Key Takeaways:

- Platform Expansion: 14% recurring revenue growth driven by new finance and IT offerings alongside core HCM.

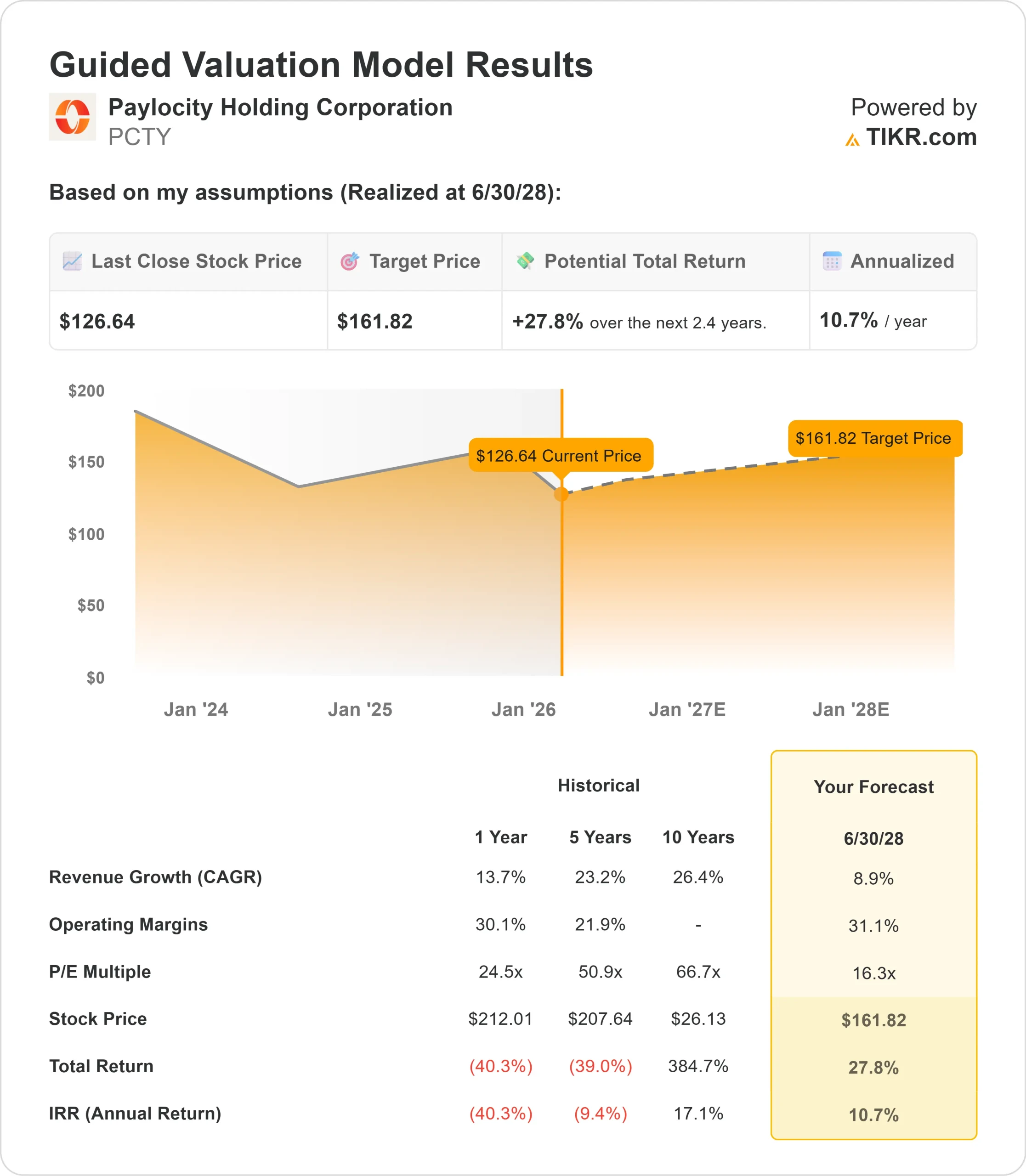

- Price Projection: Based on current execution, PCTY stock could reach $162 by June 2028.

- Potential Gains: This target implies a total return of 28% from the current price of $127.

