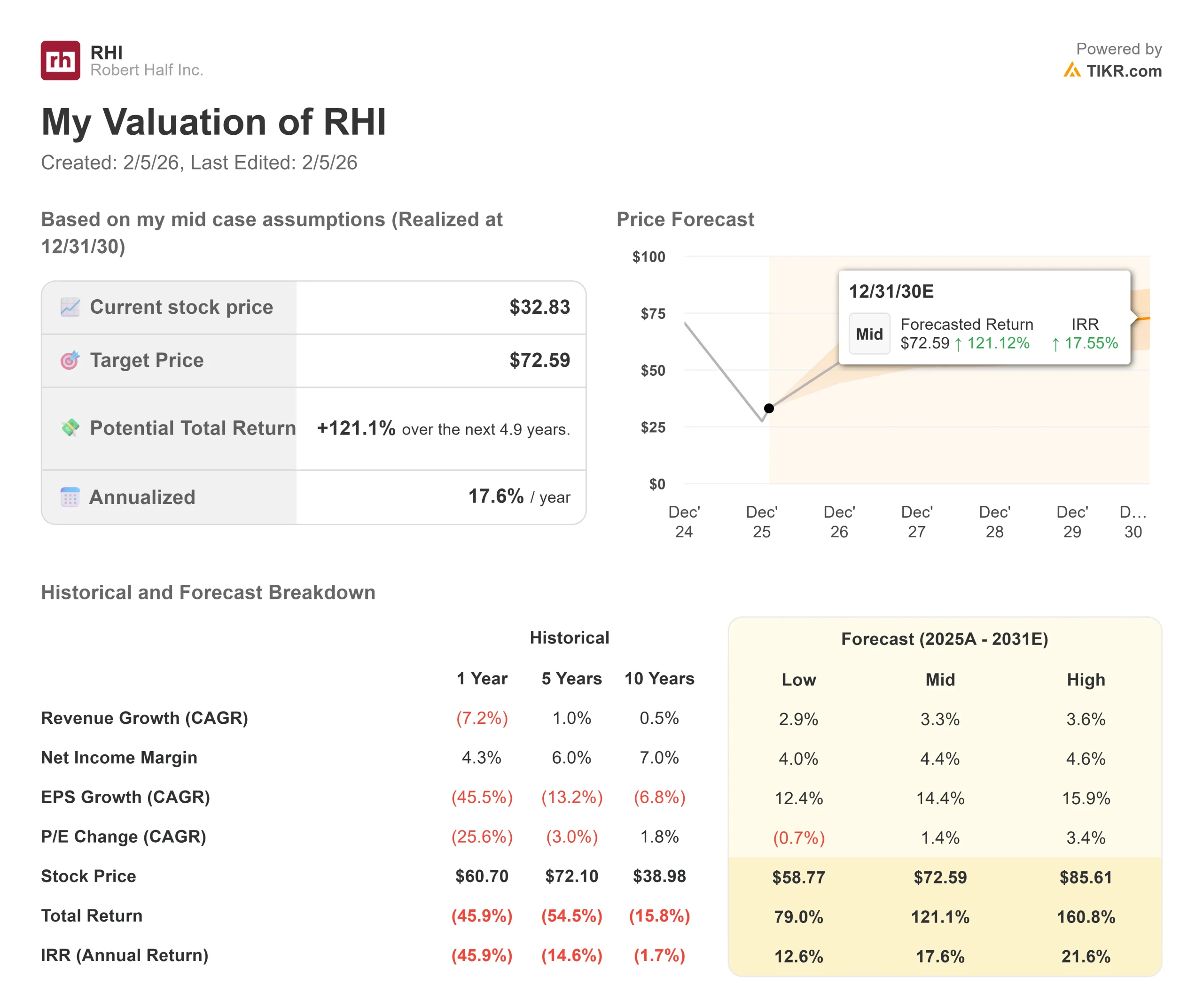

Staffing companies face economic sensitivity and competitive pressures. Here’s how Robert Half stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 2.9% and net income margins compress to 4.0%, investors still see a 79% total return (12.6% annually).

- Mid Case: With 3.3% growth and 4.4% margins, we expect a total return of 121% (17.6% annually).

- High Case: If SMB hiring accelerates and Robert Half maintains 4.6% margins while growing at 3.6%, returns could hit 161% total (21.6% annually).

See what analysts think about RHI stock right now (Free with TIKR) >>>

The range reflects execution on capturing pent-up SMB demand, successful margin expansion as Protiviti scales technology consulting, and the company’s ability to leverage retained capacity without significant headcount additions.

In the low case, economic uncertainty persists, or AI disruption proves more immediate than expected.

In the high case, SMB hiring rebounds faster than anticipated, Protiviti’s tech consulting momentum exceeds expectations, and operating leverage delivers stronger-than-expected margin expansion.

How Much Upside Does Robert Half Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!