Key Takeaways:

- AI Acceleration: LiveRamp’s data network is positioned as essential infrastructure for AI-powered marketing.

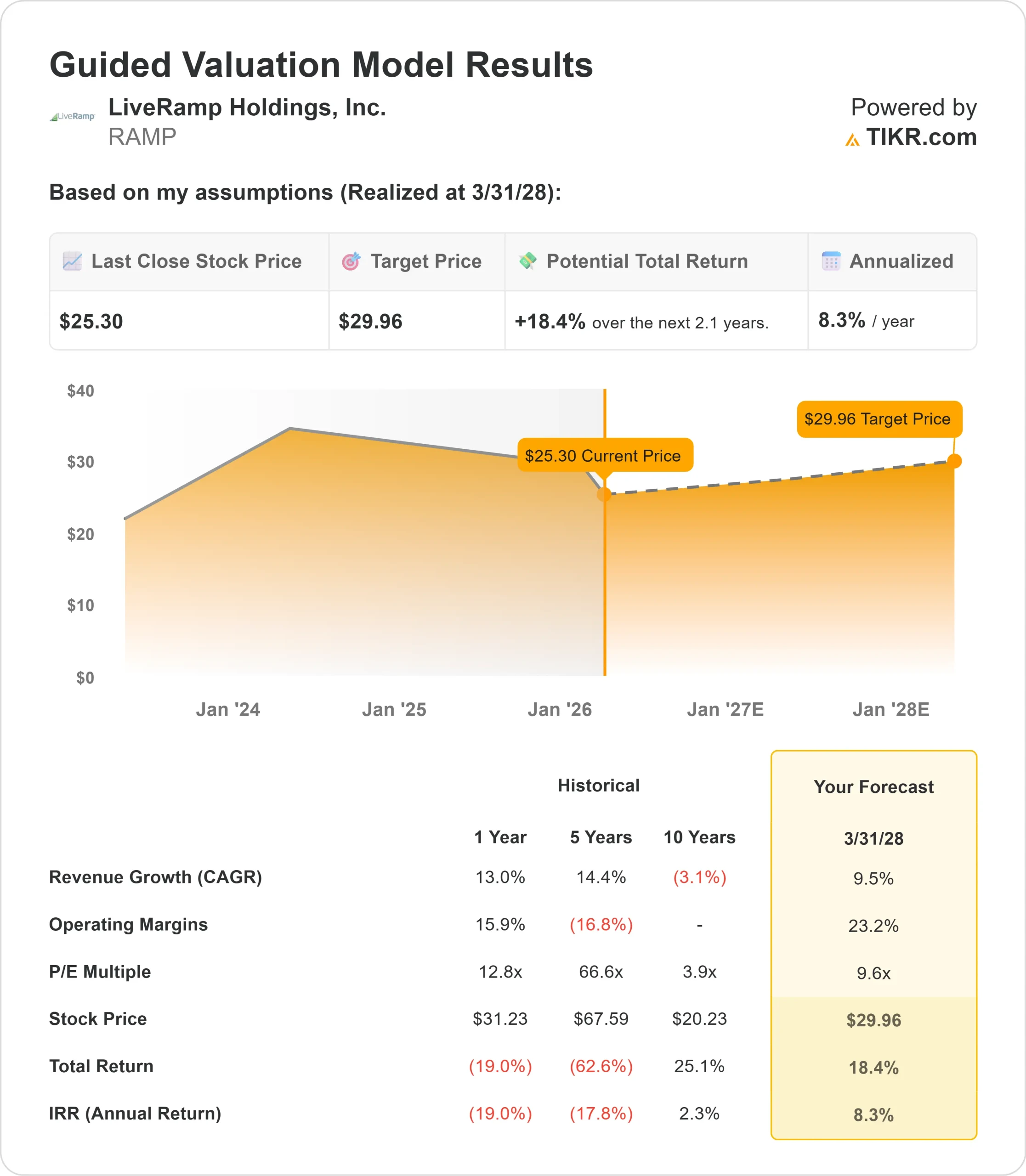

- Price Projection: Based on current execution, RAMP stock could reach $30 by March 2028.

- Potential Gains: This target implies a total return of 18% from the current price of $25.

- Annual Return: Investors could see roughly 8% growth over the next 2.1 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

LiveRamp (RAMP) delivered a strong third quarter in fiscal 2026 with revenue and operating income exceeding guidance for the 11th consecutive quarter.

CEO Scott Howe emphasized that AI represents a tailwind rather than a threat to the business.

