Key Takeaways:

- TTR Franchise Boom: 135% year-over-year growth driven by AMVUTTRA cardiomyopathy launch.

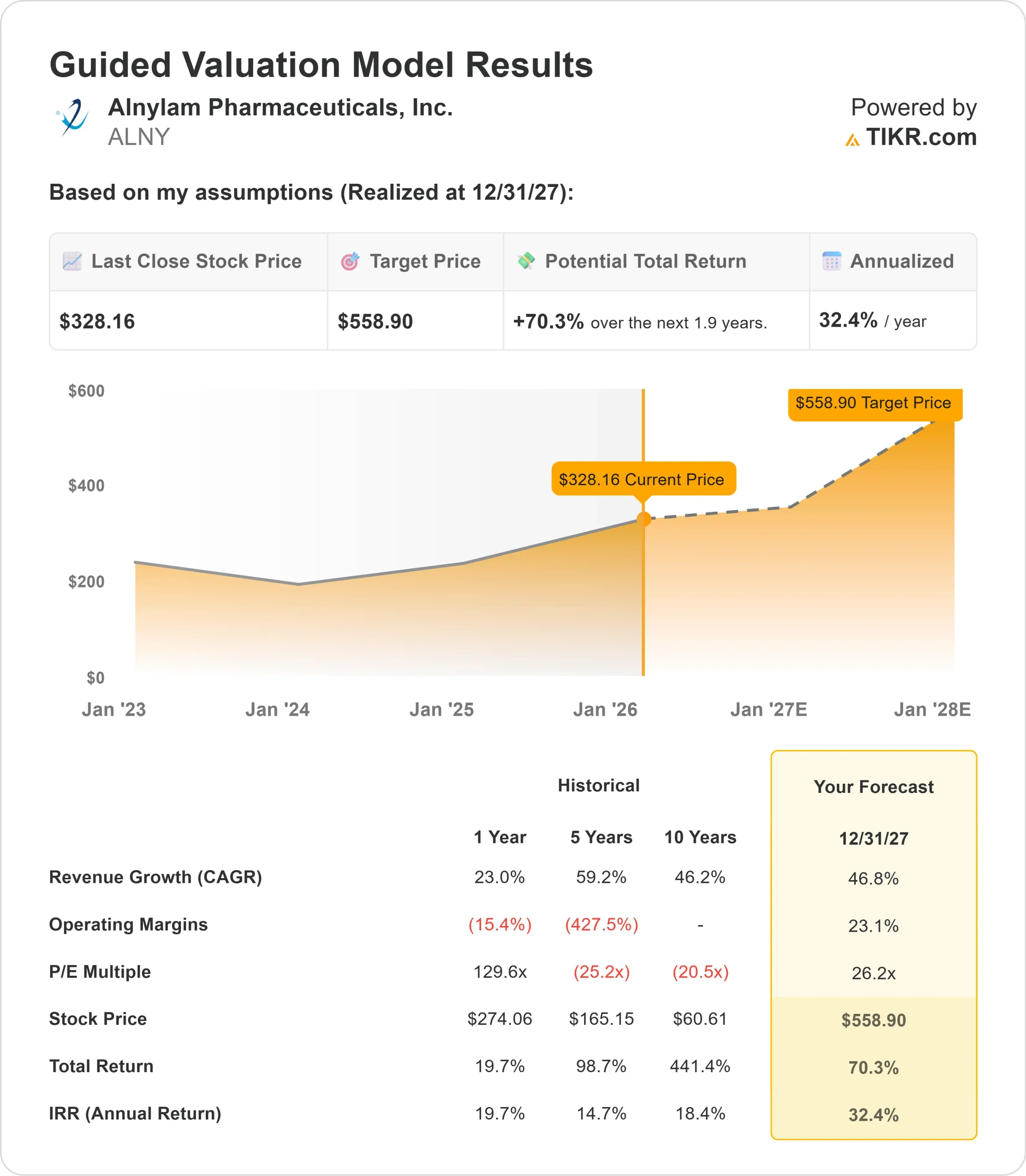

- Price Projection: Based on current execution, ALNY stock could reach $559 by December 2027.

- Potential Gains: This target implies a total return of 70% from the current price of $328.

- Annual Return: Investors could see roughly 32% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Alnylam Pharmaceuticals (ALNY) just posted one of its strongest quarters ever with total revenues of $851 million, up 103% year-over-year.

The company’s TTR franchise generated $724 million in sales, driven by the U.S. launch of AMVUTTRA for cardiomyopathy.

CEO Yvonne Greenstreet is executing an aggressive growth strategy centered on TTR leadership. The company raised its 2025 revenue guidance to $2.95-$3.05 billion, a $275 million increase at the midpoint. This represents 82% growth compared to 2024.