- Annual Return: Investors could see roughly 11% growth over the next 2.4 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Paylocity Holding Corporation (PCTY) just wrapped up a strong first quarter of fiscal 2026 with recurring revenue up 14% and total revenue reaching $408 million.

The company closed its largest acquisition to date, Airbase, while expanding beyond traditional HCM software into the CFO’s office and IT departments.

CEO Toby Williams is executing an aggressive platform expansion strategy centered on AI-powered workflows.

The company increased its long-term revenue target from $2 billion to $3 billion while raising profitability expectations.

Adjusted EBITDA margin hit 35.9% in Q1, and management projects reaching 40-45% EBITDA margins long-term.

Despite strong momentum, Paylocity stock trades around $127, down significantly from its highs, offering upside for investors who recognize the company’s position in modern workforce software.

See analysts’ full growth forecasts and estimates for PCTY stock (It’s free) >>>

What the Model Says for Paylocity Stock

We analyzed Paylocity’s transformation from a pure HCM provider to a comprehensive platform spanning HR, finance, and IT.

The company is expanding beyond payroll and benefits administration.

- The Airbase acquisition adds spend management and financial workflows, creating an integrated platform for customers to manage employees and business operations.

- With AI embedded throughout, Paylocity is capturing wallet share as organizations consolidate vendors.

- The company serves mid-market businesses, maintaining strong broker relationships that deliver over 25% of new business.

- This distribution advantage provides resilience while platform expansion creates unprecedented cross-sell opportunities.

Using a forecast of 8.9% annual revenue growth and 31.1% operating margins, our model projects the stock will rise to $162 within 2.4 years. This assumes a 16.3x price-to-earnings multiple.

That represents compression from Paylocity’s historical P/E averages of 24.5x (one year) and 50.9x (five years).

The lower multiple acknowledges integration risks from the Airbase acquisition and potential moderation in software spending.

The real value lies in sustaining the platform expansion while maintaining industry-leading service levels and broker relationships.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PCTY stock:

1. Revenue Growth: 8.9%

Paylocity’s growth centers on platform expansion beyond HCM. The company achieved 14% organic growth in recurring revenue for Q1, driven by strong demand for both core HCM and new finance offerings. Management expects momentum to continue as Paylocity for Finance gains traction.

The Airbase acquisition adds spend management capabilities that management says are seeing strong early adoption.

Beyond finance and IT, the company maintains a massive runway in core HCM with relatively low penetration in its target market of mid-sized businesses.

2. Operating margins: 31.1%

Paylocity is sustaining strong profitability while investing in product development.

The company delivered 35.9% adjusted EBIDTA margin in Q1, benefiting from operational leverage and AI-driven efficiency gains.

Management has increased long-term margin targets to 40-45% adjusted EBITDA, citing benefits from AI automation across engineering, sales, and service operations.

Usage of AI-powered features has more than doubled, with over 1.2 million questions answered by the AI assistant.

3. Exit P/E Multiple: 16.3x

The market values Paylocity at 16.7x earnings. We assume the P/E will compress modestly to 16.3x over our forecast period.

Near-term integration from the Airbase acquisition creates execution risk. The company must successfully combine operations while maintaining growth momentum across HCM, finance, and IT.

As platform benefits become clearer and Paylocity demonstrates sustained growth with improving margins, the company should maintain a reasonable multiple.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Software companies face spending cycles and competitive pressures. Here’s how Paylocity stock might perform under different scenarios through June 2030:

- Low Case: If revenue growth slows to 7.8% and net income margins compress to 23.9%, investors still see a 25.2% total return (5.2% annually).

- Mid Case: With 8.7% growth and 25.6% margins, we expect a total return of 56.2% (10.7% annually).

- High Case: If platform adoption accelerates and Paylocity maintains 26.9% margins while growing at 9.6%, returns could hit 90.0% total (15.7% annually).

See what analysts think about PCTY stock right now (Free with TIKR) >>>

The range reflects execution on finance and IT adoption, successful Airbase integration, and margin expansion as AI drives efficiency gains.

In the low case, platform expansion disappoints, or integration challenges emerge.

In the high case, cross-sell momentum exceeds expectations, broker relationships strengthen further, and AI benefits materialize faster than anticipated.

How Much Upside Does Paylocity Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!