Key Stats for Salesforce Stock

- Past week’s performance: -2.4%

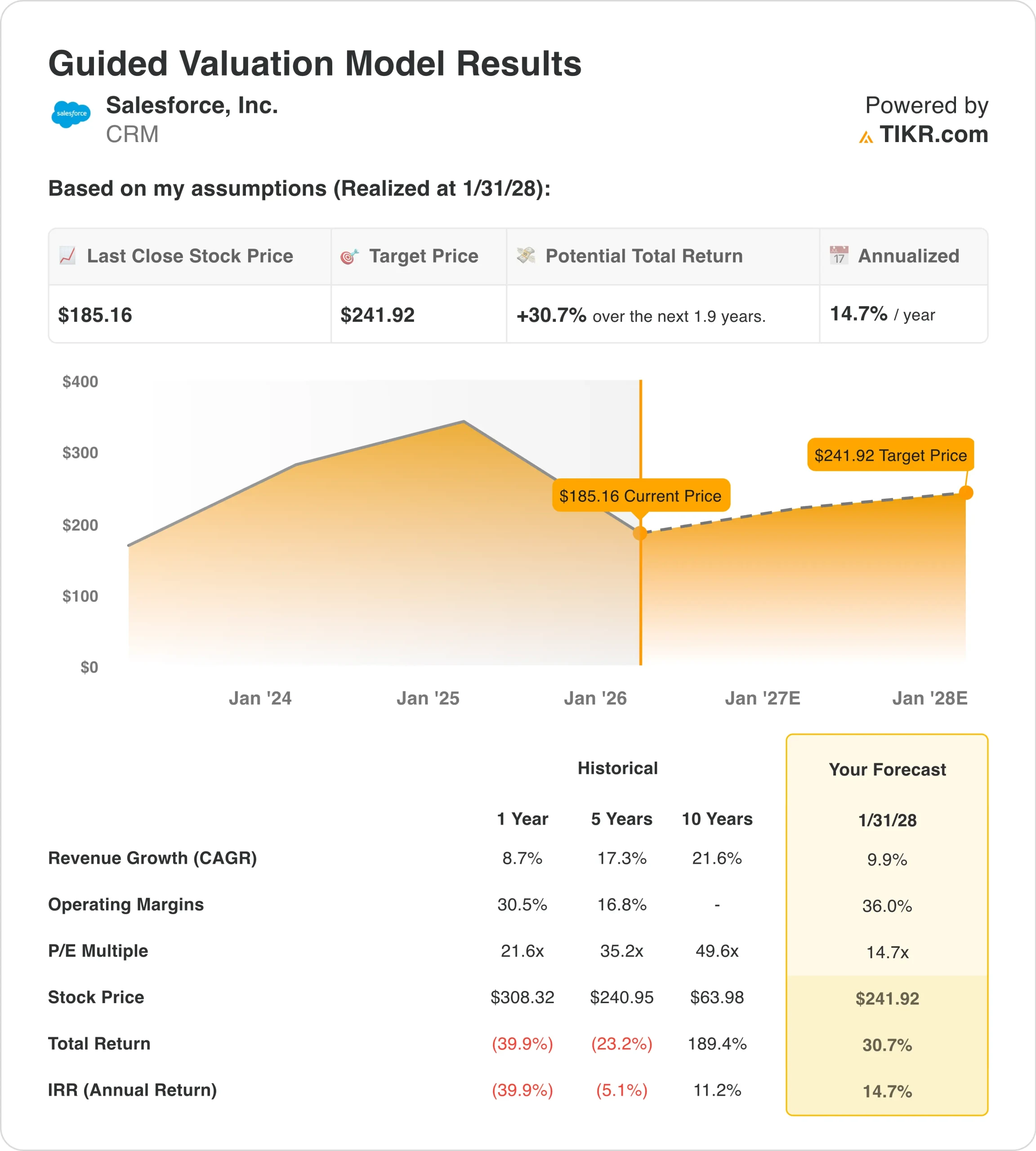

- 52-week range:$180 to $314

- Valuation model target price: $242

- Implied upside: 30.7% over 1.9 years

Value your favorite stocks like Salesforce with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Salesforce (CRM) stock was roughly flat over the past week, but shares have remained volatile heading into earnings because investors are weighing fresh AI-related headlines, deal activity, and broader software-sector sentiment ahead of a key reporting catalyst on Feb. 25.

In early February, Salesforce cut fewer than 1,000 jobs, according to a Business Insider report cited by Reuters, and the reductions affected roles across marketing, product management, data analytics, and parts of the Agentforce AI product organization, which kept investor focus on cost discipline and internal restructuring.

At the same time, Salesforce has continued to push its Agentforce strategy through acquisitions, and that pace of deal-making has been a major talking point during the past two weeks.

Salesforce announced a definitive agreement to acquire Cimulate to strengthen AI-powered commerce and improve product discovery and conversational shopping experiences for retailers, and then the company said it signed a definitive agreement to acquire Momentum to expand how Agentforce 360 and Slackbot can ingest and analyze unstructured third-party voice and video data for agentic workflows.

Salesforce’s stock has also moved alongside the broader software group in February, as Reuters reported that parts of the U.S. market entered an “AI scare trade,” pressuring software names while investors reassessed which business models could face faster disruption from AI-enabled automation.

The next major scheduled catalyst is Salesforce’s fourth-quarter and full-year fiscal 2026 results on Feb. 25, and the company has also scheduled an earnings conference call the same day, which makes the report a key moment that can reset near-term expectations for growth, margins, and guidance.

See analysts’ growth forecasts and price targets for CRM (It’s free) >>>

Is Salesforce Stock Undervalued?

Under the valuation model assumptions realized through January 2028, the stock is modeled using:

- Revenue growth (CAGR): 9.9%

- Operating margins: 36%

- Exit P/E multiple: 14.7x

Based on these inputs, the model estimates a target price of $241.92, implying a 30.7% total return from the current share price of $185.16 and a 14.7% annualized return over the next 1.9 years.

Operationally, Salesforce’s recent results anchor the valuation model in profitability and cash flow rather than rapid revenue expansion, because LTM revenue totals $40.3B while gross margin stands at 77.7% and EBIT margin at 22.0%, highlighting how the company has expanded operating leverage compared with earlier years.

Cash generation remains a central support for the story because Salesforce produced $12.9B of LTM free cash flow and a 32.0% free cash flow margin while also returning capital through $8.9B of LTM share repurchases and paying $1.6B of common dividends.

The balance sheet also remains relatively conservative for a company of this size, because LTM net debt is about $312M and net debt/EBITDA is 0.03x, which gives Salesforce flexibility to keep investing in AI initiatives while also continuing shareholder returns and targeted acquisitions.

From a valuation perspective, the stock’s multiple compression over the past year has been significant because CRM trades around 14.7x forward earnings, and the model assumes a 14.7x exit P/E multiple, which implies the forecast is not dependent on a higher terminal valuation to work.

If sentiment remains volatile into earnings, crowded near-term narratives explain much of the uncertainty, since Salesforce continues integrating AI-focused acquisitions, managing workforce actions, and operating within a software sector that remains sensitive to shifting AI disruption concerns, making guidance and commentary on Feb. 25 as important as the quarter’s headline numbers.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>