- The company posted 9% revenue growth with Subscription revenue accelerating to match that pace.

- More importantly, annual recurring revenue (ARR) jumped $11 million quarter-over-quarter while total customer count increased by 15—the largest quarterly gain in over three and half years.

- While software companies face disruption, LiveRamp provides the critical data infrastructure that enables AI systems to operate securely across platforms.

- The company has already signed over 20 AI partnerships, including collaborations with Google and emerging players like Scout.

- The company operates the industry’s largest consented identity graph, enabling precise targeting and measurement across channels.

- As AI workflows accelerate the advertising cycle—plan, activate, optimize, measure—more data flows through LiveRamp’s platform, directly increasing revenue without proportional cost increases.

The shift to usage-based pricing is gaining momentum. Following successful pilots with direct brand customers, LiveRamp expanded this model to reseller partners, including Publicis.

The new pricing lowers barriers to entry for mid-sized brands while allowing existing customers to scale flexibly across all platform capabilities.

See analysts’ full growth forecasts and estimates for RAMP stock (It’s free) >>>

What the Model Says for LiveRamp Stock

We analyzed LiveRamp’s position as the foundational data network powering AI-driven marketing.

The company benefits from four competitive moats that become more valuable in an AI world: its industry-leading identity graph, true platform interoperability, enterprise-grade data governance, and unmatched network scale connecting thousands of customers and partners.

AI amplifies these advantages by increasing the velocity and volume of data moving across the network. Every AI application, agent, or surface becomes a new node generating revenue.

Management estimates roughly 10% of current activations already flow to AI-enabled partnerships.

LiveRamp’s expansion into commerce media through partners like Uber and PayPal opens new verticals. Travel companies, food delivery platforms, and financial services providers are launching commerce media networks—each requiring LiveRamp’s infrastructure to connect their smaller SMB advertisers.

The clean room business continues with strong momentum, particularly for cross-platform measurement and Commerce Media use cases.

About 70% of LiveRamp’s 50 largest integrations now involve CTV providers or platforms enabled to buy CTV inventory.

Using a forecast of 9.5% annual revenue growth and 23.2% operating margins, our model projects the stock will rise to $30 within 2.1 years. This assumes a 9.6x price-to-earnings multiple.

That represents compression from LiveRamp’s historical P/E averages of 12.8x (one year) and 66.6x (five years).

The lower multiple reflects near-term market uncertainty around AI’s impact on software, despite management’s compelling case that LiveRamp benefits from increased AI adoption.

The real value lies in capturing the structural shift toward data collaboration and AI-powered marketing while expanding operating margins toward the company’s Rule of 40 target by fiscal 2028.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for RAMP stock:

1. Revenue Growth: 9.5%

LiveRamp’s growth centers on structural demand for secure data collaboration.

The company delivered 9% consolidated revenue growth in Q3 with strong momentum across subscription, marketplace, and services.

Management expects to reach 10%+ revenue growth as usage-based pricing takes hold and AI partnerships scale.

Recent bookings were up strong double digits, driven primarily by clean room expansions with existing customers.

The Publicis partnership expansion and similar deals in the pipeline should accelerate growth in the back half of fiscal 2027.

2. Operating margins: 23.2%

LiveRamp has expanded operating margins by an average of 3 points annually over the past five years.

This fiscal year, the company is on track to expand margins by 4 points to 22% while still investing in growth initiatives.

The margin story improves with scale.

Management’s highly fixed-cost structure means that higher revenue growth naturally increases profitability.

Ongoing offshoring initiatives continue to deliver additional efficiency gains. The company targets 25-30% operating margins as part of its Rule of 40 goal by fiscal 2028.

3. Exit P/E Multiple: 9.6x

The market currently values LiveRamp at 9.8x earnings. We assume the P/E holds relatively steady at 9.6x over our forecast period.

This conservative multiple reflects market skepticism about AI’s impact on software companies.

However, as LiveRamp demonstrates that AI drives incremental data volume rather than displacing revenue, the multiple should go higher.

