Key Stats for Moody’s Stock

- 52-Week Range: $402 to $547

- Current Price: $456

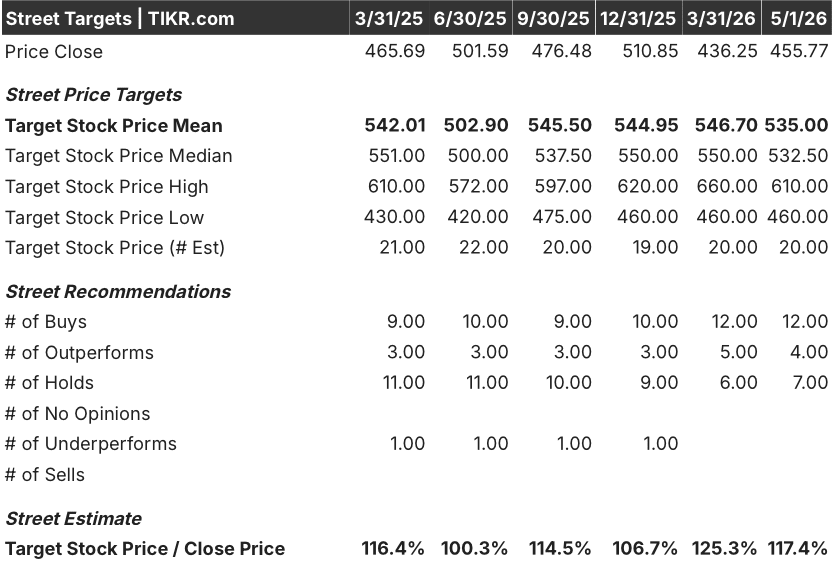

- Street Mean Target: $535

- Street High Target: $610

- Analyst Consensus: 12 Buys / 4 Outperforms / 7 Holds

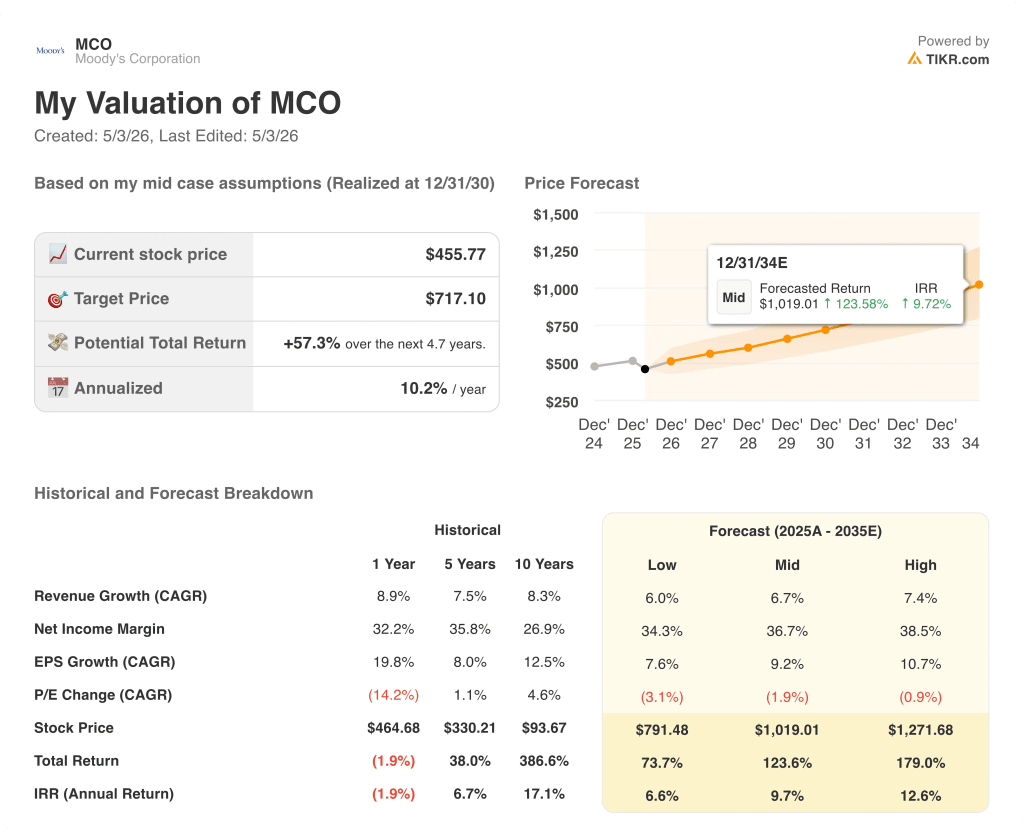

- TIKR Model Target (Dec. 2030): $717

What Happened?

