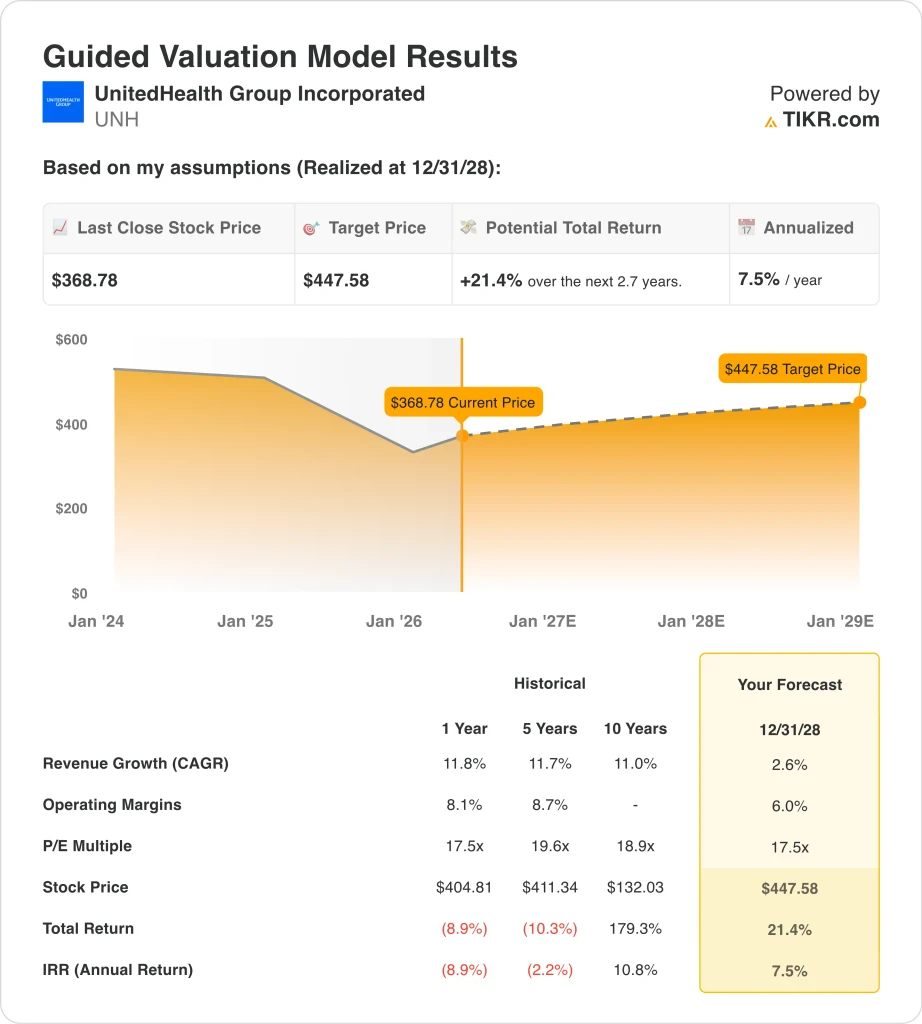

Key Stats for UnitedHealth Stock

- Past week’s performance: 4%

- 52-week range: $235 to $410

- Valuation model target price: $448

- Implied upside: +21.4% over 2.7 years

Value your favorite stocks like UNH with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

UnitedHealth Group (UNH) rose about 4% over the past week. The move built on a strong Q1 2026 earnings report released on April 21, with quarterly revenue of $111.7 billion clearing the analyst consensus of $109.6 billion by more than $2 billion.

Investor sentiment shifted positively as Reuters noted the company appears to be “finding its footing” after a challenging stretch. And street commentary described the quarter as evidence that the company’s turnaround is gaining pace.

Alongside the earnings release, UnitedHealthcare announced it would eliminate most prior authorizations for medical procedures. Prior authorization is the process by which insurers require doctors to obtain advance approval before covering certain treatments or medications.

This policy shift is one of the most significant changes UnitedHealthcare has made in years. And it signals a strategic effort to reduce administrative friction for healthcare providers and improve relations with patients.

Other headlines added context to the operating environment. UnitedHealth limited employee raises to 2% in 2025, per Bloomberg News, while CEO Stephen Hemsley received total compensation of $60.9 million for the same year.

And on April 22, the company pushed back on a Trump administration Medicare pilot program covering GLP-1 weight-loss drugs like Ozempic and Wegovy. Covering these medications under Medicare would add materially to the company’s medical cost base, so resistance to this pilot reflects disciplined cost management.

If UNH stock is to recover toward prior highs near $410, investors need continued operational improvement and confirmation that the prior authorization change does not raise medical costs materially.

See analysts’ growth forecasts and price targets for UNH (It’s free) >>>

Is UnitedHealth Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 2.6%

- Operating Margins: 6%

- Exit P/E Multiple: 17.5x

Based on these inputs, the model estimates a target price of $448, implying +21.4% total return over the next 2.7 years and a 7.5% annualized return.

A 7.5% annual return is below the 10% threshold many investors require for a compelling opportunity. But it is above the risk-free rate. And the current 2.4% dividend yield adds to the return profile, while the stock trading well below its 52-week high of $410 reflects meaningful pessimism already priced in.

The conservative model assumptions reflect real near-term challenges. Revenue growth of just 2.6% annually implies UNH’s top-line expansion will be slower than its historical 11% pace. And the 6.0% operating margin is well below the company’s historical performance in the 8% to 9% range. These inputs capture ongoing uncertainty around claims costs, regulatory changes, and competitive pressures in the Medicare Advantage market.

Compared to the broader managed care sector, UNH trades at roughly 19x next-twelve-month earnings. This is a modest premium to peers like Cigna and Centene. But UNH’s scale, its diversified Optum services and technology segment, and its historically strong free cash flow support a multiple premium.

What’s Driving UNH Stock Going Forward?

The prior authorization policy change is the most important near-term operational catalyst. UnitedHealthcare is targeting 70% of prior authorizations under a standardized electronic submission process by the end of 2026.

This shift should reduce friction for healthcare providers and build goodwill with patients. But investors will monitor medical cost ratios closely in Q2 and Q3 to assess whether the policy change is raising claims expense.

Cost control remains a key focus for the rest of 2026 and into 2027. Management’s pushback on the GLP-1 Medicare pilot signals continued emphasis on disciplined cost management in the Medicare Advantage (MA) business. Medicare Advantage is the private insurance option for Medicare-eligible seniors. And it represents one of the largest and most closely watched segments of UNH’s overall business.

The Amedisys merger, which received court approval for settlement in December 2025, adds another dimension to UNH’s strategic positioning. Amedisys is a home health and hospice provider. And the acquisition expands UNH’s Optum Health services division, which delivers care in settings outside traditional hospitals.

The Q2 2026 earnings report expected on July 14 is the next major checkpoint for investors. Analysts will assess whether the prior authorization change is affecting claims costs. And management commentary on Medicare Advantage enrollment and 2027 plan pricing will shape expectations for the next leg of UNH’s recovery story.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in UnitedHealth?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UNH, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UNH alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze UnitedHealth stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!