The company’s positioning as essential infrastructure for responsible AI deployment in regulated marketing environments provides defensive characteristics that warrant a premium valuation.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

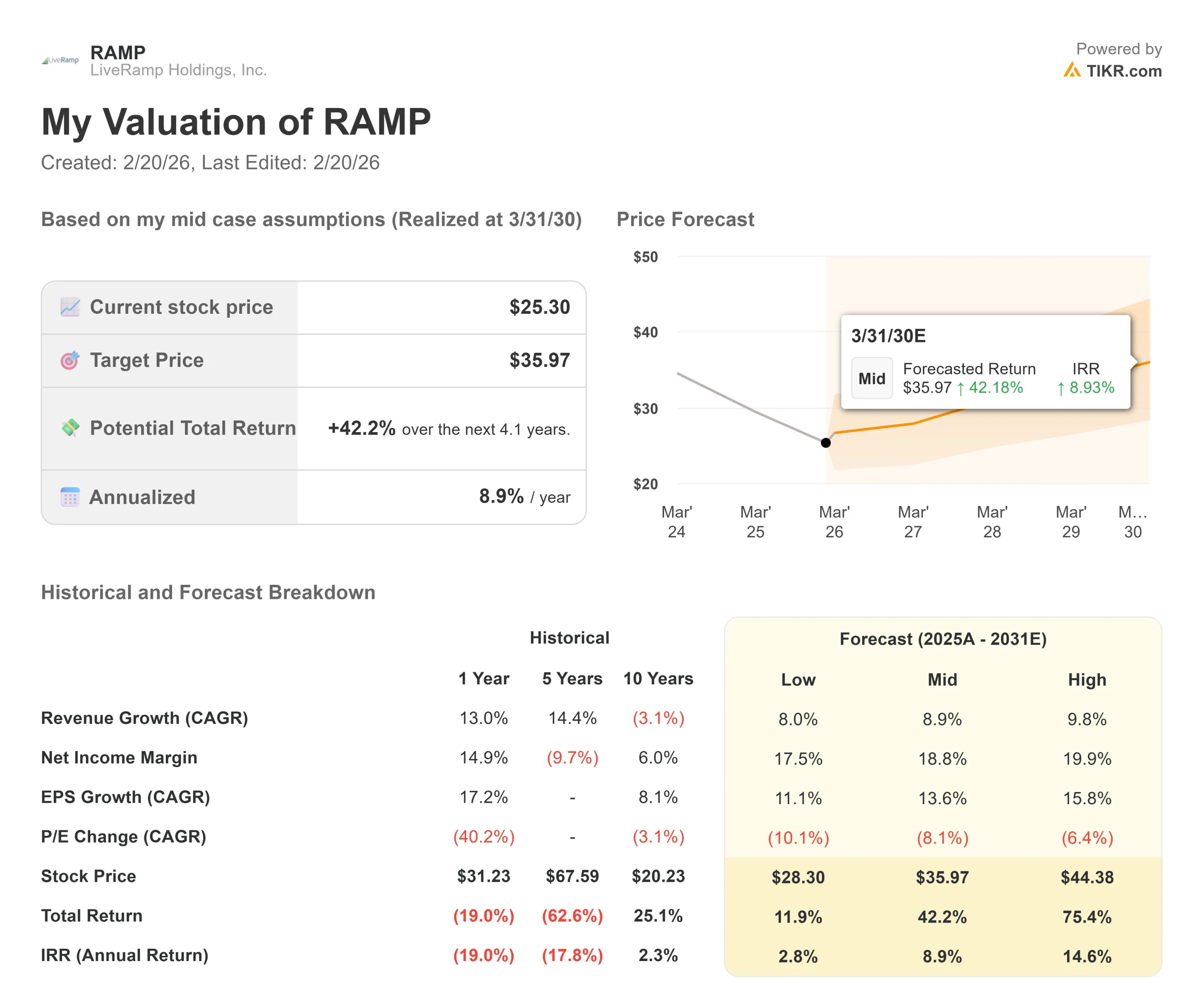

Data collaboration platforms face technology adoption cycles and regulatory changes. Here’s how LiveRamp stock might perform under different scenarios through March 2030:

- Low Case: If revenue growth moderates to 8.0% and net income margins compress to 17.5%, investors still see a 12.0% total return (2.8% annually)

- Mid Case: With 8.9% growth and 18.8% margins, we expect a total return of 42.2% (8.9% annually)

- High Case: If AI adoption accelerates, driving 9.8% revenue growth while LiveRamp maintains 19.9% margins, returns could hit 75.4% total (14.6% annually)

See what analysts think about RAMP stock right now (Free with TIKR) >>>

The range reflects execution on AI partnerships, successful scaling of usage-based pricing, and the company’s ability to reach its Rule of 40 targets.

In the low case, AI disruption proves more severe than expected or usage-based pricing fails to gain traction.

In the high case, AI partnerships scale faster than anticipated, and operating leverage drives margins ahead of plan.

How Much Upside Does LiveRamp Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!