Moody’s Corporation (MCO), the credit ratings and analytics giant that grades debt and sells data intelligence to financial institutions worldwide, reported record Moody’s Investors Service revenue of $1.15 billion in Q1 2026, even as Moody’s stock trades roughly 10% below where it started the year.

The quarter’s headline was a guidance raise: management lifted its full-year 2026 adjusted diluted EPS outlook to a range of $16.40 to $17.00, up from the prior range of $15.00 to $15.60, signaling that the business is running ahead of internal expectations.

Revenue across both segments grew 8% to $2.1 billion, with Moody’s Analytics (the subscription-driven research and data arm) posting an 11% increase in recurring revenue fueled by demand for insurance platforms, cloud-based know-your-customer solutions, and banking analytics.

AI-related debt issuance and large-scale infrastructure financing drove the record performance at Moody’s Investors Service, the ratings arm, as corporations raced to fund data centers and energy infrastructure through the bond market.

Chief Executive Rob Fauber stated on the Q1 2026 earnings call that “as AI adoption accelerates, it is driving demand for Moody’s decision-grade connected intelligence in high-stakes environments,” connecting the company’s 600-million-entity data network directly to the AI infrastructure buildout.

The strategic picture sharpened further: Moody’s expanded its partnership with Microsoft to embed its credit intelligence natively into Microsoft 365 Copilot workflows, named Christina Kosmowski as incoming CEO of Moody’s Analytics effective June, and raised its full-year share repurchase guidance to approximately $2.5 billion, underscoring management’s confidence in forward cash generation.

Wall Street’s Take on MCO Stock

The guidance raise repositions Moody’s stock from a defensive compounder into an active re-rating candidate, with a business model structurally exposed to two of the most durable spending themes in 2026: AI infrastructure and compliance automation.

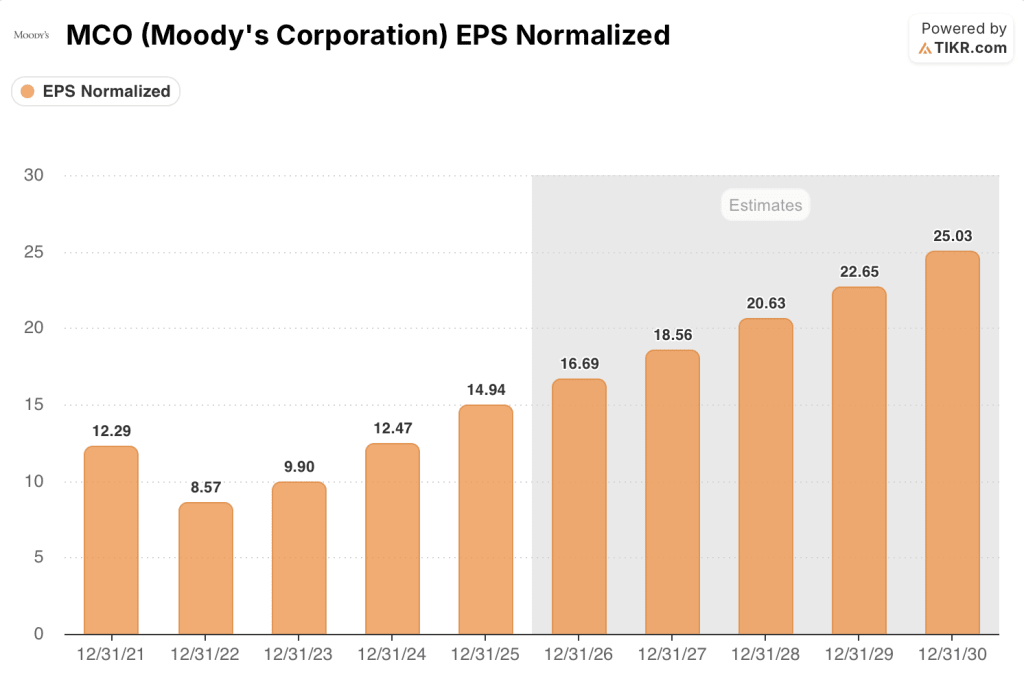

MCO’s normalized EPS reached almost $15 in 2025, up nearly 20%, and the Street now models around $17 for 2026, representing roughly 12% growth, accelerating further to around $19 in 2027 as AI-driven analytics demand compounds into Moody’s Analytics’ recurring revenue base.