AMVUTTRA patient demand roughly doubled in Q3 versus Q2, with broad adoption across both academic and community settings.

The company is also advancing multiple Phase III trials, including the ZENITH cardiovascular outcomes trial for zilebesiran in hypertension.

Despite extraordinary momentum in its TTR franchise, Alnylam stock trades at $328, offering upside for investors who recognize the company’s transformation into a top-tier biotech.

See analysts’ full growth forecasts and estimates for ALNY stock (It’s free) >>>

What the Model Says for Alnylam Pharma Stock

We analyzed Alnylam’s evolution into the dominant player in TTR amyloidosis, with an expanding pipeline of multibillion-dollar opportunities.

- The company is capitalizing on a massive, underdiagnosed market. AMVUTTRA now serves patients with both polyneuropathy and cardiomyopathy, creating a broad revenue base.

- The drug’s quarterly subcutaneous administration and superior TTR knockdown are resonating with physicians who previously relied on daily oral stabilizers.

- Health system setup is essentially complete. Nearly all 170 priority U.S. health systems now use AMVUTTRA, and roughly 90% of patients can receive treatment within 10 miles of home.

- Payer coverage is strong, with no step edits for first-line use, and most patients pay no out-of-pocket costs.

Using a forecast of 46.8% annual revenue growth and 23.1% operating margins, our model projects the stock will rise to $559 within 1.9 years. This assumes a 26.2x price-to-earnings multiple.

That represents significant compression from Alnylam’s historical P/E average of 129.6x over the past year.

The lower multiple acknowledges the company’s transition from growth-at-all-costs to sustainable profitability while managing competitive pressures in the TTR space.

The real value lies in maintaining AMVUTTRA’s launch momentum while expanding internationally and advancing next-generation therapies like nucresiran with biannual dosing.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ALNY stock:

1. Revenue Growth: 46.8%

Alnylam’s growth centers on the AMVUTTRA cardiomyopathy opportunity in the U.S., which delivered approximately $300 million in Q3 net revenues. This doubled from Q2, reflecting strong physician adoption.

The company is gaining share in the competitive first-line setting while maintaining clear leadership among patients progressing on stabilizers. International launches are beginning, with Japan tracking in line with leading analogs and Germany in early stages following reimbursement decisions.

Beyond TTR, the pipeline offers substantial upside. The ZENITH Phase III trial for zilebesiran in hypertension could support a launch around 2030, targeting an 11,000-patient outcomes study. The company is also advancing programs in bleeding disorders and neurodegenerative diseases including Alzheimer’s.

2. Operating margins: 23.1%

Alnylam achieved non-GAAP operating income of $476 million in Q3, a dramatic turnaround from losses in prior years. The company is proving it can scale profitably.

Gross margins on product sales hit 77% in Q3, though they will compress slightly as AMVUTTRA royalty rates increase with higher sales volumes. Management expects mid-single-digit net price declines on a year-over-year basis for the TTR franchise.

R&D expenses grew 23% year-over-year to support multiple Phase III trials, while SG&A increased 35% to fund the AMVUTTRA launch. As the commercial infrastructure matures, operating leverage should improve.

3. Exit P/E Multiple: 26.2x

The market currently values Alnylam at 34.2x trailing earnings. We assume compression to 26.2x as the company matures.

Near-term execution risk around international launches and competitive dynamics in TTR amyloidosis weigh on the multiple. Pfizer’s stabilizer and other silencers are entering the market, though Alnylam maintains differentiation through quarterly dosing and robust HELIOS-B outcomes data.

As the company demonstrates sustainable profitability and pipeline advancement, it should command a premium biotech multiple. The transition from a single-product story to a diversified commercial engine supports long-term valuation expansion.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

The TTR franchise faces evolving competitive dynamics and execution risk on international launches. Here’s how Alnylam stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth slows to 27.3% and net income margins reach 34.0%, investors still see a 111% total return (21.0% annually).

- Mid Case: With 30.2% growth and 37.0% margins, we expect a total return of 199% (32.4% annually).

- High Case: If TTR momentum accelerates and Alnylam achieves 39.8% margins while growing at 33.1%, returns could hit 315% total (44.0% annually).

See what analysts think about ALNY stock right now (Free with TIKR) >>>

The range reflects execution on AMVUTTRA international launches, successful defense against competitive threats, and advancement of pipeline programs into commercial products.

In the low case, competition intensifies or international pricing disappoints.

In the high case, AMVUTTRA becomes the standard of care globally and pipeline programs deliver ahead of schedule.

How Much Upside Does Alnylam Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!