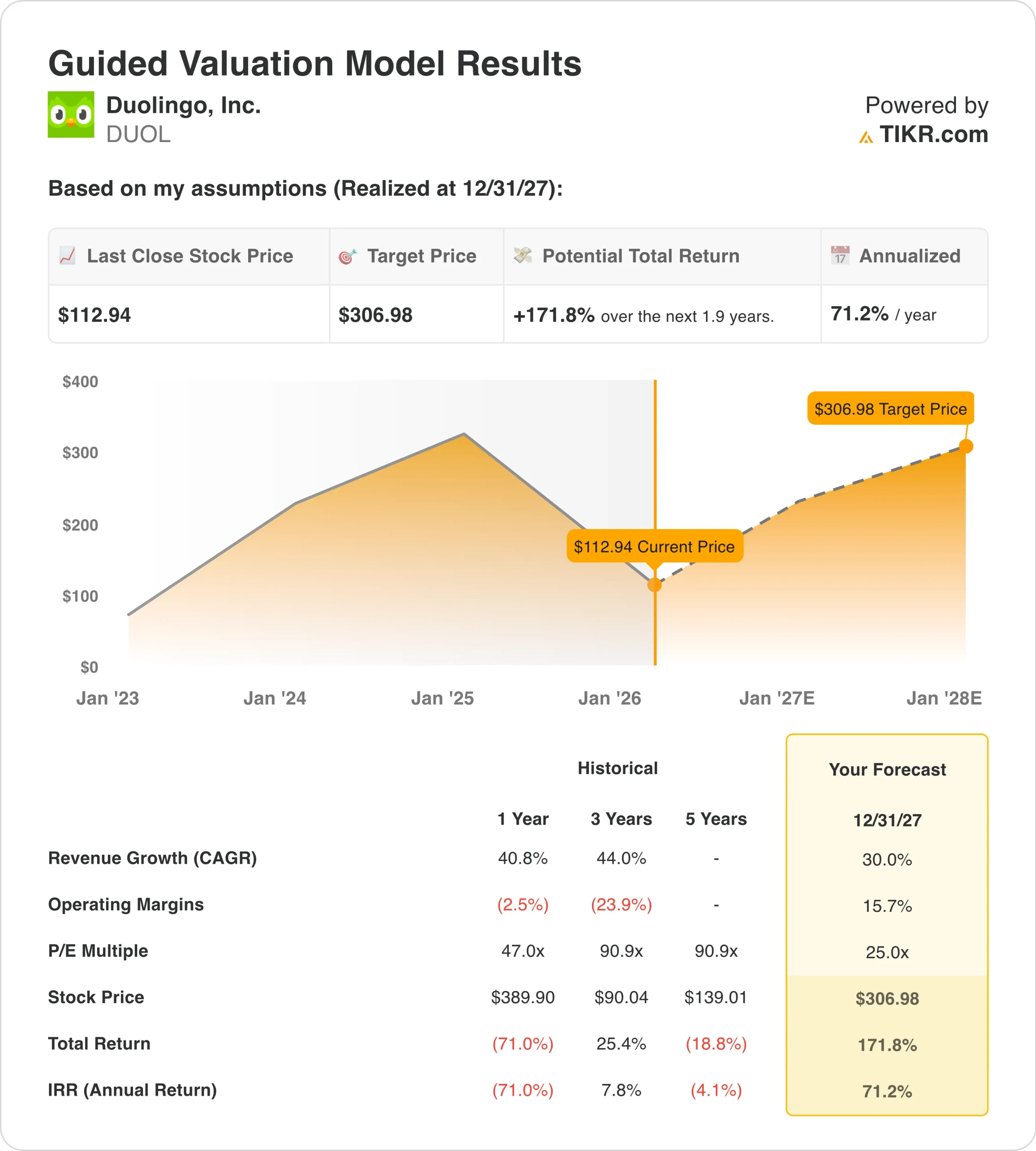

Key Stats for DUOL Stock

- Past week’s performance: stayed flat

- 52-week range: $107 to $545

- Valuation model target price: $307

- Implied upside: 172% over 1.9 years

Value your favorite stocks like DUOL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Shares of Duolingo (DUOL) declined over the past week, with the stock trading near $113 after renewed pressure tied to company-specific news and valuation concerns.

Earlier in January, Duolingo shares slid after Reuters reported that CFO Matt Skaruppa would step down after nearly six years. Although the company named Gillian Munson as the new CFO the same day, the leadership transition added short-term uncertainty, and the stock has remained volatile since.

At the same time, several Reuters “BUZZ” reports in January highlighted softer engagement concerns raised by Wells Fargo, which trimmed its price target. That commentary weighed on sentiment, especially after Duolingo’s strong multi-year run left the stock sensitive to changes in growth expectations.

More recently, Reuters disclosed multiple insider share sales on February 20, including transactions by the CFO, general counsel, and chief engineering officer. While these sales were disclosed as routine, they added to near-term pressure given the stock’s recent pullback.

Importantly, there were no changes to revenue guidance or long-term growth strategy during the week. The move reflects investor recalibration around valuation, leadership changes, and engagement trends rather than a shift in Duolingo’s underlying business performance.

See analysts’ growth forecasts and price targets for DUOL (It’s free) >>>

Is DUOL Stock Undervalued?

Under the valuation model assumptions realized through 2027, the stock is modeled using:

- Revenue growth (CAGR): 30%

- Operating margins: 15.7%

- Exit P/E multiple: 25x

Based on these inputs, the model estimates a target price of $306.98, implying a 171.8% total return from the current share price and a 71.2% annualized return over the next 1.9 years.

Execution remains the central driver behind these assumptions. Duolingo continues to deliver strong top-line growth, with LTM revenue reaching $964 million and gross margins holding near 72%. Operating margins have improved to 11.6% as scale benefits offset continued investment in product and R&D.

Cash generation also strengthened, with LTM free cash flow of $355 million and a 37% margin, supporting Duolingo’s net cash position of more than $1.0 billion. That balance sheet flexibility helps offset near-term volatility tied to leadership changes and engagement concerns.

Looking ahead, investor focus will remain on user engagement trends, operating margin durability, and the upcoming Q4 and full-year 2025 earnings report scheduled for February 26. Those results are likely to shape expectations for growth and profitability into 2026.

If Duolingo continues to scale revenue while maintaining margin discipline, the current share price reflects uncertainty rather than a deterioration in fundamentals.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>