Key Stats for Corteva Stock

- Year-to-Date Performance: 13%

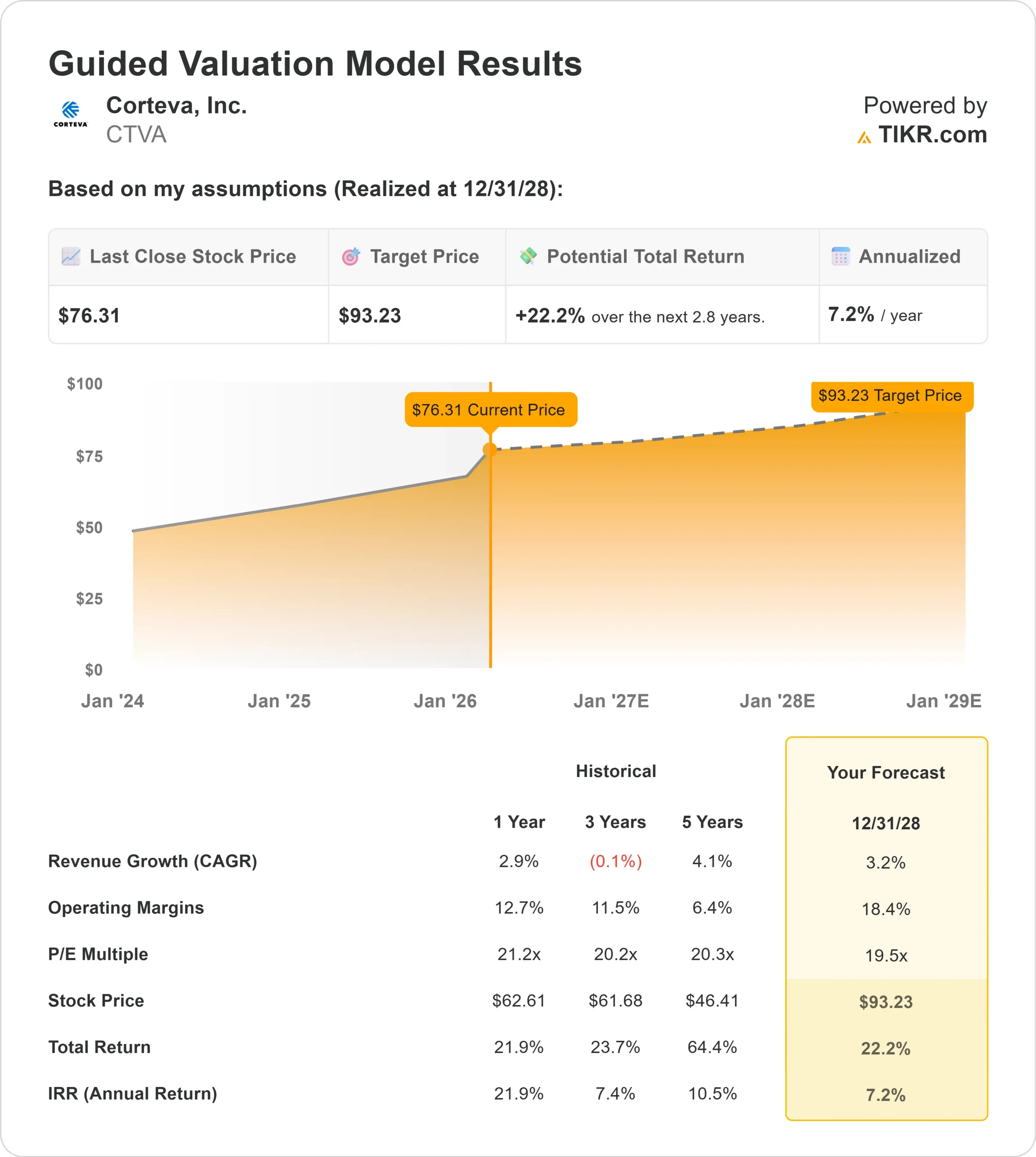

- 52-Week Range: $53 to $77

- Valuation Model Target Price: $93

- Implied Upside: 22%

Value your favorite stocks like Corteva with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Corteva stock is up about 13% year to date, recently trading near $76 per share as investors responded to strong earnings momentum, licensing acceleration, and reaffirmed 2026 guidance. Shares remain close to their 52 week high of $77, reflecting sustained buying interest following record profitability.

The stock moved higher after the company reported record 2025 results and reinforced growth expectations for 2026.

Operating EBITDA rose 14% to $3.85 billion, margins expanded more than 200 basis points to above 22%, and free cash flow reached $2.9 billion.

Management reaffirmed 2026 operating EBITDA guidance of $4.0 billion to $4.2 billion, about 7% growth at the midpoint, driven by mid single digit Crop Protection volume growth, $120 million of net royalty improvement, and $200 million of productivity savings, with CEO Chuck Magro stating, “We are reiterating our preliminary operating EBITDA midpoint of $4.1 billion.”

The company also announced a $610 million Bayer agreement expected to generate about $1 billion of aggregate earnings upside over the next decade while accelerating corn and cotton licensing opportunities.

Institutional positioning has remained active. JPMorgan Chase cut its stake by 17.9% to 4.17 million shares valued at about $282 million, while Citigroup reduced its holdings by 12.2% to 2.46 million shares worth about $166 million.

Barings trimmed its position by 34.0%, and Shell Asset Management reduced its stake by 64.3%. At the same time, Jupiter Asset Management initiated a 976,446 share position valued at about $66 million, Alberta Investment Management acquired 74,200 shares worth roughly $5.0 million, and NEOS Investment Management increased its stake by 40.8%.

Despite selective trimming, institutional investors and hedge funds collectively own about 81.54% of Corteva, with Vanguard holding 80.2 million shares representing 11.81% of the company.

The stock’s 13% year to date advance reflects confidence in margin expansion, accelerating royalty income, and stronger earnings visibility into 2026.

See analysts’ growth forecasts and price targets for Corteva (It’s free) >>>

Is Corteva Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 3.2%

- Operating Margins: 18.4%

- Exit P/E Multiple: 19.5x

Revenue is projected to rise from about $17.4 billion in 2025 to nearly $19.9 billion by 2030, reflecting steady seed trait adoption, expanding licensing income, and continued demand for differentiated crop protection products rather than an aggressive acreage rebound.

The most important driver in 2026 is margin expansion. Crop Protection volumes are expected to grow mid single digits, royalty income is set to improve by $120 million as Conkesta and corn licensing ramp, and productivity savings of $200 million provide operating leverage.

With EBITDA margins already above 22%, incremental revenue growth can translate into outsized earnings growth.

The Bayer agreement also materially changes the long term earnings profile. Accelerated corn licensing beginning in 2027, entry into cotton licensing, and improved freedom to operate increase royalty visibility, which tends to carry higher margins and lower capital intensity than branded sales.

Corteva’s balance sheet supports the setup, with $2.9 billion in free cash flow generated in 2025 and continued capital returns through dividends and share repurchases.

Based on these inputs, the model estimates a target price of $93, implying about 22% upside from current levels.

At today’s valuation, Corteva appears undervalued, with 2026 performance likely driven by licensing acceleration, Crop Protection volume growth, and sustained margin expansion.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>