Sixteen analysts hold positive ratings on Moody’s stock (12 Buys, 4 Outperforms) against 7 Holds and zero sells, with a mean price target of $535 implying around 17% upside from current levels; Wall Street is specifically watching whether the Microsoft Copilot integration converts enterprise users into new Moody’s Analytics subscribers at scale.

The target spread runs from $460 on the cautious end to $610 on the high end, with the low anchored to concern that bond issuance volumes slow if credit conditions tighten, and the high anchored to a scenario where AI workflow demand pushes Analytics recurring revenue growth into the mid-teens.

Priced at roughly 27x forward 2026 earnings, Moody’s stock trades at a meaningful discount to its own five-year historical average of approximately 31x to 33x forward P/E, at a moment when normalized EPS is growing faster than it did across most of that same historical window, leaving Moody’s stock appearing undervalued against a business compounding earnings at double-digit rates while expanding into agentic AI workflows.

The Kosmowski appointment signals that Moody’s is serious about accelerating the analytics segment: she ran a $4 billion revenue organization at Salesforce and led enterprise customer operations at Slack before joining.

Bond issuance volumes remain the single variable that could break the near-term model: a sustained pullback in investment-grade and infrastructure debt activity would directly compress MIS revenue faster than Analytics growth can offset it.

Q2 2026 earnings will be the first test of whether AI-driven issuance momentum persists beyond Q1 front-loading; watch for MIS revenue holding above $1.1 billion and Analytics recurring revenue growth staying above 10%.

What Does the Valuation Model Say?

TIKR’s mid-case model prices MCO at $717 per share by December 2030, built on a roughly 7% revenue CAGR and net income margins expanding toward 37%, with the AI analytics buildout and recurring subscription mix shift as the primary drivers.

With a roughly 9% EPS CAGR embedded in the mid case and the stock currently trading at around 27x forward earnings against a historical average closer to 32x, the multiple compression embedded in the current price overstates the execution risk for a business that just raised guidance and posted record quarterly ratings revenue, making Moody’s stock undervalued at this entry point.

The investment case hinges on a single question: whether Moody’s Analytics can sustain double-digit recurring revenue growth long enough to force a multiple re-rate, or whether macro-driven issuance volatility keeps a ceiling on sentiment regardless of how the analytics segment performs.

Bull Case

- Moody’s Analytics recurring revenue grew 11% in Q1 2026, extending the trend that drove the segment to $926 million in the quarter; a full-year run rate above $3.7 billion would confirm the subscription floor is structurally rising

- The Microsoft 365 Copilot integration opens Moody’s data to non-specialist enterprise users for the first time, expanding the addressable market beyond traditional credit professionals

- The Anthropic MCP partnership embeds Moody’s compliance workflows into Claude Enterprise, adding a second major AI distribution channel outside of Microsoft

- Share repurchases of approximately $2.5 billion in 2026 represent roughly 3% of market cap, providing a per-share earnings tailwind that compounds into the EPS CAGR even if revenue growth moderates

- TIKR’s high case puts MCO at around $1,272 by 2030, implying a roughly 13% annualized return, anchored to a 7.4% revenue CAGR and net income margins reaching 38.5%

Bear Case

- Investment-grade issuance is cyclical: the $1.15 billion MIS quarter was fueled by AI infrastructure demand, but infrastructure financing cycles have historically proven shorter than consensus assumes

- Moody’s Analytics recurring revenue growth of 11% is still below the pace needed to fully offset a meaningful MIS revenue contraction if credit markets tighten into year-end

- The forward P/E of roughly 27x still prices in above-average growth; any guide-down on full-year EPS from the $16.40 to $17.00 range would compress the multiple further at the current price

- TIKR’s low case puts MCO at around $791 by 2030, implying a roughly 7% annualized return, less compelling relative to the macro risk embedded in the ratings business

Should You Invest in Moody’s Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MCO stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Moody’s Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MCO stock on TIKR for Free →